Global| Jun 13 2007

Global| Jun 13 2007Quite Simply the Retail Data and Trends Tell the Story

Summary

There was a minor upward revision to sales in March. Now in May sales rose by 1.4% and 1.3% excluding motor vehicles. These are strong numbers even when the 3.8% rise in gas station sales is factored out. Virtually all major retail [...]

There was a minor upward revision to sales in March. Now in May sales rose by 1.4% and 1.3% excluding motor vehicles. These are strong numbers even when the 3.8% rise in gas station sales is factored out. Virtually all major retail sales aggregates are gaining momentum after a Q1 lull beset with odd holiday shifts and some unfortunate weather developments.

In the quarter to date total retail sales are rising at a 7.3% pace. Excluding Motor vehicles, sales are up at a 7.9% pace. Excluding motor vehicle sales and gas station sales the pace is at 5.3% and that number will have a very small price deflator associated with it since much of the energy is removed when gas station sales are taken out.

On balance retail sales are NOW strong in the new quarter. Inflation is moderate, so much of this translates into real sales. The overall CPI rose by 0.4% in April when the core rose by 0.2%. Deflating the headline sales pace by 2.5% (annual rate) leaves growth in the range of 4.8% to 5.3% in real terms. It is a good start to Q2 for the consumer - better than was expected. If we take inflation at April’s 0.4% headline pace as the deflator, the annualized overall pace of real retail sales drops to the 2.5% to 2.9% range in Q2 - that is s till very solid and likely an overreaction to inflation’s impact.

|

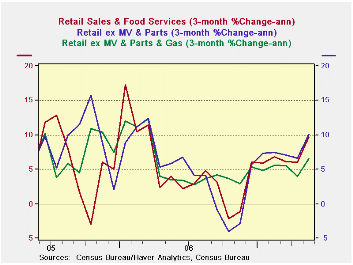

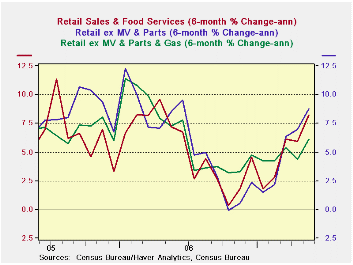

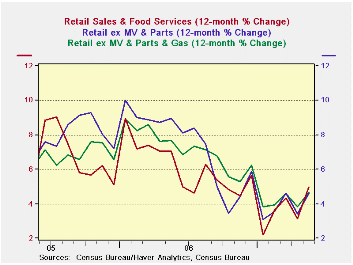

· The growth numbers cut by various retailing segments are universally strong in May and in the three months ended in May. Nondurable goods growth rates, already strong, are accelerating and that is even if gasoline station sales with their energy impact are omitted. Durable goods purchases are strengthening too. Even building materials trends are accelerating. Furniture and electronics sales are a relative laggard in the sector. But the message is pretty clear. The upturn in consumer spending is very, very broad-based in May. And comparisons with 6-month and 12-month trends (see the second and third charts) make it clear that this is not a recoup from a weak patch in earlier months. The strength is real. |

|---|

| Retail: | Mo/Mo | Seasonally Adjusted Annual Rate | |||

| Totals | 2007 May | 3-Mo | 6Mo | Yr/Yr | Yr Ago:Y/Y |

| Retail & Food Service | 1.4% | 9.6% | 8.2% | 5.0% | 7.1% |

| Retail Excl Motor Vehicles & Parts | 1.3% | 10.1% | 8.8% | 4.6% | 9.0% |

| Retail Excl Motor Vehicles & Parts & Gas | 1.0% | 6.6% | 6.1% | 4.7% | 7.7% |

| Retail: | Mo/Mo | Seasonally Adjusted Annual Rate | |||

| Durables | 2007 May | 3-Mo | 6Mo | Yr/Yr | Yr Ago:Y/Y |

| Total-Durables | 1.7% | 6.7% | 5.1% | 4.1% | 3.9% |

| Building Materials | 2.1% | 6.6% | 3.5% | -1.7% | 10.8% |

| Motor Vehicles & Parts | 1.8% | 7.9% | 6.2% | 6.6% | 0.4% |

| MV Dealers | 1.9% | 7.6% | 6.1% | 6.8% | 0.1% |

| Furniture, Electronics | 0.8% | 2.1% | 2.9% | 3.8% | 8.1% |

| Retail: | Mo/Mo | Seasonally Adjusted Annual Rate | |||

| NonDurables | 2007 May | 3-Mo | 6Mo | Yr/Yr | Yr Ago:Y/Y |

| Total-Nondurables | 1.3% | 11.2% | 9.9% | 5.4% | 8.8% |

| Food & Beverages | 0.3% | 5.7% | 6.6% | 6.1% | 4.7% |

| Health | 0.8% | 8.0% | 5.2% | 6.9% | 7.2% |

| Gasoline | 3.8% | 40.6% | 31.4% | 3.7% | 19.0% |

| Clothing | 2.7% | 13.4% | 11.0% | 7.8% | 6.1% |

| Sport Goods | 1.8% | 15.1% | 8.4% | 2.5% | 5.6% |

| General Merchandises | 1.0% | 5.7% | 5.5% | 4.6% | 5.7% |

| Non Store Retailers | 0.1% | 0.0% | 11.2% | 7.7% | 15.0% |

| Miscellaneous Retail | 0.9% | 8.0% | 5.2% | 6.9% | 7.2% |

| Non Durables Excl Gas | 0.8% | 7.0% | 6.8% | 5.7% | 7.2% |

| Services | |||||

| Food Services & Drinking | 0.7% | 9.2% | 5.7% | 5.6% | 8.1% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief