Global| Nov 05 2019

Global| Nov 05 2019PPI Has Largest Year-on-Year Drop in Three Years

Summary

The euro area PPI was weak again in September with the headline series (excluding construction) fall after falling by 0.5% a month ago. The 12-month change marks a decline of 1.3% and is weakest showing for the PPI in three years. Is [...]

The euro area PPI was weak again in September with the headline series (excluding construction) fall after falling by 0.5% a month ago. The 12-month change marks a decline of 1.3% and is weakest showing for the PPI in three years.

The euro area PPI was weak again in September with the headline series (excluding construction) fall after falling by 0.5% a month ago. The 12-month change marks a decline of 1.3% and is weakest showing for the PPI in three years.

Is the euro area headed for another bout of deflation?

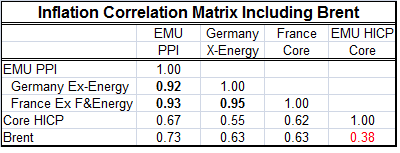

Fortunately, the answer to that question is no, at least if that answer is based on what the PPI is doing. The PPI has a poor correlation with the core HICP. In fact, there was period ending in October 2016 during which the PPI fell on year-over-year basis for 40 months in a row. Yet, the year-on-year core HICP never once turned negative. The core HICP was gaining at a 1.3% pace when this string of PPI declines began and the core HICP quickly settled down to post a year-on-year gain of only 0.9% and by the end of this run of PPI weakness the core HICP was still gaining by 0.8% year-on-year. During this period, there were only eight months in which year-on-year declines in the headline HICP were recorded (only 20% of the time that the PPI declined the HICP also was negative).

The HICP keeps its distance

The HICP keeps its distance

I tend to see all price metrics as having value, but clearly the HICP is not about to start jumping through hoops because of some weakness in the PPI. The correlation matrix shows that the PPI has a 0.73 correlation to Brent compared to a correlation of 0.38% with the core HICP, only about half the association it has with the PPI. The EMU core HICP has some correlation with the country level ex-energy indexes of Germany (0.55) and with France (0.62; core). The core HICP even has a 0.67 correlation with the EMU overall PPI itself. But clearly the headline PPI and the German ex-energy measure and the French core measures all have more in common among themselves that they do with the core HICP. The ECB targets the headline HICP and pays attention to the core, especially if oil prices are weakening and driving the headline lower.

Broad declines in the PPI across countries

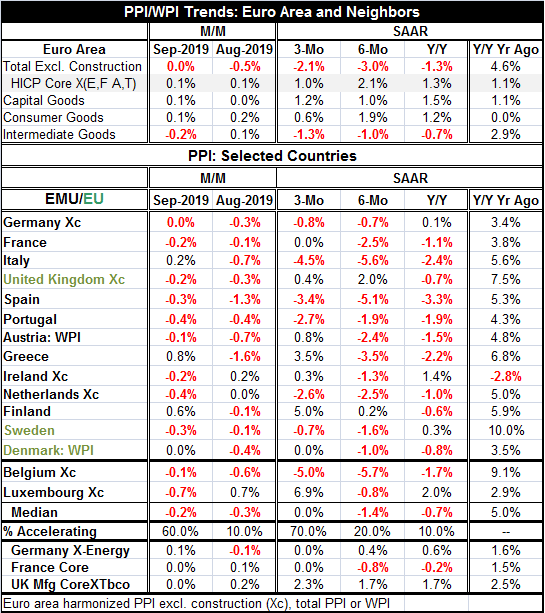

The top panel of the table shows that the PPI is declining on all horizons (three-months, six-months and 12-months), but that the tendency to decline is not getting more pronounced. During this period the core HICP is still expanding at its weakest pace, rising at a 1% rate over three months. The cause of the year-on-year declines is intermediate goods which show declines in each of the horizons and for intermediate goods where declines are becoming more pronounced. But for capital goods and for consumer goods, inflation trends show more stability although both series have weaker annualized price gains over three months than over 12 months.

A whole lot of price weakness

The data by country show the PPI declining in nine of the thirteen mixed EMU and non-EMU European countries in the table as of September. The PPI dropped in 11 of 13 in August. However, the sequential patterns show nine countries with prices dropping over six months, eight with prices dropping over 12 months, and only six with prices dropping over three months. The tendency of prices to drop is becoming less pronounced.

Diminishing inflation pressure!

This is borne out by the median country price drop that sinks from -0.7% over 12 months to -1.4% over six months but rebounds to 0% over three months. Disinflation or deflationary forces are not taking root – are not intensifying. In fact, the percentage of countries with inflation accelerating rises from 10% over 12 months to 20% over six months to 70% over three months. Granted some of these 'accelerations' are weak coming in the form of going from a larger negative number to a smaller negative number…but that counts too.

Moderate core or ex-energy trends

The data on core or ex-energy inflation are at the table bottom. They show some contrary trends. For Germany, ex-energy inflation is decelerating from 0.6% over 12 months to 0% over three months. For France, it is gyrating with the year-over-year core dropping at an accelerated 0.8% pace over six months then rebounding to 0% over three months. For the U.K., core PPI inflation is accelerating from 1.7% over 12 months and six months to a 2.3% pace over three months.

Waves of inflation

On balance, after rising for 1.5 years through the end of 2018, Brent oil prices have been declining year-on-year for nearly all of 2019. This helps to put downward pressure on PPI prices. And it has. The PPI itself has had a bit of a roller coaster ride ending a period of 40 straight months of declining in November 2016 and posting gains that accelerated to a 4.9% year-on-year pace in October 2018 before simmering down to log gains of less than 1% since June 2019 with actual year-on-year PPI declines in August and September 2019. Inflation often tends to ride these sorts of trends and waves, especially when important commodity prices are in flux.

The road ahead

For now inflation in EMU is quite stable and Christine Lagarde is taking the helm at the ECB from Mario Draghi. But that will not be an easy transition. The Germans are determined to use this transition to undo many of the programs that Draghi initiated. Today Wolfgang Schäuble 'admonished' Lagarde to implement a 'very sensible' monetary policy that respects the limits of the ECB mandate. There is no word on whether he also urged her to have the ECB hit its inflation target for a change… There is a new head at the ECB and the game there is on. It is not clear the sort of role that Lagarde will play or how much things will change at the ECB in the wake of Draghi's leaving. He was a strong president who was willing to ruffle German feathers when he thought conditions warranted it. But a new future lies ahead… The Germans look forward to preening those feathers again.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief