Global| Jun 03 2021

Global| Jun 03 2021PMI Gap Between Rich and Poor Widens

Summary

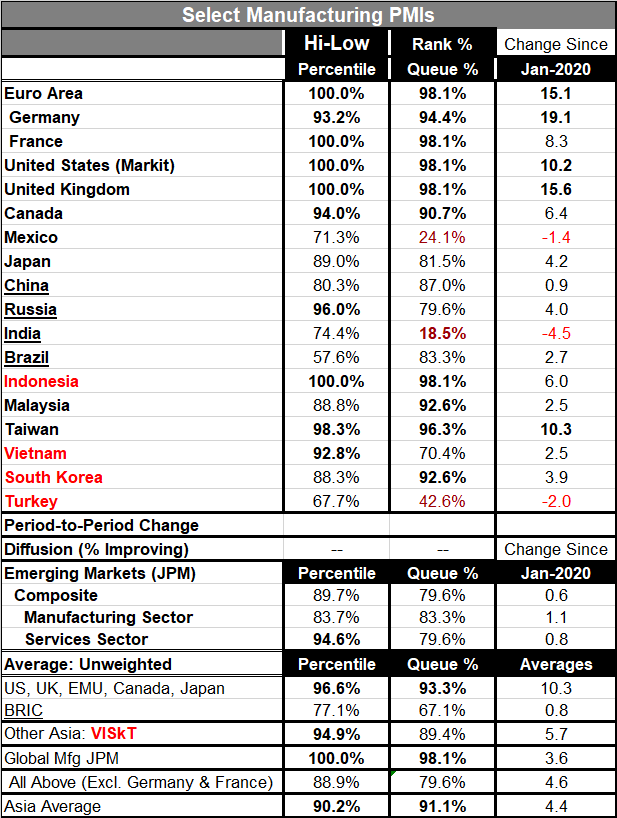

The weighted global manufacturing PMI from JPMorgan (see Global Mfg, at the table bottom) shows a tick up to 56.0 in May from 55.9 in June. The unweighted raw count of countries in the table with manufacturing sectors improving month- [...]

The weighted global manufacturing PMI from JPMorgan (see Global Mfg, at the table bottom) shows a tick up to 56.0 in May from 55.9 in June. The unweighted raw count of countries in the table with manufacturing sectors improving month-to-month shows eight improving with ten slipping. As the chart (left) reminds us, the larger more prosperous economies continue to do better and they are the countries helping to tip the balance to improvement in May.

The weighted global manufacturing PMI from JPMorgan (see Global Mfg, at the table bottom) shows a tick up to 56.0 in May from 55.9 in June. The unweighted raw count of countries in the table with manufacturing sectors improving month-to-month shows eight improving with ten slipping. As the chart (left) reminds us, the larger more prosperous economies continue to do better and they are the countries helping to tip the balance to improvement in May.

A number of subgroups (all unweighted, except the JPM indexes) at the bottom of the table show how various groups fare. Monthly data (not shown) reveal weaker conditions in emerging economies for manufacturing services and the composite in May. The BRIC group takes a step back as well. All of Asia and other Asia each are weaker month-to-month. The grouping of the U.S., U.K., EMU, Canada and Japan improves on the month.

Still, there are ten of the eighteen entries in the table with high-low standings on the May PMI readings in the top 90th percentile of their respective ranges or higher. Not all of these are the mostly highly developed economies. Vietnam, Taiwan, Indonesia and Russia make this cut. In queue percentile standing terms there is a slightly different list of ten; on this list Malaysia and South Korea replace Russia and Vietnam. There are no high-low percentile readings below their midpoint, but queue standings show that Turkey, India and Mexico each are below the midpoint of their queue of ranked observations.

The BRIC countries are lagging badly in these presentations largely because of severe virus problems in Brazil and India.

The table's far righthand column also shows how far countries have been able to rebound compared to the January 2020 levels of activity just before Covid struck. Five entries in the table log double-digit gains: Germany, the U.K., the euro area, Taiwan and the U.S. Three countries are weaker: India, Turkey and Mexico. The recovery response has been uneven.

The Service Sector

The Service Sector

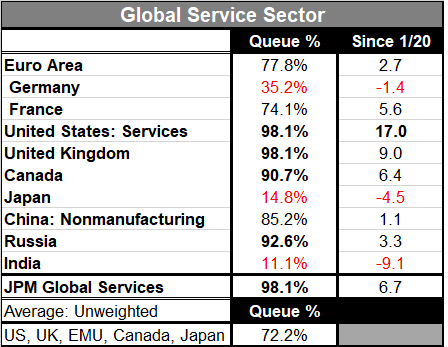

Fewer countries and areas report out separate service sector results than report manufacturing. Some like Singapore and Hong Kong simply report a composite gauge with no service/manufacturing breakout. What the services chart shows is that only the U.S. has a double-digit gain in its raw PMI index since January 2020. The U.K. comes close with a gain of 9.0. However, three countries have weaker service sectors and it's a curious list: India, Japan and Germany. India of occur has an ongoing severe Convid-19 outbreak. Japan has been cautious in controlling its infection rate with an eye to preserving the Olympics. Germany's service sector has lagged even as its manufacturing sector has prospered.

Queue standings show that of these ten entities four have readings in the top ten percentile of their queue standings. These are Canada, Russia, the U.K. and the U.S. Readings are below their respective historic medians in India, Japan and Germany, the same three countries that have weakened since January 2020.

Still, on this timeline the weighted JPMorgan service sector index has a 98th percentile standing. It has jumped to a reading of 59.4 in May boosted by a U.S. service sector reading of 70.4 and by readings in the lower 60s by the U.K. and Ireland.

Clearly the virus continued to divide and affect performance across countries. Manufacturing is more uniformly prospering or at least improving internationally. Few countries' manufacturing sectors have been left behind. But with services, we see some very large and efficient economies also struggling with their service sector performance because of virus issues. Developing economies struggle because their populations have not been widely vaccinated (or vaccinated at all!) and services often require face-to-face relationships, the kind that quickly spread the virus. Clearly there is still a lot of room for improvement in the global economy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief