Global| Aug 08 2005

Global| Aug 08 2005Stagnant U.S. Wages & Strong Consumer Spending?

by:Tom Moeller

|in:Economy in Brief

Summary

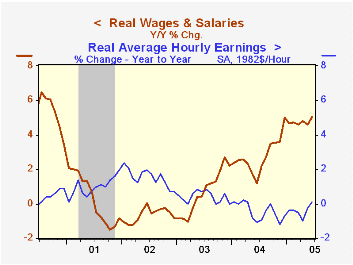

As of July, average hourly earnings in the U.S. when adjusted for inflation had barely risen (0.1%) versus the year ago level. That stagnancy followed an outright decline in real earnings of 0.4% for all of 2004. The lack of movement [...]

As of July, average hourly earnings in the U.S. when adjusted for inflation had barely risen (0.1%) versus the year ago level. That stagnancy followed an outright decline in real earnings of 0.4% for all of 2004.

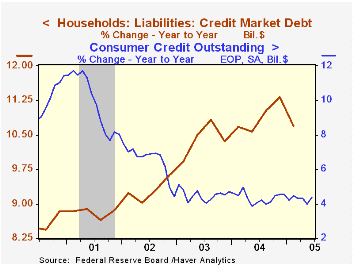

The lack of movement contrasts with the recent strength of consumer spending which has been growing 4% in real terms. Part of the discrepancy is explained by consumers' increased usage of debt. While the latest consumer credit figures show no growth acceleration as of June (steady at 4.5%), consumer debt from the more broadly defined Flow of Funds accounts indicates consumers' indebtedness accelerated to 10-11% growth versus less than 9% as of 2001.

Faster growth in wages & salaries also explains some of the discrepancy. As of the latest personal income report, wages & salaries had risen 7.4% from a year earlier and 5.0% when adjusted for inflation. These growth rates are faster than in the popular average hourly earnings measure for several reasons including the recent increase in job growth, fewer individuals working part time and relatively strong jobs growth in the high wage financial as well as the professional & business services industries.

| 3 Month (AR) | Y/Y | 2004 | 2003 | 2002 | |

|---|---|---|---|---|---|

| Average Hourly Earnings | 3.3% | 2.7% | 2.1% | 2.7% | 2.9% |

| Real | 1.0% | 0.1% | -0.4% | 0.4% | 1.5% |

| Wage & Salary Disbursements | 4.3% | 7.4% | 5.4% | 2.6% | 0.8% |

| Real | 2.4% | 5.0% | 2.8% | 0.7% | -0.6% |

by Louise Curley August 8, 2005

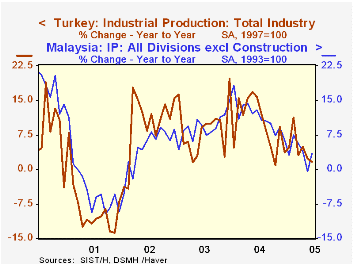

June industrial production figures for Turkey, Malaysia, Slovakia and Italy were released today. The pace of industrial production in the faster growing emerging markets has slowed up this year. In Turkey, industrial production for the first half of this year is only 4.6% above the first half of 2004. In the past three years industrial production in Turkey had grown by 9% or better. In Malaysia, growth in industrial production was 11.29% in 2004, 9.3% in 2003 and 4.6% in 2002. In the first six months of this year, industrial production in Malaysia is up only 3.8% over the corresponding period of 2004. The year to year changes in industrial production in Turkey and Malaysia are shown in the first chart. The deceleration in growth is clear.

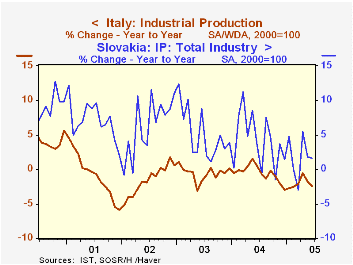

The figures for Slovakia are less dramatic than those for Turkey and Malaysia but show the same trend. Growth in the past six months over the same period of last year was 2.1% compared with growth of 6.4%, 5.0% and 4.2% in the past three years. The second chart contrasts the year to year growth in industrial production in Slovakia with that of Italy. Italy's economy has been one of the most sluggish in the Euro Zone. In fact the economy was in recession in the first half of this year, according to the two quarter decline in GDP definition of a recession. Italy is the only country reporting today that shows a year to year decline in industrial production in the first half of this year.

| Industrial Production | Jun 05 | May 05 | Jun 04 | 1H/1H % | 2004 % | 2003 % | 2002 % |

|---|---|---|---|---|---|---|---|

| Turkey (1997=100) | 130.6 | 129.5 | 128.5 | 4.57 | 9.78 | 8.76 | 9.43 |

| Malaysia (1993=100) | 239.3 | 230.2 | 231.3 | 3.83 | 11.29 | 9.30 | 4.59 |

| Slovakia (2000=100) | 127.3 | 127.8 | 125.2 | 2.05 | 4.20 | 4.08 | 6.40 |

| Italy (2000=100) | 94.7 | 95.4 | 97.0 | -2.01 | -0.58 | -0.60 | -1.62 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief