Global| Oct 31 2007

Global| Oct 31 2007Sentiment Slips but Flash Inflation Flares

Summary

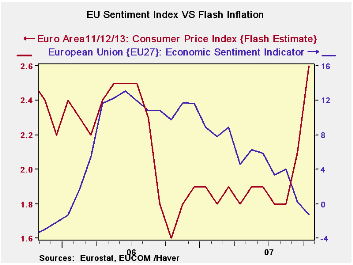

Flash flare does not seem to be part of trend Wake up call or wrong number? The survey on flash inflation for the EMU region does not appear to be part of a trend. Indeed with the euro rising, the only real impulse to inflation right [...]

Flash flare does not seem to be part of trend…Wake up call or wrong number?

The survey on flash inflation for the EMU region does not appear to be part of a trend. Indeed with the euro rising, the only real impulse to inflation right now is from commodity prices and since they are priced in dollars even that channel is muted.

The jump in the flash HICP seems to be just a flash in the pan but it’s a pan with explosives in it since the flash has made a huge impact. On a day when the EU Commission indexes show widespread losing in the Euro area and Draghi and Liikanen have made statements about the coming adverse impact on growth. On a totally different track, the BKK’s/ECB’s Weber has cautioned that the pressures on prices could force the ECB to act again to quell rising inflation pressures.

The table below shows the relative trends. There are only three new observations for October for the flash overall rate and the overall rates for German and Italian inflation. For the others, trends derive from prices in September. Through that point there is no solid evidence of inflation spiking or even gradually rising. But Italy and Germany do support the acceleration in the overall rate in October.

There is no core rate to look at to infer what the culprit was in creating price pressures. But there is little evidence of inflation building in the pipeline. In the Euro area 13 both goods and services prices have been pushed to lower rates of increase by the rising euro. For goods the strong euro is at work as the new three-month inflation rate through September is only 0.1% down from inflation in the area of 2% previously. Service sector inflation is at 2.1% for three months up from 2% over six months but down from 2.6% Yr/Yr. In short the 2.6% Euro area flash CPI may be a wake up call but it may also be a wrong number.

| Trends in HICP | |||||||

|---|---|---|---|---|---|---|---|

| % mo/mo | % saar | ||||||

| Oct-07 | Sep-07 | Aug-07 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EU-13 | #N/A | 0.4% | 0.0% | 1.8% | 2.5% | 2.1% | 1.7% |

| Core | #N/A | 0.2% | 0.2% | 2.1% | 2.0% | 2.0% | 1.5% |

| Goods | #N/A | 1.0% | 0.0% | 0.1% | 2.2% | 1.9% | 1.6% |

| Services | #N/A | -0.5% | 0.2% | 1.8% | 2.5% | 2.5% | 2.0% |

| FLASH - | 0.2% | 0.2% | 0.2% | 2.1% | 2.0% | 2.6% | 1.6% |

| Monthly Flash data are derived from Yr/Yr presentation | |||||||

| HICP | |||||||

| Germany | 0.2% | 0.7% | -0.1% | 3.1% | 2.7% | 2.7% | 1.1% |

| France | #N/A | 0.1% | 0.3% | 1.8% | 2.7% | 1.6% | 1.5% |

| Italy | 0.7% | 0.3% | 0.2% | 4.7% | 3.3% | 2.3% | 1.9% |

| UK | #N/A | 0.1% | 0.1% | -0.4% | 0.6% | 1.7% | 2.4% |

| Spain | #N/A | 0.4% | 0.0% | 2.3% | 2.8% | 2.7% | 2.9% |

| Core Excl Food Energy & A | |||||||

| Germany | #N/A | 0.3% | 0.1% | 2.4% | 2.6% | 2.3% | 0.8% |

| France | #N/A | 0.1% | 0.3% | 2.0% | 2.0% | 1.6% | 1.2% |

| Italy | #N/A | 0.4% | 0.2% | 2.3% | 1.8% | 1.8% | 2.0% |

| UK | #N/A | #N/A | 0.2% | #N/A | #N/A | #N/A | 1.6% |

| Spain | #N/A | 0.2% | 0.3% | 3.0% | 2.7% | 2.6% | 3.0% |

| Blue shaded area data trail by one month | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief