Global| Jan 20 2010

Global| Jan 20 2010PPI Core Behaves; Headline Is Still Unruly

Summary

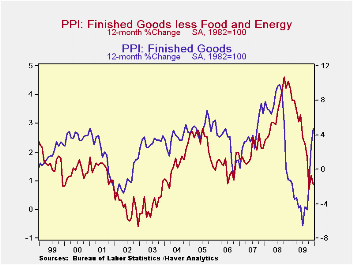

On the month the PPI was a “what-me-worry’ sort of report. A headline gain of 0.2%, the core flat, the core for consumer goods up a scant 0.1%:. No problem. Still Yr/Yr the PPI headline is up by 4.7% -and it is accelerating its rise [...]

On the month the PPI was a “what-me-worry’ sort of report. A headline gain of 0.2%, the core flat, the core for consumer goods up a scant 0.1%:. No problem. Still Yr/Yr the PPI headline is up by 4.7% -and it is accelerating its rise over shorter periods. But the core is complacent rising by 0.9% over 12-months and the consumer core is up by 1.6%. Moreover, the consumer core and overall Core PPI are both still decelerating.

The PPI is not the Fed’s preferred inflation gauge. Still it is good to see that core inflation is not percolating. If we look at the correlation between the core PPI for consumer goods and the core CPI for goods we find an R-squared relationship of 0.15, very low. The PPI is less important that the CPI and it does not track the CPI either.

The Fed emphasizes core inflation at the CPI level and for good reason. While other central banks look at the headline rate and the while that focus made the Fed (and economists) the butt of jokes as oil prices soared in 2008, history confirms the good judgment in emphasizing core inflation. Food and energy prices are volatile. When you include them in the headline you get exaggerated results when food and energy prices move. If they advance inflation is measured as too high; if they recede inflation is measured as too low. The core is the best shot we have at getting to true ongoing inflation. In 2008 when headline inflation flared the core was relatively quiescent encouraging the Fed to not over do it with worry. In fact central banks that targeted headline inflation were stuck in 2008 and 2009 since they had to cut rates with inflation still way over their targets and then make excuses. Core targeting would have made more sense.

In any event the PPI is not a source of worry. The year over year rate is still accelerating as the core rate is still decelerating. Energy and food prices each have accelerated but recently oil is looking a bit more like its movements may be capped. If so the core reading once again will hold sway on the outlook for inflation. It was inevitable that headline inflation would rise as oil prices rebounded in a global recovery. But oil has mostly come back up to where it belongs and from now on it is less clear that oil is going to be fueling a further rise in the headline.

For now we think the Fed is perfectly satisfied with inflation’s performance and prospects. Inflation expectations are for the most part still well contained. Today’s PPI report was as expected an economic non-event.

| Key Trends In Producer Prices | |||||

|---|---|---|---|---|---|

| Dec-09 | PPI Trends By Type Of Good | ||||

| PPI | 1Mo:M/M | 3-Mo:ar | 6-Mo:ar | 1-Yr | Yr-Ago |

| Total PPI | 0.2% | 9.5% | 5.0% | 4.7% | -1.2% |

| Finished Consumer Gds | 0.3% | 13.5% | 7.1% | 6.5% | -2.9% |

| Consumer Foods | 1.4% | 15.0% | 4.5% | 1.1% | 3.4% |

| Finished C Gds Excl Foods | -0.2% | 12.9% | 7.9% | 8.3% | -5.4% |

| Nondurables less Food | -0.1% | 19.6% | 12.0% | 11.5% | -8.7% |

| ConsNonDurxF&E | 0.2% | 3.4% | 2.5% | 2.5% | 5.5% |

| Durable Goods | -0.1% | -3.0% | -2.3% | 0.3% | 3.5% |

| Finished Core Cons Gds | 0.1% | 0.4% | 0.3% | 1.6% | 4.6% |

| Capital Goods | -0.1% | -1.5% | -0.8% | 0.0% | 4.3% |

| MFG Industries | -0.1% | -1.0% | -0.3% | -0.3% | 4.0% |

| NonMFG Industries | 0.0% | -1.5% | -0.8% | 0.1% | 4.4% |

| Core PPI | 0.0% | -0.5% | -0.1% | 0.9% | 4.5% |

| Memo: Finished Energy | -0.4% | 36.6% | 21.5% | 21.2% | -21.2% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief