Global| Oct 10 2016

Global| Oct 10 2016OECD LEIs Stuck in Very Low Gear: A Eulogy for Growth

Summary

The OECD LEIs remain mired in the muck of readings below the breakeven value of 100, but close enough for the OECD to continue to look for relatively stable growth. The overarching OECD index, the U.S. index, the U.K. index, the Japan [...]

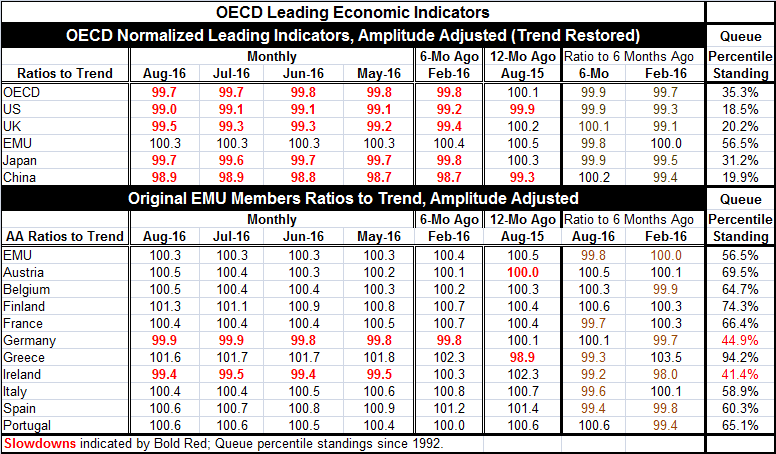

The OECD LEIs remain mired in the muck of readings below the breakeven value of 100, but close enough for the OECD to continue to look for relatively stable growth. The overarching OECD index, the U.S. index, the U.K. index, the Japan Index and the China index, each sits below their respective 100 index level as of August. The OECD and Japan sit at 99.7, the U.K. is at 99.5, the U.S. is at 99.0 and China sits at its 98.9 index level. The EMU has a 100.3 standing, above its 100 mark, but not by much. On the month, only the U.S. index deteriorated while the Fed made plans to hike rates before yearend. The U.K. and Japan improved by small amounts; the rest of the indices were flat on the month. None of this is particularly worrisome or reassuring. It is the same sluggish environment that has evolved the global economy since the financial crisis came and went. However, what is interesting is that on both sides of the policy aisle policymakers are getting restless. Some think policy is dangerous because it has been too expansive for too long. Others think that the global economy is more at risk because growth remains stuck in such a low track with no sign of acceleration. Both sides are looking to do something to remedy their respective concerns. In the U.S., despite uneven growth and slowing jobs gains, the Fed seems to be stepping closer to a rate hike. At the recent IMF meeting, members worried more vocally about protectionism and entertained talk at least about the possible use or role of fiscal stimulus. And the pending remedies from these factions are, of course, 180 degrees different.

The OECD LEIs remain mired in the muck of readings below the breakeven value of 100, but close enough for the OECD to continue to look for relatively stable growth. The overarching OECD index, the U.S. index, the U.K. index, the Japan Index and the China index, each sits below their respective 100 index level as of August. The OECD and Japan sit at 99.7, the U.K. is at 99.5, the U.S. is at 99.0 and China sits at its 98.9 index level. The EMU has a 100.3 standing, above its 100 mark, but not by much. On the month, only the U.S. index deteriorated while the Fed made plans to hike rates before yearend. The U.K. and Japan improved by small amounts; the rest of the indices were flat on the month. None of this is particularly worrisome or reassuring. It is the same sluggish environment that has evolved the global economy since the financial crisis came and went. However, what is interesting is that on both sides of the policy aisle policymakers are getting restless. Some think policy is dangerous because it has been too expansive for too long. Others think that the global economy is more at risk because growth remains stuck in such a low track with no sign of acceleration. Both sides are looking to do something to remedy their respective concerns. In the U.S., despite uneven growth and slowing jobs gains, the Fed seems to be stepping closer to a rate hike. At the recent IMF meeting, members worried more vocally about protectionism and entertained talk at least about the possible use or role of fiscal stimulus. And the pending remedies from these factions are, of course, 180 degrees different.

All indices except for the U.K. also are below their respective values of six months ago. The six-month values are below their respective values of six-months before that in all regions. There is a lengthy period of underperformance depicted here.

In addition, we can evaluate the various countries and regions by the relative standing of these OECD indicators in their historic queue or 'stack' of values since 1992. On that basis, the U.S., China and the U.K. all are the weakest with readings clustered at or below their respective lower 20th percentile when ranked in a queue of historic data. Japan is in its lower 31st percentile; the whole of the OECD stands in its 35th percentile, while the EMU manages an above-median 56th percentile standing.

For the EMU, the readings stand above the 100 mark for all of the early EMU members except Germany and Ireland. Readings are below their respective six-month ago readings for the whole of EMU, France, Greece, Ireland, Italy and Spain. That underperforming group includes three of the four largest EMU economies.

Europe's growth remains weak although the bit of 'good news' today was that German exports in August jumped by 5.3% month-to-month, an outsized gain that was last exceeded in May 2010. But in that May report the rise followed a 3.2% drop in April and came during a period of real turbulence. This year the August gain came after a drop of 2.6% in July and a series of nine months in which exports fell in five of them. Nominal German exports are up by more month-to-month than they are year-over-year (4.9%). Meanwhile, real German export-order growth is quite firm and steadying at around a relatively solid 6% pace. Still, the August monthly export gain is coming off such a weak month that the rise is much less impressive than it seems. To provide some perspective, two-month export growth is only the highest since March of this year.

At the recent IMF meetings, world financial ministers met to discuss issues. They displayed concern about growing protectionism. It is unclear if any nations are prepared to take any concrete steps to affect global growth as a result of this meeting or the expression of these concerns. China came under attack for its overproduction and on allegations of dumping (selling below cost). The global economy is clearly struggling. It is stuck in their low gear as the LEIs make clear and as the position of this month's indices in their historic ranking underscores. In the end, here are questions whether anyone is prepared to do anything about it besides provide a eulogy for growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.