Global| Oct 29 2009

Global| Oct 29 2009Q3 GDP Posts First Gain AfterMore-Than Year Long Recession

by:Tom Moeller

|in:Economy in Brief

Summary

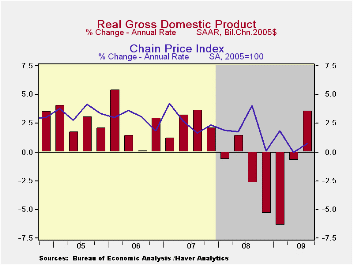

The U.S. economy grew last quarter at hardly a barn-burning rate, but at least it was positive for the first time in over a year. Real GDP during 3Q'09 grew at an expected 3.5% annual rate after a 3.7% decline since late-2007. The [...]

The U.S. economy grew last quarter at hardly a barn-burning rate, but at least it was positive for the first time in over a year. Real GDP during 3Q'09 grew at an expected 3.5% annual rate after a 3.7% decline since late-2007. The rise was fueled by upturns in domestic demand and inventories but lessened by deterioration in the foreign trade deficit. Consensus expectations are that economic growth will continue in coming quarters at roughly a 3.0% rate which, by postwar standards, would be subpar.

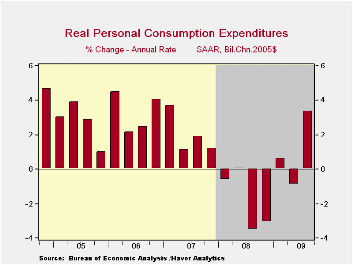

Domestic final demand growth was positive for just the second

quarter since 1Q'08. The upturn owed to a 3.1% gain in consumer

spending (-0.3% y/y) that was led by a 22.8% rise in durables

consumption. The Cash for Clunkers sales incentive program by

auto-makers caused motor vehicle consumption to jump at a 56.4% annual

rate, though it still was up just 1.4% from one-year earlier.

Elsewhere, personal consumption of furniture grew at a 6.4% (-5.9% y/y)

rate following a like downturn during 2Q. Spending on clothing

& shoes fell at a 1.5% (-5.1% y/y) rate while services spending

gained a modest 1.8% (0.4% y/y).

Domestic final demand growth was positive for just the second

quarter since 1Q'08. The upturn owed to a 3.1% gain in consumer

spending (-0.3% y/y) that was led by a 22.8% rise in durables

consumption. The Cash for Clunkers sales incentive program by

auto-makers caused motor vehicle consumption to jump at a 56.4% annual

rate, though it still was up just 1.4% from one-year earlier.

Elsewhere, personal consumption of furniture grew at a 6.4% (-5.9% y/y)

rate following a like downturn during 2Q. Spending on clothing

& shoes fell at a 1.5% (-5.1% y/y) rate while services spending

gained a modest 1.8% (0.4% y/y).

In the fixed-investment side of the GDP accounts, residential

spending also grew for the first time since 1Q'06. The 23.3% rise

(-18.1% y/y) followed a 2Q decline of similar magnitude. During the

downturn, which spanned three years, residential investment fell by

more than one-half. Continuing to the downside at a 2.5% (-18.9% y/y)

rate was business investment. The decline was led by a 9.0% (-20.8%

y/y) drop in spending on structures though equipment spending rose a

modest 1.1% (-17.9% y/y). That increase was led by a gain in

transportation equipment spending (-47.2% y/y) and an upturn in

information processing equipment & software (-6.4% y/y).

Government investment rose at a 2.3% rate (1.8% y/y) led by a gain in

defense spending (5.0% y/y).

In the fixed-investment side of the GDP accounts, residential

spending also grew for the first time since 1Q'06. The 23.3% rise

(-18.1% y/y) followed a 2Q decline of similar magnitude. During the

downturn, which spanned three years, residential investment fell by

more than one-half. Continuing to the downside at a 2.5% (-18.9% y/y)

rate was business investment. The decline was led by a 9.0% (-20.8%

y/y) drop in spending on structures though equipment spending rose a

modest 1.1% (-17.9% y/y). That increase was led by a gain in

transportation equipment spending (-47.2% y/y) and an upturn in

information processing equipment & software (-6.4% y/y).

Government investment rose at a 2.3% rate (1.8% y/y) led by a gain in

defense spending (5.0% y/y).

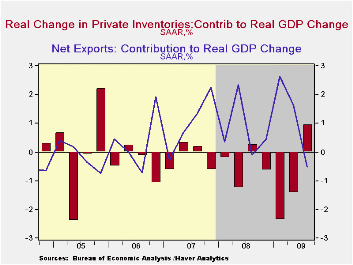

Inventory accumulation made a positive contribution to GDP

growth for just the second time in two years. The modest 0.9% addition

followed subtractions of 1.4 and 2.4 percentage points during the prior

two quarters.

Inventory accumulation made a positive contribution to GDP

growth for just the second time in two years. The modest 0.9% addition

followed subtractions of 1.4 and 2.4 percentage points during the prior

two quarters.

For the first time in a year, deterioration in the foreign trade deficit lowered GDP growth. The 0.5 percentage point subtraction was due to a 16.3% (-14.9% y/y) rise in real imports which outpaced the 14.7% (-11.2% y/y) gain in exports.

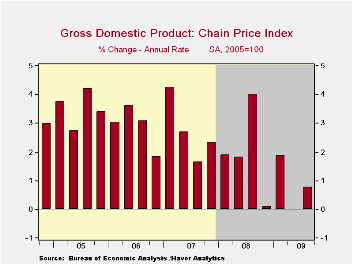

The GDP price deflator rose a slim 0.8%. Though the PCE price index gained 2.8% (-0.6% y/y), the rise in the overall domestic final sales price index was held to just 1.6% (-1.0% y/y) as the fixed investment price index fell sharply (-2.5% y/y).

| Chained 2005$, % AR | 3Q '09 | 2Q '09 | 1Q '09 | 2Q Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| GDP | 3.5 | -0.7 | -6.4 | -2.3 | 0.4 | 2.1 | 2.7 |

| Inventory Effect | 0.9 | -1.4 | -2.4 | -1.2 | -0.4 | -0.4 | 0.1 |

| Final Sales | 2.6 | 0.7 | -4.1 | -1.5 | 0.8 | 2.5 | 2.6 |

| Foreign Trade Effect | -0.5 | 1.7 | 2.6 | 0.9 | -1.2 | 0.8 | 0.1 |

| Domestic Final Demand | 3.0 | -0.9 | -6.4 | -2.4 | -0.4 | 1.7 | 2.5 |

| Chained GDP Price Index | 0.8 | -0.0 | 1.9 | 0.7 | 2.1 | 2.9 | 3.3 |

by Tom Moeller October 29, 2009

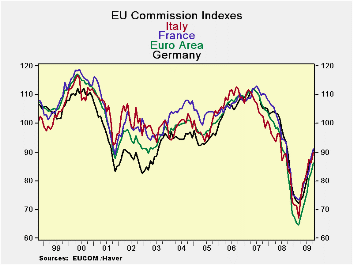

The EU Commission indices made their eight largest advance

Since October 1988 for the EU region as a whole. This boosted the

overall index for the EU to the 46th percentile of range much closer to

its midpoint but still 14% below its average level for the same period.

Surprisingly in relative terms it is the consumer that is

boosting the region the most. Consumer confidence stands at the 50%

mark of its range. Construction lags the most of all sectors, standing

in the 17th percentile of its range followed by services that languish

in the 31st percentile of their range. Both retailing and the

industrial sector are in their respective 41st percentiles.

As to countries, the large countries are clustered closely

together in their respective range readings. Spain is the weakest in

the 38th percentile of its range. Compared to the UK in the 47th range

percentile; among EMU members Italy is the relative strongest in its

42nd percentile leaving a small gap between the best reading and the

worst among large countries in the e-Zone.

Still if we look at the rankings by queue the results are much

weaker. The range ranking positions the current reading between the

highest and lowest range values. The queue orders the various readings

by component or country depending on its application. It ranks them

presenting the result as a percentage (100 is highest). The queue

percentiles show that while the various indicators have come sharply up

from their lows and some although some are closing in on range

midpoints the ranked readings are still no where near normal.

The overall EU reading that stands in the 46th percentile of

its range also stands in the 11th percentile of its queue – a terribly

low standing. The real message here is that yes there is a significant

recovery from the lows in gear but the current levels of the indices

are still well below normal.

While the EU and EMU regions are making progress there is

still a very long way to go.

| EU Sectors and Country level Overall Sentiment | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| EU | Oct 09 |

Sep 09 |

Aug 09 |

Jul 09 |

Percen -tile |

Rank | Max | Min | Range | Mean | By Queue Rank% |

| Overall Index | 86 | 82.6 | 81 | 75 | 46.0 | 222 | 116 | 60 | 56 | 99 | 11.6% |

| Industrial | -20 | -24 | -26 | -30 | 41.3 | 225 | 7 | -39 | 46 | -8 | 10.4% |

| Consumer Confidence | -15 | -17 | -20 | -21 | 50.0 | 188 | 2 | -32 | 34 | -11 | 25.1% |

| Retail Trade | -12 | -11 | -12 | -14 | 41.9 | 215 | 6 | -25 | 31 | -6 | 14.3% |

| Construction | -34 | -35 | -36 | -37 | 17.4 | 216 | 4 | -42 | 46 | -17 | 13.9% |

| Services | -11 | -11 | -11 | -19 | 31.7 | 143 | 32 | -31 | 63 | 13 | 7.1% |

| %m/m | Oct 09 |

Based on Level | Level | ||||||||

| EMU | 4.1% | 2.5% | 6.3% | 86.2 | 41.1 | 222 | 117 | 65 | 53 | 100 | 11.6% |

| Germany | 3.9% | 1.7% | 6.3% | 90.8 | 38.0 | 201 | 121 | 72 | 49 | 100 | 19.9% |

| France | 3.4% | 5.9% | 2.3% | 91.1 | 40.9 | 187 | 119 | 72 | 47 | 100 | 25.5% |

| Italy | 4.4% | -1.5% | 4.5% | 90.0 | 42.7 | 214 | 121 | 67 | 54 | 100 | 14.7% |

| Spain | 2.4% | -1.5% | 3.7% | 82.6 | 31.9 | 220 | 117 | 67 | 50 | 99 | 12.4% |

| Memo: UK | 3.8% | 0.0% | 13.1% | 86.7 | 47.1 | 219 | 121 | 56 | 65 | 99 | 12.7% |

| Since Oct 1988 | 251 | -Count | Services: | 154 | -Count | ||||||

| Sentiment is an index, sector readings are net balance diffusion measures | |||||||||||

by Tom Moeller October 29, 2009

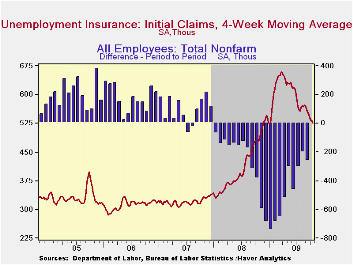

The trend

toward improvement in the job market continued this month. The Labor

Department indicated that initial claims for unemployment insurance

held roughly steady w/w at 530,000. The figures are down moderately

from an average of 549,000 claims during September and are down sharply

from the peak reached in March of 674,000 claims. The four-week moving

average of claims fell to 526,250 while the latest weekly figure was

slightly higher than Consensus expectations for 521,000 claims.

The trend

toward improvement in the job market continued this month. The Labor

Department indicated that initial claims for unemployment insurance

held roughly steady w/w at 530,000. The figures are down moderately

from an average of 549,000 claims during September and are down sharply

from the peak reached in March of 674,000 claims. The four-week moving

average of claims fell to 526,250 while the latest weekly figure was

slightly higher than Consensus expectations for 521,000 claims.

The largest increases in initial claims during the week ending October 17 were in California (+5,774, +12.6% y/y), Puerto Rico (+685, +52.9% y/y), Minnesota (+614, +38.8% y/y), Nevada (+366, 8.7% y/y ), and Nebraska (+239, -1.6% y/y), while the largest decreases were in Wisconsin (-5,681, +29.5%), New York (-4,711, +15.5% y/y), Pennsylvania (-4,033, +28.2% y/y), Illinois (-3,870, +44.9% y/y), and Oregon (-2,706, -16.6% y/y).

Continuing claims for unemployment insurance

during the latest week fell 148,000 to their lowest level since

late-March.  The decline reflects the improved job market but may also

be a function of the exhaustion of benefits. Continuing claims provide

an indication of workers' ability to find employment. The four-week

average of continuing claims fell modestly to 5,960,750 and have fallen

12.0% from their peak. This series dates back to

1966.

The decline reflects the improved job market but may also

be a function of the exhaustion of benefits. Continuing claims provide

an indication of workers' ability to find employment. The four-week

average of continuing claims fell modestly to 5,960,750 and have fallen

12.0% from their peak. This series dates back to

1966.

Extended benefits for unemployment insurance fell slightly for the first decline in seven weeks. The prior week's level was revised up. Through early-October extended benefits averaged 551,381.

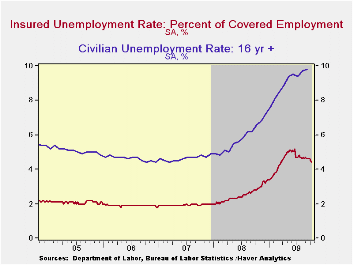

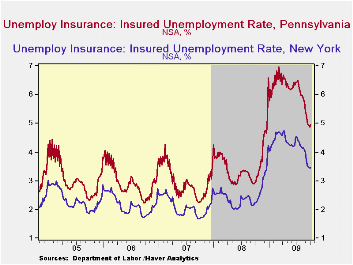

The insured rate of unemployment slipped again to 4.4%, from an unrevised 4.5%, and matched its lowest since late-March. The rate reached a high of 5.2% during late-June. During the last ten years, there has been a 93% correlation between the level of the insured unemployment rate and the overall rate of unemployment published by the Bureau of Labor Statistics.

The lowest

insured unemployment

rates during the week ending October 9 were in North Dakota (1.1%),

South Dakota (1.1), Virginia (2.0), Wyoming (2.4), Maine (2.4), Texas

(2.6), Colorado (2.9), Minnesota (3.0), Maryland (3.1), Mississippi

(3.5), New York (3.5), Florida (3.7), and Georgia (3.8). The highest

insured unemployment rates were in Puerto Rico (6.3), Oregon (5.3),

Nevada (5.3), Pennsylvania (5.0), California (4.6), Michigan (4.6),

Wisconsin (4.8), North Carolina (4.5), South Carolina (4.5), and

Washington (4.3).

The lowest

insured unemployment

rates during the week ending October 9 were in North Dakota (1.1%),

South Dakota (1.1), Virginia (2.0), Wyoming (2.4), Maine (2.4), Texas

(2.6), Colorado (2.9), Minnesota (3.0), Maryland (3.1), Mississippi

(3.5), New York (3.5), Florida (3.7), and Georgia (3.8). The highest

insured unemployment rates were in Puerto Rico (6.3), Oregon (5.3),

Nevada (5.3), Pennsylvania (5.0), California (4.6), Michigan (4.6),

Wisconsin (4.8), North Carolina (4.5), South Carolina (4.5), and

Washington (4.3).

The unemployment insurance claims data is available in Haver's WEEKLY database and the state data is in the REGIONW database.

Birth date, business cycles, and lifetime income from the U.S. Office of Management and Budget is available here.

| Unemployment Insurance (000s) | 10/23/09 | 10/16/09 | 10/09/09 | Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Initial Claims | 530 | 531 | 520 | 9.3% | 420 | 321 | 313 |

| Continuing Claims | -- | 5,797 | 5,945 | 53.6% | 3,342 | 2,552 | 2,459 |

| Insured Unemployment Rate (%) | -- | 4.4 | 4.5 | 2.8 (10/2008) | 2.5 | 1.9 | 1.9 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief