Global| Nov 25 2015

Global| Nov 25 2015Retail Sales Growth Turns Negative In September

Summary

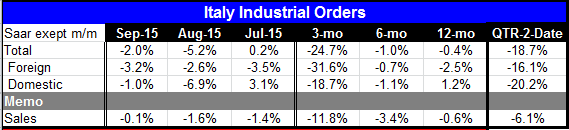

Retail sales volumes and consumer confidence in Italy have recovered much better than has the Italian industrial sector. Italian orders fell for the second month in a row. Italian foreign orders have fallen in each of the last three- [...]

Retail sales volumes and consumer confidence in Italy have recovered much better than has the Italian industrial sector. Italian orders fell for the second month in a row. Italian foreign orders have fallen in each of the last three-months, and in four of the last five months. And, while, Italian retail sales have fallen in September they are up by 1.5% over 12-months. The industrial weakness has not yet hit retailing hard.

Retail sales volumes and consumer confidence in Italy have recovered much better than has the Italian industrial sector. Italian orders fell for the second month in a row. Italian foreign orders have fallen in each of the last three-months, and in four of the last five months. And, while, Italian retail sales have fallen in September they are up by 1.5% over 12-months. The industrial weakness has not yet hit retailing hard.

Italy is still struggling. Like much of the rest of Europe, its manufacturing sector continues to do worse than its domestic sectors.

Italian industrial orders show extreme weakness with accelerating declines over more recent periods. In the quarter to date overall orders are falling at an 18 percent annual rate. Foreign orders are falling at a 16 percent annual rate compared to domestic orders falling at a 20 percent annual rate. Domestic orders, orders that are very weak in the quarter-to-date, have only begun to show greater weakness than foreign orders.

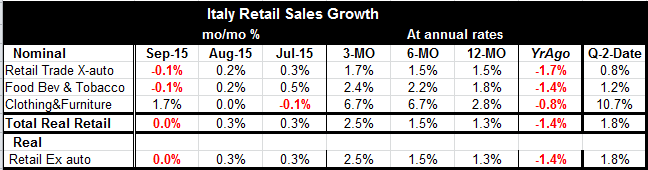

Italian retail sales are growing but are not prospering. Sales fell by 0.1% in September after rising by a meager 0.2% in August. Three month growth at 1.7% is marginally above its 6-month pace and 12-month pace of 1.5%. But in the quarter to date sales are up only at a 0.8% pace.

Italy's foreign order weakness comes despite a substantially undervalued euro exchange rate. Easy ECB monetary policy and its debilitating impact on the EMU exchange rate have not been able to resuscitate the moribund Italian economy or to breathe new life into its manufacturing sector. Italy remains weak despite some improvement in consumer confidence and expanding, but weak, retail sales. Its pursuit of austerity has dominated any attempt to restore growth to its former pace.

The ECB is preparing to launch further monetary accommodation and it is expected to be announced at its upcoming December meeting. Italy needs further stimulus but it is not clear that further ECB accommodation will be the right ticket for Italy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief