Global| May 17 2017

Global| May 17 2017Rethinking EMU Inflation and Beyond

Summary

Were the Bundesbank alone in the EMU, there would be no rethinking of anything. The Bundesbank and the Germans are sure that they already know it all and they have no doubt about that. When it comes to running policy in Germany, I [...]

Were the Bundesbank alone in the EMU, there would be no rethinking of anything. The Bundesbank and the Germans are sure that they already know it all and they have no doubt about that. When it comes to running policy in Germany, I don't doubt that they are right.

Were the Bundesbank alone in the EMU, there would be no rethinking of anything. The Bundesbank and the Germans are sure that they already know it all and they have no doubt about that. When it comes to running policy in Germany, I don't doubt that they are right.

On being not the Bundesbank

But the European Central Bank is a hybrid. And as much as it was created in the image and likeness of the former Bundesbank, the Bundesbank it is not. Even with the Bundesbank's single minded one-pillar objective as its foundation, it is still not the Bundesbank.

Good fences do not make the neighbors good

The Bundesbank had one 'client'; the ECB has 19. And while we think of central banks - and certainly the Bundesbank- as being independent, the number of clients makes a difference that is significant. As we watch the restive populace in Europe, and the U.K. departure from the EU, it should be very clear that rules alone do make a monetary union (or a customs union). Good fences may make good neighbors, but good fences do not make your neighbors good.

Power from the people!

In truth, the Bundesbank gets its power from the people and from German history and its experience with hyperinflation. This is not so much of a shared experience across the 19 members of the EMU. And while the Bundesbank and its policy results are much revered, everything has its limits. There is also the fact that the formation of the EMU and the obliteration of national currencies has not erased borders or dulled cultural differences. There is no shared fiscal policy and he only fiscal pooling that occurs is through dues paying to support the structures needed to run the EU apparatus and the self-funding of the ECB. Basically, we can assume that the rest of Europe hoped to get excellent monetary management at a lower price than what they have had to pay. Good policy output requires good input. You can't have bad economic input and turn it into good monetary policy at a low cost. That expectation was not realistic. And the ECB was instituted only to create an 'output' (steady inflation) and there was nothing really disciplining internal results to help achieve that goal outside of weak and formerly unenforced Maastricht guidelines on fiscal policy.

Germany clings to its lead

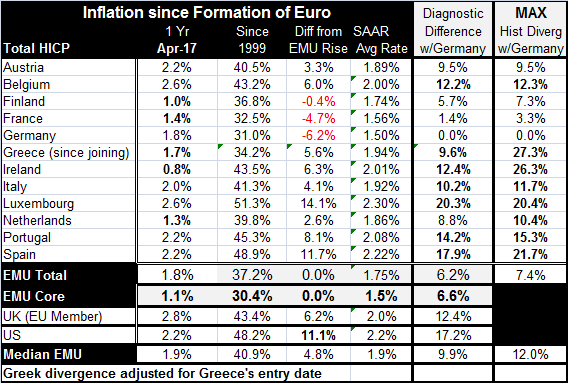

The fact is that Germans retain this fear of inflation. That has meant that policy in Germany has been run to keep inflation even lower than in the rest of the EMU. The table shows that the German price level rise (and average inflation rate) has been lower than other members' rates. One consequence of that is that Germany has become even more competitive than the rest of the EMU. And those who strayed and did not rein in inflation have been forced through a gristmill of austerity to wring the excess out and bring them back to the fold. Greece's once 27% price level disadvantage with Germany has been reduced to 9.6%. It is now on a par with Italy and Austria. Luxembourg remains and unrepentant outlier, but as a financial center, that matters less. Ireland has made great changes. Spain has made some change and still has a way to go.

The core

We can also calculate core inflation differences; these, actually, are even worse. For the EMU as a whole, core inflation shows all of the EMU at an even slightly greater disadvantage to Germany as the EMU wide core difference with Germany is 6.6%, compared with 6.2% for headline inflation. (The comparison here is understated since Germany has a huge weight in the EMU scheme of things the rest of EMU is even farther behind Germany as we see in the individual comparisons for the headline.) The Bundesbank never made policy on core inflation. Inflation is inflation is inflation. But with 19 clients to serve, Draghi has drifted over to the core measure at least implicitly. With the ECB's headline inflation arguably at its objective of inflation just less than 2% (1.8% year-on-year), the core still has not caught up. The core is not there. It has not been there. The core is not close enough even in a game of horseshoes and hand grenades. At 1.1%, inflation is still far below 2%. Moreover, if you look at the core on the chart, the core has been sagging. Its trend is lower- unlike for headline inflation. Why does this matter?

Looking for an answer...a scape goat

With economies underperforming, economists are looking for solutions and for scapegoats. And if it is really true that the economy grows 'best' with inflation at 2%, the central bank better make sure we get 2% inflation. This is more the mantra of the Fed. In Europe, just under 2% is simply 'The Target' and not the holy grail for growth. But as core inflation lingers well below the headline at a time that growth is not substantial, that same question will percolate in Europe. If the goal for inflation is 2%, why do you let the core run so cold?

Germany: running hot at low temperatures

Germany has an economy geared to run hot at low temperatures. By that, I mean to point out that Germany's economy is not hurt by low inflation. Its structure and the support from its people are still there and it is actively supported at low levels of inflation. That is not so in other countries where low inflation creates more anxiety and is more of a problem for growth.

The great manipulation: Germany vs. EMU

Germany has kept is headline inflation at a 1.5% compounded pace since the EMU was formed; this is against an EMU-wide target of just under 2%. The EMU actual inflation rate has averaged 1.75% since the EMU was formed with a core that has averaged 1.5%. On this same timeline, the German compounded core rate has averaged 1.24%. Germany has steaked out the low ground and this puts more pressure on its fellow EMU members who lose competiveness with Germany if they don't 'keep-down' (a variant, you may recognize, of 'keeping up').

Some ARE more equal than others

In essence, Germany's unilateral decision on inflation constrains all of the EMU and has played a role in reducing the profile of EMU inflation possibly to a pace that is unhealthy for growth for Europe even if that is not true for Germany. Now that EMU members have had their run-in with going their own way, I presume individual members will be a little less eager to run unilaterally stimulative policies knowing that there will be a price to pay for them down the road. The best speed is to match Germany's speed which would require a lot of change since the speed for German inflation comes from an economy with a very different structure built on very different values than the rest of Europe.

Draghi gets it

Draghi implicitly understands this when he says that there is no evidence of widespread inflation, he is chalking up the headline HICP rise to oil prices and noting the weakness in the core.

Coming to grips with the unintended impact of policy goals and structural defects

But this is something that central banks, not just the ECB, have to come to grips with. Have their policies resulted in a grip that is too tight? Is Germany's single-minded focus on having the lowest inflation rate in the EMU healthy or selfish? Wherever the euro exchange rate goes because of the performance of German inflation, Germany will always be the most competitive country in the EMU. That's what the smallest price gain means. So if this is Germany's way of running policy, is it selfish because everyone can't do it...only one can. That means Germany has nothing to teach anyone about good policy. Of course, Germany's massive current account surplus speaks to how well this has worked for Germany and also illustrates how German success comes at a cost to others since they must run the counterpart deficits.

The Trump effect

If there is one good thing that has come of Trump upsetting the trade apple cart, it is that it has finally exposed some of these policies to closer scrutiny. Trade is not free or fair just because you sweep away barriers. Trade must occur at market-determined prices using market-determined exchange rates and this is where things get dodgy. Germany has engineered a situation in which it is always nested in the most competitive slot in the EMU. That is to the detriment of its fellow EMU nations but has broader trade consequences as well. All this is a reminder that economies are general equilibrium systems and all the moving parts must mesh together. If they don't, there is trouble or at least action and reaction. And central banks are simply trying to engineer the monetary policy that accommodates the best economic functioning. That's hard to do in a monetary union when some members are manipulating the monetary system to their own advantage.

More broadly

The broader implications are that central bankers may want to actually expend more effort on studies that look at how low inflation might impede growth. The literature so far is essentially focused on inflation expectations and about how variable, unexpected or high inflation can be debilitating. But what about inflation that is too low? Is there such a thing as being too rich, too thin, or having inflation too low? We have discovered anorexia. We know there is fallout from greed and yet the U.S. income distribution continues to become more concentrated. What about inflation? Inquiring minds want to know? Can it be too low? If so, on what measure?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief