Global| Sep 07 2016

Global| Sep 07 2016OECD LEIs Are Flat: Subtle Slowing Mostly Indicated

Summary

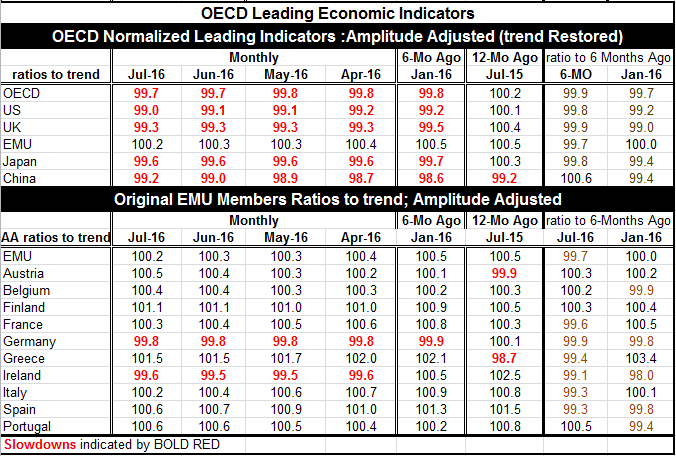

The OECD LEIs for July are mostly at index levels below 100 which indicate some slowing. In the top panel of select countries/regions only EMU retains an index value above 100 at 100.2. China is below 100 but has picked up in July [...]

The OECD LEIs for July are mostly at index levels below 100 which indicate some slowing. In the top panel of select countries/regions only EMU retains an index value above 100 at 100.2. China is below 100 but has picked up in July compared to June rising from 99.0 to 99.2. The US is slowing further, dropping in July to 99.0 from 99.1. Compared to their index readings of six months ago, all of the countries/regions in the top panel of the table are slowing except China. All but EMU were slipping over the prior 6-mo period as well. There is for the most part a long slow slippage in train. I would describe this as akin to termites in the wood work.

The OECD LEIs for July are mostly at index levels below 100 which indicate some slowing. In the top panel of select countries/regions only EMU retains an index value above 100 at 100.2. China is below 100 but has picked up in July compared to June rising from 99.0 to 99.2. The US is slowing further, dropping in July to 99.0 from 99.1. Compared to their index readings of six months ago, all of the countries/regions in the top panel of the table are slowing except China. All but EMU were slipping over the prior 6-mo period as well. There is for the most part a long slow slippage in train. I would describe this as akin to termites in the wood work.

The Lourdes Strategy

There is nothing good or in the sense of progress going on. There is subtle and ongoing-actually relentless- erosion. There are few exceptions. But the damage is so slow policymakers feel that they ignore it. And this is at least partly because they have done so much they are afraid of the gravity of the next steps they may have to take and fear taking them preferring to watch to see if there is some spontaneous end to the ongoing erosion in conditions instead. We could call this the Lourdes strategy as it seems to be geared to waiting for a miracle.

Poor Trends

Looking more closely at EMU and the trends of its original member countries, we see a bit of stability. Only Germany- the largest EMU economy- and Ireland have readings persistently below 100. However, compared to 6-mo ago the overall EMU reading is weaker; also weaker are France, Germany, Greece, Ireland, Italy and Spain. All four of the largest EMU economics are on this list. Compared to six-months before that there was slowing in Belgium, Germany, Ireland, Spain and Portugal. Germany, Ireland and Spain have long legacies of ongoing slowing behavior. Picking up over six-months are the smaller economies: Austria, Belgium, Finland and Portugal.

Reassurance...no

There is not much here to reassure. Trends are not positive within EMU and they are not improving for the most part. The OECD data which are designed to look ahead more than just to chronicle the past are nonetheless echoing the recent message from the PMI data which have continued to soften and to emit readings that are weak in absolute terms.

Queue standings of LEI values are weak- The US is very weak!

We can also rank the standing or levels of the current OECD LEIs in a queue of data back to early 1992 for all these countries and regions. Such a ranking of current readings expressed in percentile terms finds the U.S. and the U.K. are the relative weakest in their 13th percentile and 12th percentile, respectively. China stands in its 18th percentile; Japan in its 25th percentile. The EMU LEI reading stands above its median for the period at its 52nd percentile. Despite assertions that the US is doing relatively better and that the Fed might even be close to hiking rates, compared to this relatively long timeseries of LEI observations it is EMU that is the more solid ground relative to the recent past when we rank the regions on forward looking LEI indices.

Inside EMU

Looking inside EMU at is various members, Greece is doing the relative best with a ranking of its OECD LEI that has been higher only 8% of the time since 1992. Finland stands in is 68th percentile as the next relative strongest. After that France, Austria, Portugal and Belgium are the next strongest with rankings in their low-to-mid 60th percentile region. Spain ranks in its 58th percentile and Italy at its 52nd percentile. Standing below their historic medians are Ireland, at its 45th percentile, and Germany, at only its 35th percentile.

Weakness is the watch-word

These rankings only place the current LEI readings in a queue of historic values. The OECD uses the actual index magnitudes as markers rather than just the relative standings, but both have meaning. And on all scores too many key countries are too weak: the U.S., the U.K. Germany, Japan and China. Any way you slice it weakness is still the watch-word of the global economy. In some ways the weakness might be subtle but it is still present.

And the ECB...sits on its hands

At today's ECB meeting Central Bank President Mario Draghi was still in search of the right policy options and not yet prepared to pull the trigger on a new round of stimulus. Instead, the ECB has "tasked the relevant committee to evaluate the options that ensure a smooth implementation of the purchase program." If ever there was an evasive bureaucratic description of what policy was not about to do, that was it. Draghi released some modest downgrades of EMU growth forecasts and gave lip-service to downside risks being present saying also that the changes in the outlook and the risks were not yet substantial enough to warrant action. This, of course, is by now familiar ground. Warning with no action - or action that is less than expected and eventually not effective- is business as usual. There is no sense despite the ongoing stubborn nature of the economic weakness that there is any imperative to act. After all, there is always plenty of time to be too-late and to do too-little.

Kicking "the can" instead of kicking the butt of weakness

The ECB has just kicked the can down the road and this is largely what markets had expected it to do at this meeting. But that does not mean that markets will like it. What else could the ECB do? It has been suggested that it could engage in the purchase of new types of assets, like bank bonds, non-performing loans or in the extreme case, stocks. And none of these are actions that it should take lightly. Some would argue they are actions it should not take at all. And that, in the end, is why the ECB chooses to do nothing. Draghi again urged that structural reforms be taken up by regional governments to raise productivity, improve the business environment, and boost the infrastructure. He did not invoke the name of the tooth fairy or of Santa Claus. But why not add them to the wish list of things that will never happen? And he urged... "Fiscal policies should also support the economic recovery." But that ship seems to be hopelessly under repair in dry dock. That ship may never sail again, at least not under Draghi's tenure.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief