Global| Nov 03 2015

Global| Nov 03 2015Oil and Select Middle Eastern Country PMI Ills

Summary

Oil prices crashed late in 2014 and have created a sort of chaos in world markets ever since. The crash in the oil price was a combination of things involving slower growth in China and in the rest of the world as well as the impact [...]

Oil prices crashed late in 2014 and have created a sort of chaos in world markets ever since. The crash in the oil price was a combination of things involving slower growth in China and in the rest of the world as well as the impact of technology and its ability to raise old oil fields from the dead. There are geopolitical features as well. Add fracking and the development of more natural gas fields and a true energy glut developed hammering prices - and that just a few short years removed from the notion that oil would trade at $150/bl ($123/bl average in April of 2011). The oil price crash was precipitated by the Saudis, the largest oil producer in the world, and their sudden reluctance to be the world's swing producer to hold oil prices aloft.

Oil prices crashed late in 2014 and have created a sort of chaos in world markets ever since. The crash in the oil price was a combination of things involving slower growth in China and in the rest of the world as well as the impact of technology and its ability to raise old oil fields from the dead. There are geopolitical features as well. Add fracking and the development of more natural gas fields and a true energy glut developed hammering prices - and that just a few short years removed from the notion that oil would trade at $150/bl ($123/bl average in April of 2011). The oil price crash was precipitated by the Saudis, the largest oil producer in the world, and their sudden reluctance to be the world's swing producer to hold oil prices aloft.

The Saudis now seek a hegemony that will not require its flex of market muscle to cost it market share. However there is nothing in the Saudi's actions that gives a hint as to how that might be accomplished. When OPEC ruled, oil production was concentrated, but OPEC no longer controls global prices and many of the new producers are small. Market structure does not lend itself to OPEC like collusion. The plunge in oil prices is meant to put pressure on other producers but it is like the pulling the pin of a hand grenade in a closed room. The Saudis are damaged too.

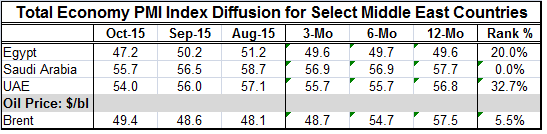

The table produces PMI data for the whole economy of Egypt, Saudi Arabia and the UAE. These whole economy PMIs have been dropping and fast. The speed of decline has picked up in the last several months. The level of the respective PMI indices is low (in a ranking stemming back to April 2011). In this three-country group, the UAE is the relative strongest with a standing in its 32nd percentile. Egypt is next, standing in its 20th percentile. Saudi Arabia is the relative weakest, standing in its lowest level for this period. Of course, in absolute terms (the diffusion level), Saudi Arabia is the strongest, but the percentile gauges make a different comparison. They show how weak the Saudi economy is relative to its own history, not relative to other countries. On that score, it is the worst off it has been since April 2011.

The oil weapon has brought pressure on the smaller oil explorers and producers in the U.S. In fact, there are bank loans that are going bad; U.S. bank regulators have warned banks about how they handle problems in the sector. The rig count in the U.S. fell to 578 as 16 rigs went out of service in the week ended October 30. This is the lowest rig count in the U.S. since June 2010 when Brent crude stood above $74/bl. Yes, the low oil price policy is working. But that does not mean this strategy will be successful.

We also see trouble and pressure in the Saudi economy.

Saudi Arabia's economy is under pressure. The nation may be forced to take on sovereign bank debt or to scale back on some of its investment projects. The Saudi credit rating was recently cut by Standard & Poor's to A+ from AA- a drop of one notch on the rating scale. The A+ rating is six levels up from junk. Other countries rated A+ are Israel and Ireland. Energy sales make up about 80% of the Saudi budget revenue. Playing with oil prices in Saudi Arabia is playing with fire.

The oil situation is complicate as geopolitical forces enter in the wake of a U.S.-Iran nuclear deal. That will end Iran oil sanctions and permit Iranian oil to flow freely to world markets. We see pressures being generated all around. There will be new oil brought to market by Iran. Technology will continue to generate oil output. But the counter force of weak prices will limit and remove some production. And global demand seems destined to be weak for the foreseeable future.

While central banks are doing their best to pump up growth, monetary stimulus simply is not working. Saudi Arabia's strategy has been able to reduce the rig count. It is not clear how much new production will be made uneconomic by oil hovering just below $50/bl in terms of the Brent price. If Saudi Arabia gets more aggressive, an act that would hurt it too, it is not clear that it has anything lasting to gain. Low prices cannot erase the technology. Technology is there and would become economic again if oil prices were to rise after an act to shove them lower.

Oil market dynamics are complicated. My guess - and that is all one can have at this point - is that oil prices are going to continue to float in this range. If the global economy slips further lower oil prices could evolve and that would be a disaster for all oil producers. I don't see prices lower than this as a purposeful or productive Saudi strategy. But that does not mean it can't happen.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief