Global| Jan 31 2017

Global| Jan 31 2017Seven-Year Low (Unemployment) Meets Four-Year High (Inflation); What's a' Matter? Matter Meets Anti-Matter

Summary

The European Monetary Union (EMU) is at one of those crucial policy crossroads where priorities begin to shift. So far, the ECB is holding fast onto its old program of economic stimulus. But unemployment has now fallen to a seven-year [...]

The European Monetary Union (EMU) is at one of those crucial policy crossroads where priorities begin to shift. So far, the ECB is holding fast onto its old program of economic stimulus. But unemployment has now fallen to a seven-year low and inflation is up to a four-year high and the policy priorities of the ECB may be shifting or about to shift.

The European Monetary Union (EMU) is at one of those crucial policy crossroads where priorities begin to shift. So far, the ECB is holding fast onto its old program of economic stimulus. But unemployment has now fallen to a seven-year low and inflation is up to a four-year high and the policy priorities of the ECB may be shifting or about to shift.

Unemployment convergence and divergence

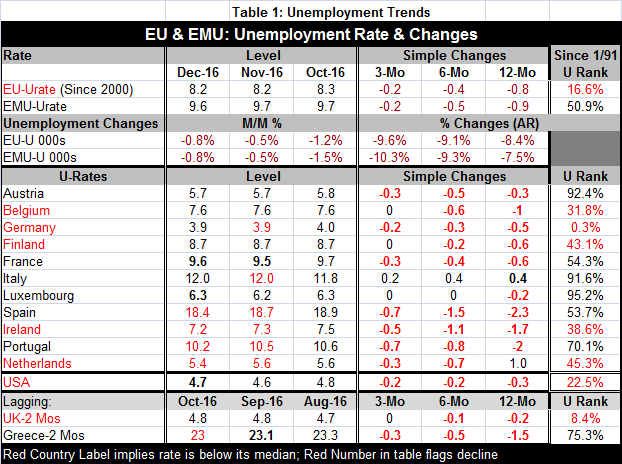

The unemployment rate in the EMU has been falling. For five of the 11 original EMU members in the table, unemployment rates are below their medians; four have unemployment rates that have dropped this month. The unemployment rate for the whole of the EU region is below its median, but for the EMU it is not yet below its median but it is close (it resides at its 50.9 percentile; its median occurs at its 50th percentile). Three EMU members still have unemployment rates that have been higher since 1991 only 10% of the time (Austria, Italy and Luxembourg; Italy is the third largest economy in the EMU and it matters). Portugal's unemployment rate has been higher 30% of the time. Spain and France have rates only slightly above their respective medians. Still, it is clear that based on unemployment rates a good number of EMU nations would not be prepared to see rates go higher just yet.

The ECB and its mandate- a simply story

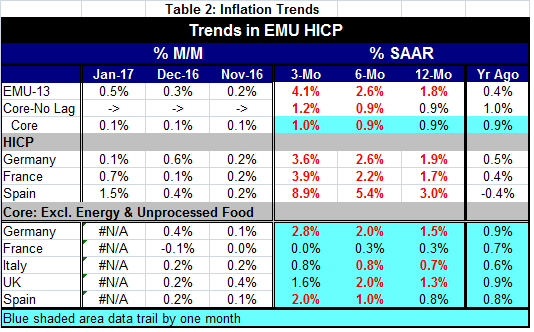

The ECB is a central bank with only an inflation mandate so with the headline HICP now with a gain of 1.8% over 12 months is arguably close to or at its pricing objective and further pressure on prices would put it over the top and in all likelihood put pressure on the bank to cease its easing programs and do a 180 degree switch to fight rising prices. Or maybe not, if the story goes beyond simplicity.

ECB Mandate - a more complex reality

Inflation data for the EMU are not yet available for all individual members nor are core or ex-energy prices yet available on that basis. But the overall core rate introduces a complexity to the above simple story. That complexity is that energy is mostly pushing inflation up. You may have seen the morning headlines about how inflation is higher and rising and at multi-year highs across many countries of the euro area. But overall core inflation is still running at a pace of less than 1% over 12 months less than 1% over six months and has stepped-up to just 1.2% (compounded) over three months.

Despite the clear acceleration of headline inflation in EMU and across its members Mario Draghi, ECB President, has cited this pressure as due to rising energy prices and has distained calling it a true rise of inflation. For that reason, he says he sees no real inflation or reason to alter ECB monetary policy.

Throwing down the gauntlet

We can expect to see fireworks over this interpretation soon. For one, the core rate is not what is targeted by the ECB. For another, the headline is the only rate that the ECB focuses on and there has been no tradition at the ECB (or Bundesbank before it) for cutting a special inflation deal because the forces of headline inflation seemed to be temporary. If headline inflation is temporary, then any tightening will be temporary. Although in the financial crisis the U.S. was able to persuade the ECB to take some solace from sinking global growth conditions to ease rates ahead of inflation breaking because it was at that time so clear that inflation was in fact being under mind even as it lingered too high after spurting on a surge in global oil prices that shift was unusual. The ECB now finds itself in uncharted waters and the Germans are anxious since inflation in Germany has more substance than elsewhere and is rising faster. Table 2 uses lagging data on the core HICP to demonstrate that German core inflation is rising faster than it is in the other large EMU and EU economies.

ECB policy discourse: don't fence me in...

Of course, the ECB was modeled after the Bundesbank in all its respects. If the German's were making policy, rates would already be higher since oil prices on world markets are rising and inflation in Germany is uncomfortable. But the ECB makes policy for all of the EMU not just Germany and Draghi is using an interpretation of inflation (lasting vs. transitory) that will put him on the hot seat and in opposition to the other hard money members of the ECB council. The ECB is coming into one of its most difficult times. Certainly policy-making in the teeth of the financial crisis and slowdown was a problem for the bank but the need for action was clear and even though Germany dragged its feet in opposition to nearly all of the stimulus moves eventually they were adopted by the ECB making stimulus later and less effective. But Germany ultimately did give in. We might expect a parallel opposition to rate hiking this time with rising inflation eventually calling the tune to which the ECB will have to dance. The inability of EMU members to look clearly a the challenges they face because they look through the lens of ideology and the rigid way in which policy has been made under the ECB charter so constructed by German influence has not served EMU well. The German belief that low and stable inflation is the bedrock of any economy and of successful growth got in the way of the bank seeing and reacting to other risks. And that belief and defense of it helped keep the ECB from reacting in a timely fashion to the opposite threat of deflation when it emerged. And that, arguably, is a contributing factor to current economic under-performance. Now with inflation rising in a one dimensional way, the ECB again finds itself in an awkward spot with same old opposition lined up in familiar places on opposite sides of the fence. Who said 'good fences make good neighbors?' It may be true, but fences make poor colleagues.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief