Global| Nov 02 2016

Global| Nov 02 2016Selected Japan Indicators Show Stagnation

Summary

With the Bank of Japan holding its fire in its recent meeting, Japan's economy continues to give off very muted signals. Annual growth rates for traditional indicators such as retail sales, industrial production, exports and [...]

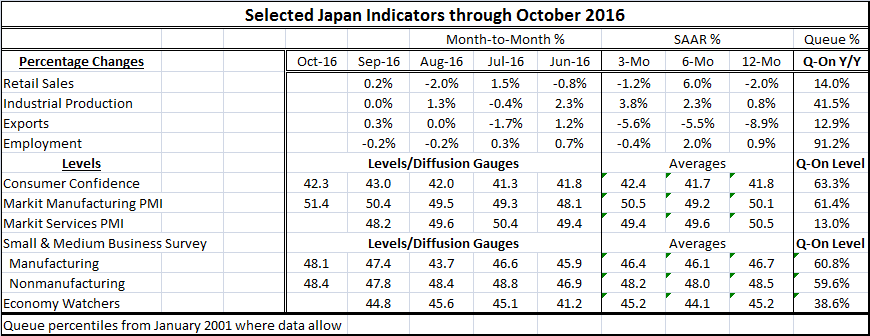

With the Bank of Japan holding its fire in its recent meeting, Japan's economy continues to give off very muted signals. Annual growth rates for traditional indicators such as retail sales, industrial production, exports and employment are modest or low except for employment. Retail sales and export growth are each lower less than 15% of the time. IP is weaker only 41% of the time. But job growth is strong. Even with a slowing and shrinking population, employment is still strong by historic standards.

With the Bank of Japan holding its fire in its recent meeting, Japan's economy continues to give off very muted signals. Annual growth rates for traditional indicators such as retail sales, industrial production, exports and employment are modest or low except for employment. Retail sales and export growth are each lower less than 15% of the time. IP is weaker only 41% of the time. But job growth is strong. Even with a slowing and shrinking population, employment is still strong by historic standards.

Gauged in terms of level of the diffusion reading on confidence and manufacturing, both up-to-date through October, conditions in Japan are modestly firm with a low 60th percentile standing. The PMI for services (September) is much weaker with a 13th percentile standing. This standing is more or less in line although clearly much weaker than the economy watchers index which is also a service sector barometer. That index also is up-to-date through September. The economy watchers index has a below median standing at its 38th percentile. So both of these gauges see some weakness in services but one sees more weakness than the other.

The small to medium business surveys for manufacturing and nonmanufacturing firms have a standings in their respective 60th percentile; they are close to the Markit reading for manufacturing and not as weak as the services PMI and also substantially stronger than the economy watchers' standing.

Still, the picture from Japan is not pretty or encouraging. Among the growth rate indicators, all are slipping or losing momentum except IP where output gains do show acceleration. But the Markit diffusion gauge on manufacturing is stuck around the neutral score of 50; that is it has been stuck there, until this last month. Its step up will be a nascent trend to watch. The services diffusion index also has been stuck and in its case, it has been stuck below 50, showing contraction. The economy watchers (diffusion) index also has been logging values below 50, signaling ongoing service sector contraction. The small and medium-sized business indictors are signaling somewhat firm readings (60th percentile) compared to their past history. But both of these diffusion indices are below 50, signaling ongoing contraction. There is simply too much contraction or slowing signaling here to be ignored.

All of these trends make it a bit hard to understand where any firmness in growth is going to come from. The BOJ is holding its fire for now. And it may not have the most potent tools left to use. But what Japan needs to restore growth very clearly is something even if monetary policy tools are not the right stuff. A shift in social policy to favor more births, more immigration or to encourage women to develop business careers to boost labor force growth all are examples of shifts that could help to spur growth. But none of these actions are on the menu. Japan seems to like its culture as it is and is trying to make the best of an economic situation that continues to embrace the traditional values in Japan. The eventual question that Japan fails to address with this policy path is that if Japan is going to be content to shrink; how long it will be before it stops shrinking since long-term shrinking is not a viable strategy. And how is Japan, in the meantime, going to handle its large debt burden?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief