Global| Dec 02 2009

Global| Dec 02 2009PPI Heats Up in the Euro Area

Summary

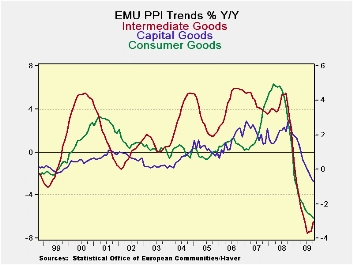

The EMU PPI has turned up in October pushing the three month headline PPI series to an annual rate gain of 4.1%. Main categories (independently seasonally adjusted) all show declines in October while the headline (ex construction) [...]

The EMU PPI has turned up in October pushing the three month headline PPI series to an annual rate gain of 4.1%. Main categories (independently seasonally adjusted) all show declines in October while the headline (ex construction) series is up.

Inflation in Germany, France, Italy and the UK rose this month. Only German core PPI inflation fell

Only Germany has persistently declining Inflation as its 3-mo, 6-mo and 12-mo inflation rates all are falling. Even so, German core inflation is showing a steady menu of higher increase across its sequential growth rates and its headline pace, despite dropping, is dropping by less and less as we shorten the horizon for inflation calculation. That means that despite its persistent declines even German headline inflation is seeing upward pressures embedded those ongoing but diminishing declines. French headline and core rates are accelerating as are the headline rates for Italy and the UK. The recent UK inflation result is eye-popping.

On balance the Euro Area has some inflation cooking. It is on simmer but Europe is not Japan and has no deflation problem. For the most part the inflation that is appearing seems to be healthy after a period of extended price declines and in an economy that needs to begin to post some growth in the aftermath of asset price drops. Italy and UK inflation rates are uncomfortably high. But headline inflation is being buffeted by energy prices and may not be indicative of true inflation pressures at all. PPI inflation is notoriously volatile. The ECB looking more closely at the HICP, yet this report will not go unnoticed.

| Euro Area and UK PPI Trends | ||||||

|---|---|---|---|---|---|---|

| M/M | Saar | |||||

| Euro Area | Oct-09 | Sep-09 | 3-Mo | 6-MO | Yr/Yr | Y/Y Yr Ago |

| TotalxConstruct | 0.3% | -0.1% | 4.1% | 0.4% | -6.6% | 6.1% |

| Capital Goods | 0.0% | 0.0% | -0.1% | -0.8% | -0.7% | 2.8% |

| Consumer Goods | -0.3% | -0.1% | -1.1% | -0.8% | -2.8% | 2.8% |

| Intermediate & Capital Goods | -0.1% | 0.5% | 3.3% | 0.5% | -6.5% | 4.1% |

| MFG | 0.3% | 0.0% | 5.2% | 2.4% | -5.2% | 3.6% |

| Germany | 0.2% | -0.2% | -5.2% | -6.1% | -7.5% | 7.8% |

| Gy ExEnergy | -0.3% | 0.1% | 0.4% | -1.0% | -3.2% | 2.4% |

| France:Tot | 1.0% | -0.2% | 6.5% | 2.7% | -6.6% | 4.9% |

| Fr ExF&Energy | 0.3% | 0.0% | 1.5% | -0.4% | -3.4% | 3.3% |

| Italy | 0.3% | 0.3% | 5.9% | 1.2% | -6.1% | 4.7% |

| UK | 1.4% | 0.4% | 19.0% | 8.6% | -2.7% | 14.6% |

| Euro Area Harmonized PPI ex construction | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief