Global| May 10 2010

Global| May 10 2010OECD LEIs Continue To Advance

Summary

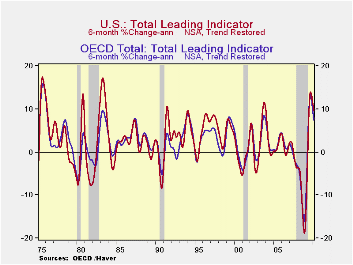

After a jackrabbit jump the OECD trend restored Leading Economic indicators are slowing their pace. Still, viewed over six months which is the OECD’s preferred way of using them, the grow rates across the OECD region remain quite [...]

After a jackrabbit jump the OECD trend restored Leading Economic indicators are slowing their pace. Still, viewed over six months which is the OECD’s preferred way of using them, the grow rates across the OECD region remain quite strong, Japan is even accelerating to the second best growth rate in the table. Still, all rates decay over three-months compared to six months.

The challenge to growth, however, is for the period ahead. Evidence is that China is slowing. The Greek crisis and its knock-on effects damaged Europe and have more permanently helped to re-shape Europe’s political power structure.

Now a new support package is in place for Greece and a one trillion dollar backstop for Europe’s laggards has been set up. The ECB is supporting this with bond purchases and the Fed has reactivated its swap lines to help. How much will these new actions compensate for the damage that came before them? How weak will China actually be? And how much if at all will the US economy and its financial markets be damaged by its one-off (?) intra-day thousand point drop in the DJIA from last week? Investing dollars, yen and euros want to know.

As of March things look good across the OECD area. The most up-to-date economic data from the US have been very upbeat. Europe’s most recent readings have been good as well, but the new investor confidence reading from Sentix turned sharply and decisively into negative territory.

Nonetheless it’s a good thing to have the economies hit by these adverse forces while they are gaining momentum. All the trends will bear watching. Upward momentum bolstered with these new pushes by policymakers yet may carry the day.

| OECD Trend-restored leading Indicators | ||||

|---|---|---|---|---|

| Growth progression-SAAR | ||||

| 3Mos | 6Mos | 12mos | Yr-Ago | |

| OECD | 5.6% | 7.3% | 10.2% | -11.1% |

| OECD7 | 6.0% | 7.8% | 10.5% | -12.5% |

| OECD.Ezone | 2.9% | 5.1% | 9.4% | -11.4% |

| OECD.Japan | 8.0% | 9.1% | 8.8% | -14.3% |

| OECD US | 8.4% | 9.7% | 11.5% | -12.8% |

| Six month readings at 6-Mo Intervals: | ||||

| Recent six | 6Mo Ago | 12Mo Ago | 18MO Ago | |

| OECD | 7.3% | 13.1% | -10.8% | -11.4% |

| OECD7 | 7.8% | 13.3% | -13.1% | -11.9% |

| OECD.Eur | 5.1% | 13.8% | -9.0% | -13.7% |

| OECD.Japan | 9.1% | 8.6% | -18.1% | -10.3% |

| OECD US | 9.7% | 13.4% | -14.6% | -11.1% |

| Slowdowns indicated by BOLD RED | ||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief