Global| Jul 21 2006

Global| Jul 21 2006Regional Fed Bank Surveys Indicate Slower Growth

by:Tom Moeller

|in:Economy in Brief

Summary

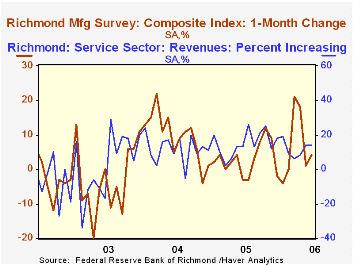

The Federal Reserve Bank of Richmond Mfg. Survey did improve in June, but the low reading of 4 still was down sharply from the highs reached earlier this year. The m/m rise reflected scant improvement in shipments & new orders though [...]

The Federal Reserve Bank of Richmond Mfg. Survey did improve in June, but the low reading of 4 still was down sharply from the highs reached earlier this year. The m/m rise reflected scant improvement in shipments & new orders though the rise in the employment index did raise the 2Q level to its highest since 3Q04.

During the last ten years there has been a 39% correlation between the Richmond survey index level and the one month change in U.S. factory sector industrial production. The latest Richmond Fed Mfg. Survey is available here.

The Richmond Fed also publishes indexes of conditions in the service sector and the revenue measure remained firm in June at a reading of 14, much improved from the lows earlier in the year but below last year's highs. The companion index of service sector employment fell moderately. The latest Richmond Fed Service-Sector Survey is available here.

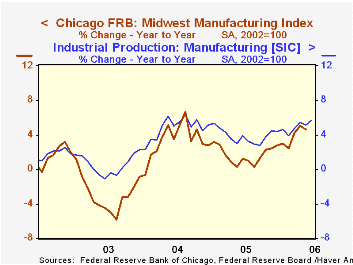

The Chicago Federal Reserve Bank's Midwest manufacturing index fell 0.2% during May from April. It was the first m/m decline in over a year though earlier strong gains left the three month growth rate firm at 5.1%. Three month growth in the index peaked late last year at 9.4%. Declines in indexes covering the machinery & resource sectors were the source of the May drop.

During the last ten years there has been a 95% correlation between the y/y change in Chicago's Midwest Mfg. index and the change in US factory sector industrial production. The May Chicago Fed Midwest Manufacturing Index can be found here.

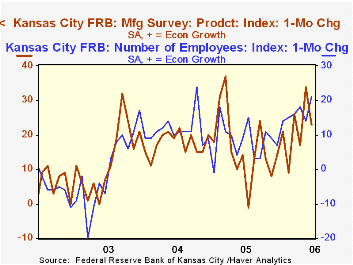

The Kansas City Fed's manufacturing survey included a production index which fell in June to 23 from 34 in May but the level remained quite firm versus last year. Though new orders also fell m/m the quarterly average reached its highest level since late 2003. The index covering the change in the number of employees was its strongest in just over two years. The prices received index also hit its highest level on record.

The Kansas City Fed survey dates back to 2001 and the June release covering manufacturing activity in the Tenth Federal Reserve District can be found here.

The data mentioned here is available in the Haver SURVEYS database.

The Supplier Industry in Transition - The New Geography of Auto Production from the Federal Reserve Bank of Chicago is available here.

| Federal Reserve Surveys | June | May | Year Ago | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Richmond Fed Mfg. Survey (Diffusion Index, 1-Mth. Chg.) | 4 | 1 | -3 | 3 | 10 | -3 |

| Chicago Fed Midwest Mfg. Index (2002 = 100) | n.a. | 106.0 | 101.3 | 102.1 | 100.4 | 97.1 |

| Kansas City Fed Production (1-Mth. Diffusion Index, + = Econ Growth) | 23 | 34 | 14 | 16 | 18 | 13 |

by Carol Stone July 20, 2006

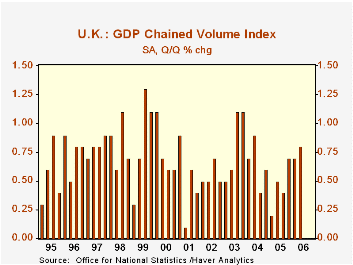

GDP growth in the UK ticked up to 0.8% in Q2 from 0.7% in Q1. The initial report of Q1 in late April was 0.6% so interim revisions were upward, with history also somewhat stronger than was thought at that time.

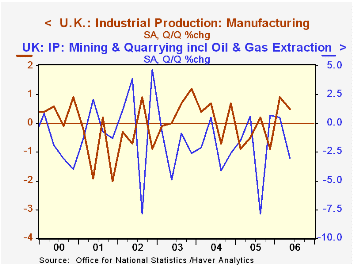

This "preliminary" estimate is compiled from industry data only. The full array of income and expenditure data will be published August 25. Among the sectors, today's report shows that, after a surge in Q1, production industries fell back by 0.1%. This was concentrated in the mining sector (including oil and gas extraction), where output was off 3.0% in the quarter and in energy supply, down 2.8%. However, manufacturing advanced 0.5%; although this was less than in Q1, it added enough to put that sector up 0.7% over a year ago, its first year-on-year increase since Q4 2004.

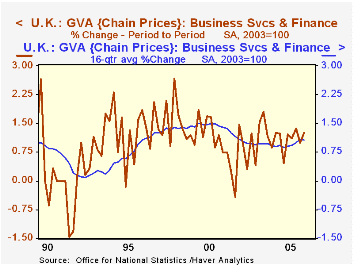

The real source of growth was the services, particularly business and financial services. Total services expanded 1.0%, with business services up 1.2%. This latter industry group is up 4.8% from a year ago. Consumer-oriented services, such as distribution, hotels & restaurants and repairs also gained 1.2% in Q2, yielding 3.3% growth over the past year. Transportation and communications are up 3.0% on the year and government and "other", 2.5%.

We are slightly surprised at this pick-up in UK growth. Just a little over a week ago, we wrote here about employment patterns that were no better than "stable", accompanied by rising unemployment. News reports this morning indicated that forecasters in a widely watched survey had projected 0.7%, the same as Q1, suggesting that our qualitative judgment was hardly unique. The flatness in production was evident from previously available production data for April and May. Just yesterday, retail trade data for the quarter showed strength (2.1%), but that, of course, is only one industry. As we mentioned last quarter, growth in Q1 was widespread across industries, giving the benefits of diversity to the economy as a whole. So this period, when production industries and mining tailed off, service businesses kept up the total.

| United Kingdom (Chained, SA, 2002=100) |

Q2 2006 | Q1 2006 | Q4 2005 | Year/ Year | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|

| GDP* | 0.8 | 0.7 | 0.7 | 2.6 | 1.9 | 3.3 | 2.7 |

| Production Industries | -0.1 | 0.8 | -0.6 | -0.8 | -1.8 | 0.7 | -0.3 |

| Service Industries | 1.0 | 0.7 | 1.1 | 3.6 | 2.8 | 3.9 | 3.1 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief