Global| Jul 02 2007

Global| Jul 02 2007National PMI Up Slightly

by:Tom Moeller

|in:Economy in Brief

Summary

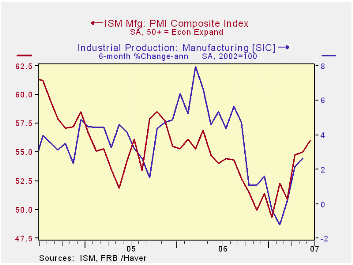

The national purchasing managers report for activity in July rose to 56 from an unrevised levels of 55 during June, according to the Institute of Supply Management. Strength in the sub-index of production was notable with a 4.6 point [...]

Strength in the sub-index of production was notable with a 4.6 point increase which was its largest monthly increase in two years.

New orders also rose but the gain was a moderate 0.7 points to a still high level of 660.3. Any reading above 50 indicates growth.

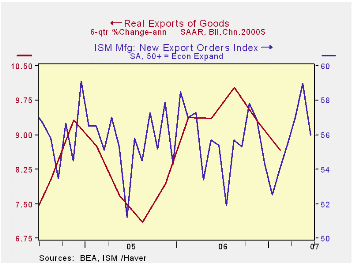

Export orders slipped three points but still indicated expansion in order books with a reading of 56.0. For the quarter, the index was at its highest level since 1Q06.

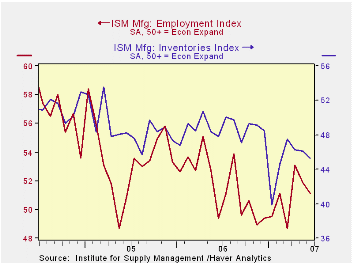

The employment index fell for the second consecutive month to 51.1.

New orders also rose but the gain was a moderate 0.7 points to a still high level of 660.3. Any reading above 50 indicates growth.

Export orders slipped three points but still indicated expansion in order books with a reading of 56.0. For the quarter, the index was at its highest level since 1Q06.

The employment index fell for the second consecutive month to 51.1. To the downside also were the speed of vendor deliveries and the inventories index which fell for the third consecutive month.

To the downside also were the speed of vendor deliveries and the inventories index which fell for the third consecutive month.Pricing pressure eased for the second month but the index remained at a high 68.0. That is up from the lows just below 50 during the last quarter of 2006.

| ISM Manufacturing Survey | June 2007 | May 2007 | June 2006 | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Composite Index | 56.0 | 55.0 | 54.0 | 53.9 | 55.5 | 60.5 |

| Prices Index (NSA) | 68.0 | 71.0 | 76.5 | 65.0 | 66.4 | 79.8 |

by Louise Curley July 2, 2007

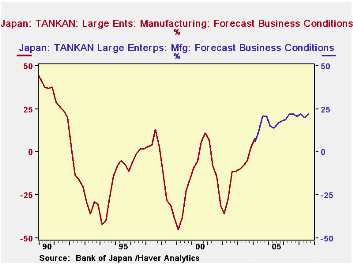

The Bank of Japan's quarterly Tankan Survey, or short term business outlook, was released today. The Bank surveyed 2,469 large, 2.915 medium and 5,455 small-sized enterprises over the period from May 28 to June 29.

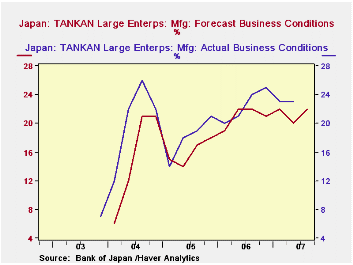

The headline series, a diffusion index for large manufacturing enterprises, rose from 20% in the March Survey to 22% in the current survey. The index has ranged between 20% and 22% since the second quarter of 2006 and has probably been the longest run of optimism manufactures have expressed since the late eighties. As noted in the Japan Data Base, major revisions in early 2004 have created a discontinuity in the time series data between December 2003 and March 2004. Pre revisions series are maintained in the data base and marked DISCONTINUED. Although they are not strictly comparable, we have plotted the DISCONTINUED and the current series in the first chart to place the current situation in a longer term perspective.

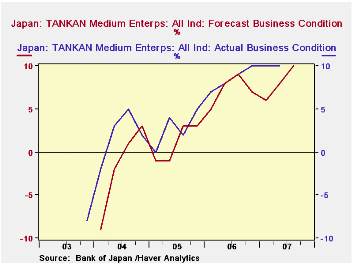

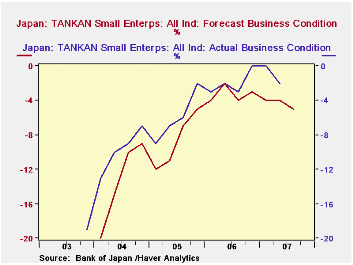

Caution on the part of the business men surveyed is evident in the fact that their forecasts have generally been below their appraisal of their actual results. The second chart compares the forecasts and appraisals of actual results for the large manufacturers. Optimists in medium-sized firms outweigh the pessimists by a margin of 10% in the current survey, but the margin has been rising as shown in the third chart. This chart also shows that medium-sized business owners, have also tended to forecast conditions below their appraisals of actual conditions. Small business owners are still pessimistic on balance. Although the degree of pessimism lessened significantly until mid 2006. it has since stagnated within a range of -2% to -4%%, as shown in the fourth chart.

| JAPAN'S TANKAN SURVEY | Q3 2007 | Q2 2007 | Q1 2007 | Q4 2006 | Q3 2006 | Q2 2006 | Q1 2006 | Q4 2005 |

|---|---|---|---|---|---|---|---|---|

| Forecast (Diffusion Indexes %) | ||||||||

| Large firms | ||||||||

| Manufacturing (HEADLINE SERIES) |

22 | 20 | 22 | 21 | 22 | 22 | 19 | 17 |

| Non Manufacturing | 23 | 23 | 20 | 21 | 21 | 19 | 17 | 16 |

| Medium-sized firms | 10 | 8 | 6 | 7 | 9 | 8 | 5 | 3 |

| Small firms | -5 | -4 | -4 | -3 | -4 | -2 | -4 | -5 |

| Actual Results (Diffusion Indexes %) | ||||||||

| Large firms | ||||||||

| Manufacturing (HEADLINE SERIES) |

-- | 23 | 23 | 25 | 24 | 21 | 20 | 21 |

| Non Manufacturing | -- | 22 | 22 | 22 | 20 | 20 | 18 | 17 |

| Medium-sized firms | -- | 10 | 10 | 10 | 9 | 8 | 7 | 5 |

| Small firms | -- | 5 | 7 | 8 | 9 | 10 | 10 | 10 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief