Global| Dec 30 2016

Global| Dec 30 2016Spain's HICP Spurts into the Land of Policy Dispute

Summary

Spain offers a very early read on inflation in December. The headlines of the HICP and CPI show a spurt in progress with a nearly 1% gain (0.8% and 0.9%, respectively) in the HICP and CPI readings in the month of December alone. These [...]

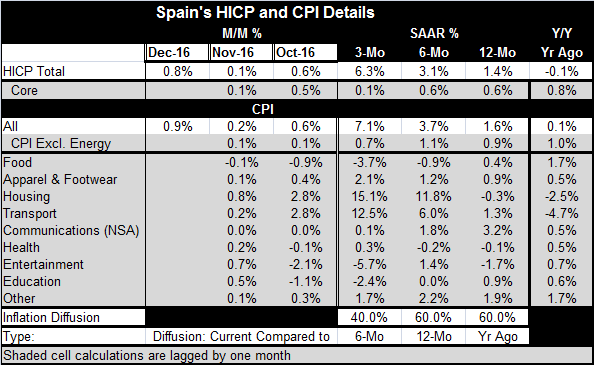

Spain offers a very early read on inflation in December. The headlines of the HICP and CPI show a spurt in progress with a nearly 1% gain (0.8% and 0.9%, respectively) in the HICP and CPI readings in the month of December alone. These compare to gains of 0.1% in the HICP and of 0.2% in the CPI in November. December readings exist only for the two headline series. In the table, we have placed the detail data in columns with a one-month lag. The three-month gain for the headline series is for the period ended in December; for the detailed categories and the core readings it will be for period ended in November and so on for the six-month and 12-month and year-ago readings. All the data are consistent except that the headline trend does not refer to quite the same period as the detail.

Spain offers a very early read on inflation in December. The headlines of the HICP and CPI show a spurt in progress with a nearly 1% gain (0.8% and 0.9%, respectively) in the HICP and CPI readings in the month of December alone. These compare to gains of 0.1% in the HICP and of 0.2% in the CPI in November. December readings exist only for the two headline series. In the table, we have placed the detail data in columns with a one-month lag. The three-month gain for the headline series is for the period ended in December; for the detailed categories and the core readings it will be for period ended in November and so on for the six-month and 12-month and year-ago readings. All the data are consistent except that the headline trend does not refer to quite the same period as the detail.

Both of Spain's headline series show accelerating inflation from 12-month to six-month to three-month. In fact, 12-month inflation is accelerating for the second year in a row.

The headline shows inflation accelerating over the last several months while the core (which is only up-to-date through November) does not show such acceleration in gear. It looks as though inflation is substantially a product of energy prices. As of November, the core reading is not showing acceleration. We execute diffusion data for the CPI categories and find that inflation acceleration across categories is mild (at 60%; where 50% is dead neutral) for 12-month (vs. 12-month ago) and six-month (vs. 12-month) and that over three-month (vs. six-month) there is mild deceleration (diffusion = 40%).

The energy price problem

There is a theme we will have to keep in mind. It is that headline inflation is going to reflect the gain in energy prices while the core may not. And that could become a problem for policymakers especially those that think forbearance of accommodative monetary policy has been overdone. Many do think that accommodative policies have overstayed their welcome and will be looking to get policy metrics back to at least neutral as soon as possible. But if the only inflation is in energy prices and if inflation elsewhere is still tame, a premature withdrawal of this monetary stimulus could weaken growth. Energy might put the wrong signal in play through the headline.

ECB girds for conflict

Jens Weidmann is already girding for battle on this issue. He has already reminded the ECB that its mandate is to make monetary policy solely on the basis of inflation. The 'arithmetic' of inflation is going to be on Jens' side when it comes time to argue policy at the ECB, but I'm not so sure that the economics of it all is going to be on his side as well. However, thanks to the ECB's narrow mandate, he only will need to get the arithmetic on his side.

Spain's trends are not in isolation

Spain is an early inflation reporter and it puts these trends on the table. I suspect it will not be alone in showing this set of data. Even in the U.S. where inflation-targeting shares the limelight with a full employment mandate, the FOMC has been looking ahead and seeing the ghost of Christmas-future...I mean of course of inflation-future. On this basis, the Fed is now hiking rates and 'plans' three more rate hikes in 2017 (if the data-gods are willing).

Inflation targeting: as much science as black-magic

The issue of inflation targeting is still more art than science. I say that because the ECB mandate is for inflation a bit less than 2% and not well specified beyond that. The Fed - I contend- does not really have a real inflation target, but it says that the economy operates best with inflation at 2%. In the case of the ECB, because of this long period of undershooting, it could have inflation above 2% for a while and looking back find it had still 'achieved' its mandate. But there is no provision for this sort of policy. The ECB is not on a price-level targeting rule that allows or requires it to get inflation back to the 'just under 2% mark' once it has undershot. In short, undershooting is no excuse (or justification) for subsequent overshooting. But some policymakers may 'feel' differently about it. For example, some might be more willing to 'risk' an overshoot because there has been such undershoot. That would be different from targeting an overshoot, but the result might not be very different.

Inflation 'targeting' in the U.S.

In the U.S., the issue is even more complicated. The Fed has not committed to reach its inflation 'target' over any horizon. Moreover, it offers up forecasts for the PCE as well as for the core PCE muddying the water on what it is actually targeting (let alone 'when'). From time to time, FOMC members will shift from speaking about one price measure to the other (core vs. headline) depending on the condition they seek to highlight and the policy tilt they already endorse. This, of course, has things backwards and is another example of how targeting has gone amok. Some members have even tried to reference the CPI's behavior when arguing for monetary policy changes; but that index is irrelevant. Ignored in all, this is the fact that the PCE has been in a long period of undershooting by both its headline or core measures. Calculating inflation back as far as 25-years ago to date - and for all shorter year-to-date periods- U.S. inflation by the core or headline PCE comes up as less than a compounded annual rate of 2%. The U.S. has been inflation-compliant even before it had a rule to comply with! While inflation targeting in the U.S. has not been in place for that long, inflation performance actually conforms to the Fed's inflation rule over the past quarter century. Still, the Fed, acts as though there is some inflation pick up ready to load up and seems to feel that policy has to get out in front of that despite 25 years of 'success' and a small net undershoot.

Rate targeting and forecasting

The Fed itself has had an abysmal forecasting record in this economic expansion. Still, it insists on making policy looking ahead. Based on its current view, it sees inflation returning to 2% and some see inflation rising more strongly requiring even more than three rate hikes in the year ahead. But the fact that inflation has no domicile in time saps that 'target' of any real meaning. Shooting at a target that you imagine in the future is just an excuse for making it up as you go along. In a world of complete credibility and excellent technical competence, that might not be so, but this world is not such a world. And making policy today for the unknown future even based on a best 'scientific estimate' simply is not good enough because of the still-present risks. Our economy is on a very narrow isthmus that separates 'too much' from 'not enough' and committing too soon in the wrong direction could create a lot of trouble.

2017 Beckons...

On balance, that is the sort of decision process and dilemma that central banks will be facing in 2017. Perhaps conditions will clarify themselves sooner and make a real policy commitment less dangerous and the true path clearer. For now markets are optimistic and the future holds hope, both in the U.S. and Europe. But globally all economies show a good deal of risk in the mix from China to Japan to Europe to the U.S. And the geopolitical situation could become more difficult. China is already back on its heels and complaining about U.S. actions. On his way out, Obama has slapped new sanctions on Russia. Secretary of State Kerry has made some disparaging remarks about Israel that the Brits have said are out of bounds. There are concerns about what the Trump view is of the U.S. relationship to Russia. The U.K. and E.U. have a drawn out Brexit process to sort out. Other European countries are less than pleased with European policy, but defecting from EMU is still not in the cards despite their disenchantment. Apart from its geopolitical snit with the U.S., China has economic issues and U.S. firms operating in China could yet become pawns in any U.S.-China confrontation. We still have a lot on our plate in 2017, plus upcoming European elections. Confrontations over central bank policies may in the end not loom as some the biggest issues that markets will have to face in 2017. We may sit there thinking that we are waiting for the 'ball to drop' on New Year's Eve when we are really just waiting for the other shoe to drop...

Happy New Year!

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief