Global| Mar 02 2010

Global| Mar 02 2010Progress- No Happily Ever After Euro-Area Inflation In February Stays Under Wraps

Summary

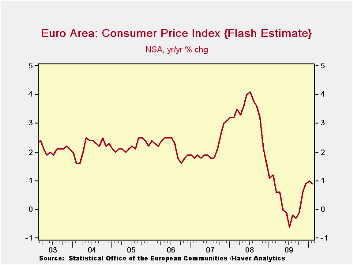

The EMU inflation chart tells a quick and dirty story of this business cycle without all the embellishments over banks lending, not-lending and financial crisis. Once upon a time, inflation was steady. Then prices overheated. Economic [...]

The EMU inflation chart tells a quick and dirty story of this business cycle without all the embellishments over banks lending, not-lending and financial crisis.

Once upon a time, inflation was steady. Then prices overheated. Economic activity subsequently plunged bringing inflation down sharply – it even negative turned Yr/Yr. All was not well. But then, weakness subsided and inflation crept back up. Now prices show signs of stabilizing with inflation around the 1% mark, well below the 2%-plus level where it had resided in the pre-crisis period. So is the inflation scare over? Will they all now live happily ever after?

Inflation fighting is no fairy tale. The recent urging of the IMF staff sho9uld make that clear; it said a higher inflation target might be ‘good for’ the US and Europe. It’s a stunning piece of work from an organization that has stepped on its own tail more than once too often. Fortunately Europe has been indignant about the suggestion and the US seems simply to have ignored it.

Inflation is very much like toothpaste out of the tube. It becomes a mess that cannot be controlled and leads to waste. Only the waste caused by excess inflation is much worse than a little excess toothpaste down the drain. In this financial crisis, however, we may have learned something that is a bit dangerous: that is that very low inflation leaves an economy less room for maneuver.

Under the leadership of former Fed Chairman Alan Greenspan all we heard was how price stability and zero inflation should be our goal and how the prices indices were biased up and so on. The lesson once again is, be careful what you wish for. Europe may fare better under lower inflation because of the breadth of its social welfare system. The US has had a harder, more stressful, time. But admitting that is not to say that US inflation should be higher or that the Fed should notch up its idea of its inflation target. It is simply to face the facts.

The ECB continues to be fixated on low inflation and, of course, has its inflation ceiling mandate. The Bank of England is similarly positioned but it has admitted to an inflation overshoot in the post crisis period that it says is not serious or lasting and contends it will ignore the temporary overshoot. The policy angle on inflation no one has really gotten their arms around is the impact of commodity prices - especially oil - on headline inflation. The ECB’s headline inflation ceiling put it in difficult straights when oil prices surged and drove headline inflation higher as the economy was weakening. The Fed’s focus on core inflation left it more flexibility to act.

Inflation is one of those peculiar things that we can all agree upon yet we find reasons to divert our attention and policy from the task at hand. It’s a bit like agreeing on what is a healthy diet yet periodically finding we are overweight and having to do something about it. The EU inflation situation appears to coming into a soft landing of sorts. That, of course, is aided and abetted by what looks like a poor growth result in the recovery. The US is in the same boat. So while the inflation situation seems in hand for now there will probably be no happily ever after here. Inflation fighting always involves pain, vigilance and sacrifice.

| Trends in EMU HICP; Flash Index | |||||||

|---|---|---|---|---|---|---|---|

| % Mo/Mo | SAAR | ||||||

| Feb-10 | Jan-10 | Dec-09 | 3-Mo | 6-Mo | 12-Mo | Yr Ago | |

| EMU-13 | 0.2% | -0.1% | 0.2% | 1.2% | 1.4% | 0.9% | 1.2% |

| Core | #N/A | -0.3% | 0.1% | -0.4% | 0.4% | 0.9% | 1.8% |

| Goods | #N/A | -0.9% | -0.1% | -2.4% | 1.4% | 0.7% | 0.2% |

| Services | #N/A | -0.5% | 0.8% | 0.3% | -0.7% | 1.4% | 2.4% |

| HICP | |||||||

| Germany | -0.3% | 0.1% | 0.1% | -0.4% | 0.2% | 0.3% | 1.0% |

| France | #N/A | 0.2% | 0.3% | 2.5% | 2.5% | 1.2% | 0.8% |

| Italy | 0.2% | -0.3% | 0.3% | 0.7% | 1.5% | 1.1% | 1.5% |

| UK | #N/A | 0.9% | 0.4% | #N/A | #N/A | #N/A | 3.1% |

| Spain | #N/A | 0.0% | 0.2% | 2.7% | 2.4% | 1.1% | 0.8% |

| Core:xFE&A | |||||||

| Germany | #N/A | -0.3% | 0.2% | -0.7% | 0.2% | 0.9% | 1.2% |

| France | #N/A | -0.2% | 0.2% | 0.1% | 0.3% | 0.9% | 1.6% |

| Italy | #N/A | -0.5% | 0.3% | 0.0% | 1.9% | 1.5% | 2.1% |

| UK | #N/A | 0.4% | 0.2% | 3.0% | 2.6% | 3.1% | 1.7% |

| Spain | #N/A | -0.3% | 0.1% | -0.1% | 0.0% | 0.3% | 1.9% |

| Blue shaded area data trail by one month | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief