Global| Mar 06 2009

Global| Mar 06 2009OECD LEI's Show Severe And Worsening Downturn

Summary

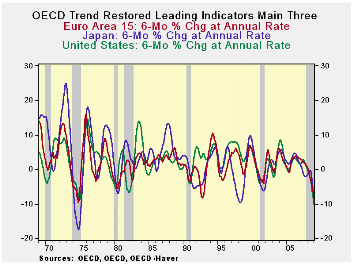

The plunge in the US, Japan and European LEIs is quite characteristic of recession as the chart on top demonstrates. However, the severity of the declines is unusual. In the past 40-Years only the 1973-75 downturn produced larger [...]

The plunge in the US, Japan and European LEIs is quite

characteristic of recession as the chart on top demonstrates. However,

the severity of the declines is unusual. In the past 40-Years only the

1973-75 downturn produced larger declines for the US. Japan’s decline

is already steeper than its 1973-75 recession drop; Europe’s is about

the same and the US drop is not (yet?) as severe.

However the OECD framework shows that the declines across most

regions are accelerating. Across 6-mo intervals all the main groups are

declining increasingly rapidly over each of the last two six month

segments (bottom panel of table). Separate progressive growth rates

(top panel of table) show that that over three months the growth rate

in Europe has showed some recovery compared to its performance over six

months. But that ‘improvement’ is not by much.

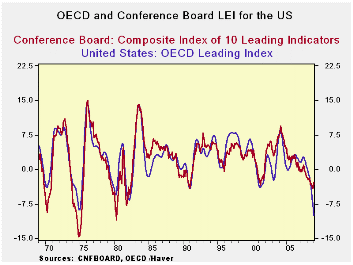

The chart below shows that the OECD and US Conference Board

indices (LEIs) have different views of the US situation. In past deep

downturns the Conference Board index fell by more. In this episode- -

at least at this point of the downturn – the OECD index is showing a

substantially sharper US decline and one that is accelerating instead

of moderating as in the US treatment from the Conference Board Index.

On balance the OECD signal for the US is much worse than from

the US own LEI that has actually stated to turn up (less down) in

January. More topical data from Europe for February suggests that

conditions there continue to weaken. The LEI signal is not infallible

and may not always give the most prescient look ahead. But it is only

one index- a single number- and only so much can be expected from it.

History is quite kind to the LEI gauge as the frame work has a very

good and consistent cyclical signal. For the moment the message is

quite clear that the OECD is not signaling that the worst is over. It

is signaling that we are still in the middle of a difficult and severe

downturn- quite severe by the standards of the past 40 years – and that

continued vigilance is recommended. It’s a very good thing that the ECB

joined the BOE in rate cuts this past week. Clearly the cut was needed.

As for the US discrepancy in the LEI signals that obviously

bears some watching.

| OECD Trend-restored leading Indicators | ||||

|---|---|---|---|---|

| Growth progression-SAAR | ||||

| 3Mos | 6Mos | 12mos | Yr-Ago | |

| OECD | -12.8% | -9.9% | -5.6% | 1.3% |

| OECD7 | -14.7% | -11.3% | -6.6% | 0.7% |

| OECD. Eur | -11.3% | -9.5% | -6.0% | 1.4% |

| OECD. Japan | -14.1% | -9.9% | -4.0% | -1.9% |

| OECD US | -17.4% | -12.8% | -7.6% | 1.2% |

| Six month readings at 6-Mo Intervals: | ||||

| Recent six | 6Mo Ago | 12Mo Ago | 18MO Ago | |

| OECD | -9.9% | -1.1% | -0.3% | 3.0% |

| OECD7 | -11.3% | -1.6% | -1.1% | 2.5% |

| OECD. Eur | -9.5% | -2.2% | 0.5% | 2.3% |

| OECD. Japan | -9.9% | 2.2% | -2.6% | -1.2% |

| OECD US | -12.8% | -2.1% | -1.4% | 3.8% |

| Slowdowns indicated by BOLD RED | ||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief