Global| Jan 08 2010

Global| Jan 08 2010OECD LEIs Are Surging Especially Strong Is The Euro-Area

Summary

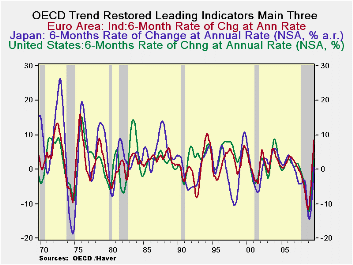

The OECD trend-adjusted leading indicators are showing strong increases compared to past business cycles. The chart shows that Europe, Japan, and the US have not been as synchronous and stronger since the expansion from the 1973-75 [...]

The OECD trend-adjusted leading indicators are showing strong increases compared to past business cycles. The chart shows that Europe, Japan, and the US have not been as synchronous and stronger since the expansion from the 1973-75 recession. The expansion from the 1981-82 recession was stronger (at least eventually) for the US but it took Japan until very late in the cycle to get stronger and Europe never did show the strength in that cycle that it is showing now, while it is still early in the cycle. Japan is not yet hitting a home run; its LEI rise (which is positive over six-months) is still small, but it also lagged in the recovery from the recession of 1981-82.

On balance the OECD data are impressive. They point to a recovery in progress. Push the pessimists aside. The main industrial economies are leading the way forward. It is important to look at the trends a to not get to caught up in the month to month numbers which always ebb and flow but whose natural ebb and flow seems more daunting when the economy is still sputtering.

What we learn in looking at the these indicators and these various economies’ monthly releases is how much the stock markets remains priced for good news but bond markets continue to mark jagged paths as they go from fearing strong growth and inflation to showing disappointment over current indicators that fall short of robustness. This sort of back and forth is very much the usual way of things early in economic recoveries. This recovery is so early in fact that the label ‘recovery’ has yet to be made official by the recession-dating arbiters.

| OECD Trend-Restored Leading Indicators | ||||

|---|---|---|---|---|

| Growth Progression-SAAR | ||||

| 3Mos | 6Mos | 12mos | Yr-Ago | |

| OECD | 11.4% | 13.7% | 6.3% | -9.7% |

| OECD7 | 12.2% | 14.4% | 5.7% | -10.4% |

| OECD.Euro-Area | 12.4% | 14.9% | 8.5% | -11.0% |

| OECD.Japan | 10.8% | 12.1% | 0.7% | -9.8% |

| OECD US | 12.2% | 14.2% | 4.9% | -10.1% |

| Six month readings at 6-Mo Intervals: | ||||

| Recent six | 6Mo Ago | 12Mo Ago | 18MO Ago | |

| OECD | 13.7% | -0.7% | -14.9% | -4.2% |

| OECD7 | 14.4% | -2.4% | -15.9% | -4.6% |

| OECD.Eur | 14.9% | 2.5% | -15.2% | -6.5% |

| OECD.Japan | 12.1% | -9.6% | -16.7% | -2.4% |

| OECD US | 14.2% | -3.7% | -15.9% | -3.9% |

| Slowdowns indicated by BOLD RED | ||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief