Global| Aug 05 2013

Global| Aug 05 2013Services Metrics Show Weakness in the Periphery

Summary

The chart plots the course of the services PMIs for the European monetary union versus three of the BRIC countries: India, China and Russia. It shows that the developing economy service sectors have tended to be stronger than Europe [...]

The chart plots the course of the services PMIs for the European monetary union versus three of the BRIC countries: India, China and Russia. It shows that the developing economy service sectors have tended to be stronger than Europe over most of their history. However, recently things have begun to change.

The chart plots the course of the services PMIs for the European monetary union versus three of the BRIC countries: India, China and Russia. It shows that the developing economy service sectors have tended to be stronger than Europe over most of their history. However, recently things have begun to change.

In the European Monetary Union there is a rebound in the services sector a foot. However, in India, China and Russia as well as Brazil, which is in the table but not on the graph, the service sector is beginning to slip.

The usual premium of the services metric in the BRIC countries to the European Monetary Union is slipping away. We have seen this premium shrink on several occasions in the past.

In 2006 the European Union was improving sharply. It closed the gap on the BRIC countries by rising while they were more or less moving sideways at a relatively strong pace.

In 2008 to 2009 weakening activity cause the BRIC countries to plunge faster than the European Monetary Union's measure as both were falling in the global recession. At that time, the gap was reversed except for China.

In 2010 there was some brief weakness in the BRIC countries while EMU remained steady; that compressed the gap and that situation repeated itself in 2011, briefly.

However, for much of 2011 to date the European Monetary Union nurtured a weak services sector while the BRIC countries have been sailing along, showing expansion rates above 50 but below what had been their historic norms for the most part. Now, the weakness of the BRIC countries is beginning to take more of a toll as the decay in their services sectors is being more persistently revealed.

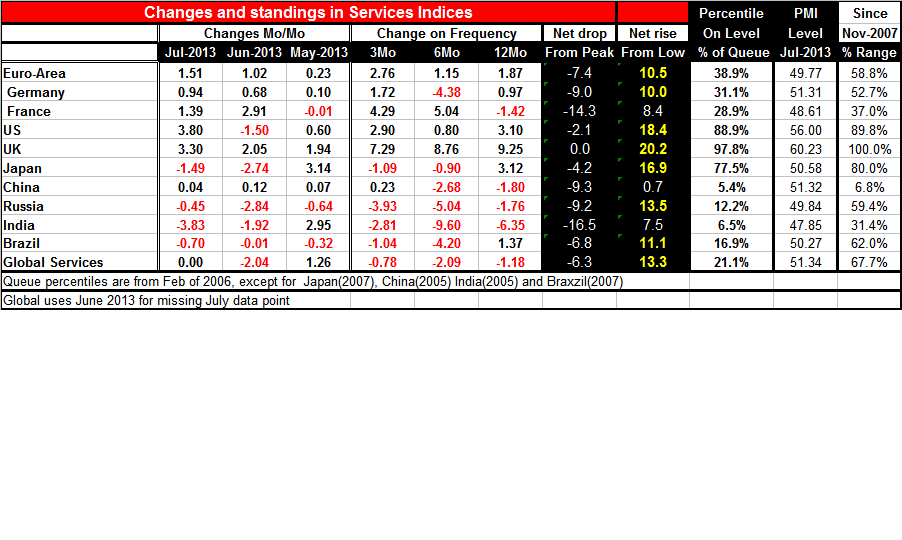

The table gives us a bit more in the way of specifics. If we look at the drops that we've seen in these various countries since roughly the onset of the financial crisis and global recession from November 2007 onward, we see the countries with the biggest service sector drops from their respective peaks are India, followed by France, followed by China and Russia; the euro-Area as a whole comes next and then Brazil.

However, in terms of increases from their lows the best-performing economy is the UK which is up by 20 points from its low followed by the US, followed by Russia and then by the global economy and finally Brazil. China, at a queue ranking value at the 0.7 percentile, is actually quite close to its cycle low (within one percentage point). China had been able to fight off much of the weakness in the financial crisis but now is finding itself becoming entangled in the difficulties of getting growth going in a slow-growth world. The advanced economies are beginning to create blowback effects on the Chinese economy which is so dependent on demand in countries overseas and is desperately trying to shift its economy to reduce that dependence.

When we assess the percentile standing of the sectors since November 2007 the best-performing economy is the UK, followed by the US. The BRIC economies wind up at the bottom with China in the bottom 5% of its range, India the bottom 6.5%, Russian the bottom 12%, and Brazil in the bottom 16 to 17 percentile of its historic queue. As a whole, the euro-Area is in roughly the bottom 40th percentile of its queue compared the 20th percentile globally (for the global metric we are using the June value for July since July is not officially in).

For a while the developing economies as well as the peripheral countries in the European monetary union were starting to improve from their lows and looked as though they beginning to outperform the core countries in the European monetary union. However, that brief episode is past and now it looks like the more industrialized, stronger countries that have been able to use monetary policy and their reserve currency status to pull themselves up by their bootstraps are now the ones that are doing better.

Part of this I think is to acknowledge that the developing economies in the past were able to improve their economies by hitching their wagons to domestic demand in the strong countries of the most advanced economies by running trade surpluses with them. With weaker demand in the advanced economies the developing economies are having more difficult time. They are probably going to be further pressured to reduce their historic tendency to run trade surpluses. While this is a story principally about the traded goods sector, there are clear implications for the economy as a whole and you see the response by looking at the services sectors which largely consist of nontradable goods. Perhaps the developing nations should seek to stimulate their services sectors to reignite growth in their manufacturing sectors instead of sitting around waiting for the business cycle to turn up in the advanced economies. The game of export-led growth no longer looks like it will play out in the future as profitably it had in the past.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief