Global| May 12 2015

Global| May 12 2015OECD LEIs Find Encroaching Weakness in March

Summary

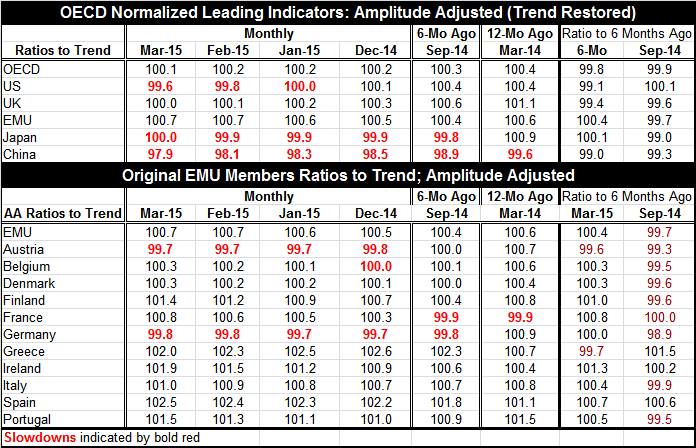

The OECD leading indicators for March show slippage in the OECD, the U.S., the U.K., and China. The EMU gauge is unchanged in March while Japan's gauge has moved higher. The U.S. has been slipping since June 2014. Its reading of 99.6 [...]

The OECD leading indicators for March show slippage in the OECD, the U.S., the U.K., and China. The EMU gauge is unchanged in March while Japan's gauge has moved higher.

The OECD leading indicators for March show slippage in the OECD, the U.S., the U.K., and China. The EMU gauge is unchanged in March while Japan's gauge has moved higher.

The U.S. has been slipping since June 2014. Its reading of 99.6 in March is its weakest since November 2011. The EMU gauge has been rising but very slowly since September 2014. China has been sliding lower gently since July 2013.

The OECD indices are net lower over six months. That is the OECD's preferred horizon to view its signals. For all of the OECD, the U.S., the U.K. and China, conditions are slipping over six months. Only Japan and the EMU show steady or improving trends over that span.

Within the EMU, only Austria and Germany show LEI readings below 100 for March. That reading means the gauges are below their long-term averages. The EMU as a whole stands at 100.7 in March level with its February reading.

The ratio to six months ago shows Austria and Greece as the only two EMU members in the table that are net lower on that span. Six months ago in September 2014, the EMU's own ratio was net lower over six months and ratios were lower in eight of the 11 countries in the table (all but Greece, Ireland and Spain). Compare that to having just two countries net lower as of March 2015. The euro area is clearly making progress.

Yet, month-to-month the OECD gauge for the EMU is unchanged. A host of indicators for other countries are showing weakness including for the OECD region taken as a whole.

U.S. and China weakening trends run relatively deep. It's not like this weakness is an artifact of one month's weak data or so. The OECD has been warning the U.S. and implicitly the Fed that the U.S. economy is not very strong despite the Fed's despite to hike rates. Right now interest rate markets are taking a toll on equity markets. There are broader consequences if rates rise. As we saw in the April jobs report, U.S. job growth has slowed down and, had construction employment not jumped in April, overall U.S. job growth would have been disturbingly weak for the second consecutive month. The OECD has a point.

In the EMU, fixes are still being applied. The ECB is in the middle of its QE program. Europe is most at risk to what it does about Greece. Greece seems to be in a lose-lose situation as it is saddled with more debt than it can carry. Most importantly, Greece has been sticking to austerity but wants some modification. Europe now seems to be punishing Greece for its attempt to wiggle out of some of its promise of austerity after an election that said the people did not like it. Greece and the EMU will have to come to some political solution over this because an economic solution does not seem to exist in this environment.

It would be much nicer if we could report that the Greece-EMU talks were occurring in an environment in which the Greek and EMU economies and the global economy were all doing better. But that is not the case. As you can see for the OECD LEIs and even for Germany, there is not even very good momentum. Time is running out. We expect some kind of accommodation to be made because the consequences for each side are too grim to risk given the circumstances of their current minor disagreements.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief