Global| Dec 08 2014

Global| Dec 08 2014OECD LEIs Tell Unsettling Story

Summary

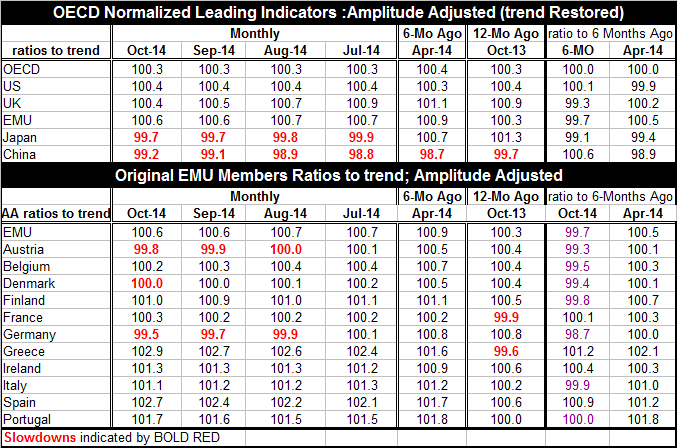

The OECD LEI in October signals weakness for most of the OECD reporting countries. The LEI readings are below 100 in October for Japan, China, Austria, Denmark and Germany. These weak readings point to lees than trend growth. In [...]

The OECD LEI in October signals weakness for most of the OECD reporting countries. The LEI readings are below 100 in October for Japan, China, Austria, Denmark and Germany. These weak readings point to lees than trend growth.

The OECD LEI in October signals weakness for most of the OECD reporting countries. The LEI readings are below 100 in October for Japan, China, Austria, Denmark and Germany. These weak readings point to lees than trend growth.

In addition The UK, EMU, and Japan show October LEI readings that are below their 6-month ago levels, signaling a slowdown.

Within EMU slowdowns are signaled for Austria, Belgium, Denmark, Finland, Germany and Italy. Over the previous six months (as of April) all of the EMU nations had been signaling an expansion as the LEI's were all above their six month ago levels. Things have changed.

Last week the Bundesbank downgraded its outlook for the Germany Economy on the same day as German industrial orders accelerated. Today German industrial output underperformed expectations. Over the weekend Angela Merkel was critical of the austerity steps taken by France and Italy. On Monday Germany was trying to undo that damage lauding France and Italy for their efforts. Still, Italy was downgraded by S&P late last week to a rating of just above junk. No matter how puny Italy's and France's efforts seem, their economies are not in good shape they are finding it hard to take stronger steps toward meeting EMU financial obligations. And they are not alone. Belgium is suffering strikes as its people protest austerity there, in a country that is solidly in the core of the euro-Zone.

Germany is having its outlook downgraded but it is still the best performing economy in Europe. Yet Germans remain uneasy with the state of fiscal policy throughout the Eurozone and have taken this opportunity to become more fiscally fit themselves. Meanwhile, the ECB is not getting a go-ahead to implement a program of greater monetary ease. Everyone is watching and waiting.

The elaboration over the weekend by Russian President Vladimir Putin of the State of Russia and his plan to deal with it suggests that Russia is suffering under a more draconian set back than Europe Economic sanctions are biting hard in Russia. Putin has announced the extent of austerity and it would appear to involve a substantial run off of Russia's foreign exchange reserves and further clamp down on wages and living standards there.

Additional news today showed a higher Chinese trade surplus as exports slowed and imports contracted. China seems to be under even stronger contractionary pressures that it seemed to be suffering from a short time ago when its leader proclaimed that all was in hand. Suddenly, trouble seems underfoot.

In today's markets Europe is still reeling from a down grade of Italy to a level just above junk status. But there are hopes that the strong U.S. job report from Friday for November is a signal of accelerating U.S. growth. Yet U.S, income growth has still not shown itself to be strong. The rise in the U.S. economy may not have strength enough to offset the weakness we are seeing throughout the global economy. The Friday U.S. jobs report showed that average hourly earnings gains did not trickle down to accelerate for production workers. Consumer attitudes in the U.S. are improving but slowly. It is far from clear the OECD leading indicators for the U.S. support that degree of optimism. The U.S leading index ratio to six months ago is only at 100.1 while the ratio from six months ago was below 100. Growth in the US has been without a substantial upward kick to momentum for some time.

Of course, there is hope that lower energy prices will revitalize global demand. Europe is an energy importer so lower prices will have substantial effect there. However, since taxes are larger as share of prices consumers pay, the impact on consumers will not be a great as in the US. But the US is also a producer and will experiences some negative effects on the production side. Those negative effects are not yet apparent among U.S. producers. Nor is there evidence of weaker U.S. exports in the wake of a rising dollar and limping growth overseas. For now the trend for Europe is negative and the hopes for the U.S are high as data from Asia for China and Japan continue to show unexpected weakness. It's not the best of circumstances as we head for the holiday season.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief