Global| Aug 08 2008

Global| Aug 08 2008OECD Indicators Do Not Point to Good News

Summary

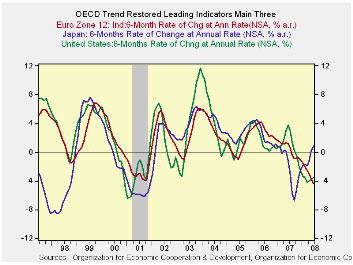

The OECD Trend-restored LEIs tell a story that is now becoming familiar in the markets. The US is still weakening. But Europe is weakening faster. Just today Italy reported a DECLINE in GDP for 2008Q2. Nout Wellink, an ECB board [...]

The OECD Trend-restored LEIs tell a story that is now becoming

familiar in the markets. The US is still weakening. But Europe is

weakening faster. Just today Italy reported a DECLINE in GDP for

2008Q2. Nout Wellink, an ECB board member, said the European growth

would… “not look so good.” Europe has been slow to admit how much its

economy is being impacted by oil and the financial crisis and the

strong euro. Denial has its costs.

I think we have finally heard the last from those poor souls

who argued that there was some sort of de-linkage going on in the

global economy. Europe would still grow, China, India ..etc. But

clearly the slowdown is hitting everyone. The Euro slowdown could

become more severe and that is part of the OECD warning this morning as

it sees a sharper slowing in the cards. OECD finds China and Brazil as

relative bright spots. The OECD said that while its leading indicators

point to slowdowns in the U.S., Japan, Germany, the U.K. and Canada,

they point to "strong" slowdowns in France and Italy. For Russia and

India, the leading indicators point to a downturn. Of course the

definition of downturn is not universal. To a fast growing economy it

could be just a big slowing in the growth rate. For most highly

developed economies it means there will be some decline in GDP.

For now the OECD message is clear and that message is not

welcome. Yet, neither is it a surprise to those who have paid

attention. Europeans have for some time looked at the bright side of

the picture and ignored the encroaching darkness. The ECB was bound and

determined to hike rates due to its horrific inflation overshoot of its

target. The ECB needed to see the strong the side of the economy to

justify a rate hike.

For now it seems to me the central banks have been put in a

very difficult position with a financial crises that crimped their

ability to act boldly. At the same time huge and ongoing increases in

oil prices struck. Exchange rates moved significantly as well. Looking

back, policy seems to have been well calibrated despite headline

inflation overshoot. The question may come to be asked if a core

inflation target might not work better in the future (since if we

assume the central banks more or less were really looking at core,

their actions are easier to understand). The ECB so badly has missed

its target it must have to wonder if wants to ever go though that

again. However, relative to a core inflation target it is has not done

so badly- nor has the Fed. We will have to see what lessons emerge from

this still evolving period.

While policy may have done a good job it nonetheless has not

been able to avoid the scars and scrapes on banks and on the real

sector. Policy has done a good job but has worked no miracles. There is

room for improvement. But first there is a policy to implement in a

still nettlesome business cycle that is building downside strength.

| OECD Trend-restored leading Indicators | ||||

|---|---|---|---|---|

| Growth progression-SAAR | ||||

| 3-Mos | 6-Mos | 12-Mos | Yr-Ago | |

| OECD | -3.5% | -3.0% | -3.1% | 2.1% |

| OECD7 | -2.3% | -3.1% | -3.8% | 1.5% |

| OECD Europe | -6.3% | -5.2% | -3.7% | 1.1% |

| OECD Japan | 3.2% | 0.7% | -1.6% | -0.3% |

| OECD US | -1.2% | -3.0% | -4.1% | 2.7% |

| Six month readings at 6-Mo Intervals: | ||||

| Recent six | 6-Mos Ago | 12-Mos Ago | 18-Mos Ago | |

| OECD | -3.0% | -3.1% | 2.7% | 1.6% |

| OECD7 | -3.1% | -4.5% | 2.2% | 0.9% |

| OECD Europe | -5.2% | -2.2% | 1.0% | 1.2% |

| OECD Japan | 0.7% | -3.9% | -1.9% | 1.2% |

| OECD US | -3.0% | -5.3% | 4.1% | 1.3% |

| Slowdowns indicated by BOLD RED | ||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief