Global| Mar 27 2014

Global| Mar 27 2014Money Growth Prevaricates; EMU Credit Slips

Summary

New data available through February 2014 point to the continuing sluggishness in money growth and outright weakness in credit growth in the European Monetary Union. Mario Draghi, European Central Bank President, must wonder sometimes [...]

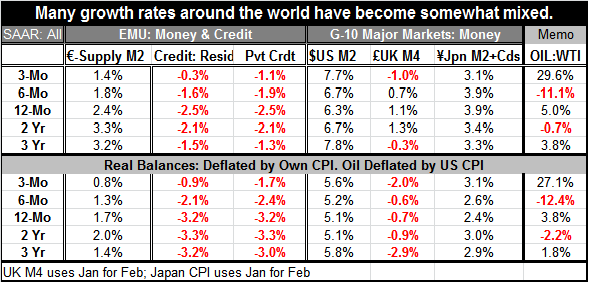

New data available through February 2014 point to the continuing sluggishness in money growth and outright weakness in credit growth in the European Monetary Union. Mario Draghi, European Central Bank President, must wonder sometimes if he is using an electric cattle prod on a dead horse. While the real sector shows some improvement, financial developments are still dodgy. Over three months credit is declining. The pace of decline over the last three months and six months is slightly less than the pace over 12 months and over the previous 2 to 3 years generally. Credit continues to be a special problem; it isn't expanding but it is contracting. Contraction is occurring at a slightly slower pace than it had been previously, but only slightly.

New data available through February 2014 point to the continuing sluggishness in money growth and outright weakness in credit growth in the European Monetary Union. Mario Draghi, European Central Bank President, must wonder sometimes if he is using an electric cattle prod on a dead horse. While the real sector shows some improvement, financial developments are still dodgy. Over three months credit is declining. The pace of decline over the last three months and six months is slightly less than the pace over 12 months and over the previous 2 to 3 years generally. Credit continues to be a special problem; it isn't expanding but it is contracting. Contraction is occurring at a slightly slower pace than it had been previously, but only slightly.

Money supply in the EMU is running a 1.4% annual rate pace over three months compared to 2.4% year-over-year. When we switch to look at real balances, money supply growth adjusted for inflation, we find that money growth is actually slowing down rather sharply in real terms. When we look at credit that same way, we continue to see a decline in real credit flows- but once again slower declines. So real credit declines are slowing their contraction, but real money growth rates are easing. This is true in both real and nominal terms.

Turning to other monetary center countries, they have mostly maintained their growth rate of money. In the US, there is a slight pickup to a 7.7% growth rate in M2 compared to 6.3% over 12 months. The UK, which had some very low money growth rate numbers, grew its M4 aggregate by 1.1% over 12 months and that now has weakened as M4 is falling at 1% at an annual rate over three months. The UK is a bit of exception to the notion that money supply growth is stable. In Japan, money supply growth of M2 plus CDs is up to 3.9% year-over-year and is only slightly weaker at 3.1% annualized over three months.

If we reload and look at these same aggregates in real terms, deflated by their own respective CPI indices, we see stability in the US with money supply that was growing 5.1% year-over-year picking up to just 5.6% over three months. In the UK, real balances are falling 0.7% year-over-year but are declining a little bit faster over three months at a -2% at an annual rate. Still, the UK has been looking at a string of declines for real balances that has not changed that much over three years. For Japan year-over-year real balance growth is 2.4% that's picked up a little bit to 3.1% over the most recent three months; an acceleration as opposed to the nominal deceleration.

All these economies continue to face particular bumps and bruises as we try to assess where they are and where they're headed in the coming months. Europe is showing an economic recovery, but there can be no doubt that its economic statistics have begun to oscillate. Germany has seen a setback in his Ifo index, as well as some weakness in its PMI sector gauges. France has showed some surprising growth in its PMI indices in both services and manufacturing. French consumer confidence has recently perked up, as has Italian confidence. But conditions in the euro area remain uneven even as it generally continues to show improving growth. Perhaps the biggest problem facing the euro area is psychological, having to do with the perceived risks from the circumstances involving Ukraine/Crimea. Certain sanctions have been placed on Russia and its economy is now expected to slip into recession around midyear. There will be knock on effects for European growth from that, although not severe effects, unless the game of imposing sanctions escalates.

The sanction game: where is the sweet-spot? The key element here seems to be to get the sanctions just right. The US and the other nations of the Western coalition want sanctions to be bad enough on Russia for it to feel the pain and to be pressured. But they don't want them to be so severe that Russia feels it has to retaliate in a way that could severely hurt the countries of Western Europe that depend so importantly on energy supplies from Russia. One counterbalancing factor is that Russia also depends on the revenues from those energy sales. Would Russia cut off its nose to spite its face?

Japan shows relatively steady nominal and real money growth with continued very low inflation. It still has the objective of stopping deflation and getting growth in gear. Along with a very accommodative monetary policy, Japan seems to promise a bottomless pit of stimulus. It is facing fiscal restrictiveness from its coming tax hike. There are concerns about how hard that hike will hit the economy and how effective monetary policy will be in the wake of this shock. Japan also is dealing with the fact that it had reoriented its pattern of commerce to trade more with China than with the US. But now the Chinese economy is performing more unevenly while the US is still gaining some traction. In addition, the generally weak state of world trade is keeping Japan from getting the kind of boost it would like to get from its export sector. Japan continues to struggle with its energy sector relying heavily on imports as it has shuttered its nuclear capability and the wake of the problems in Fukushima. Japan continues to face a tough challenge.

While the UK has the weakest and the most uneven money supply growth of the lot, it is the one economy in Europe that rivals Germany - for the moment. UK auto sales have been among the strongest the most consistent gainers across all of Europe. UK retail sales still appear to be in gear. Its sector indices on manufacturing and services continue to show relatively strong readings compared to the rest of Europe. The biggest concern in the UK seems to revolve around whether or not it's building another housing bubble or not. So far we have to judge the UK's economic performance as being quite good and to admit that the storm clouds still seem to be on the horizon and may yet dissipate. The Bank of England is not blind to this risk. The UK is still dealing with problems related to troubled financial institutions. It also is exposed to the Russia problems as there has been a number of Russian oligarchs committing substantial resources in the London financial markets. This activity has been curtailed over the past month.

The gamble on US growth: The US economy continues to do what it's been doing. Its growth is in gear. The second half of the year did produce a pickup in GDP growth. However, there continue to be big disagreements about how much the US economy is being harmed by bad weather. Economic data suggest that the pickup in the second half of the year came from inventory building which was followed by a period of weak consumer demand. As a result, the US now is in a position of having excess inventories, something that is made clear by looking at inventory versus sales growth rates across the various sectors over recent time horizons.

While there's no doubt that there was unseasonably harsh weather at the end of the year and at the turn into the New Year, it's still not clear how much that weather has adversely affected GDP. Early economic readings for March have not exactly snapped into place. At the same time, we continue to get evidence that the inventory overhang has gotten worse during this period although we don't yet see evidence that firms are cutting output sharply because of this. Instead, one implication seems to be weaker imports into the US. This is beneficial as lower imports help to support GDP growth for a time. The US also will be affected by the chilling in Ukraine mostly because it's the lead cold-warrior rather than because it is economically or geographically exposed.

Geopolitical fall out and what it means: One casualty of the crime in Crimea is that the G-8 meeting scheduled for Sochi has been scrapped. It has been replaced by the G-7 meeting around midyear- excluding Russia from membership in a club it coveted. In the interim US and Europe have something they can talk about uncommon terms of the Europeans are much more wary of the blowback from a tougher stand on Russia than is the United States.

Recently, the Baltic states particularly Lithuania, had indicated some concern that because of their large Russian speaking populations they too could become targets just as Crimea was for the same rationale that Russia used to expropriate that state. It has been suggested, but it's not clear if NATO or any Western nations are going to place troops on the ground in those countries as a more immediate deterrent.

One thing is clear, and that is that the world has changed since Russia has made its Crimea grab. Russia had been made a member of the G-8 and was ostensibly acting as a partner over the conflict in Syria helping to identify and to ship out the chemical weapons Syria had agreed to turn over. However, under Russian guidance it's clear that Syria has been moving slowly and now its actions look more disingenuous in the wake of statements made by Putin after executing the land-grab in Crimea.

When world geopolitics changes, the world's economies change: We had been in a period where multinational corporations roamed freely and formed joint ventures doing what they wanted with whoever they wanted, thinking that many of these historic rivalries were being put to bed and that we were headed in some fashion, at some speed, to a world that would be governed by more or less capitalist principles. What has happened in Russia certainly changes minds about the degree of risk in doing business there, the rule of law and the future of capitalism. The recent missile shots out of North Korea remind us of the actions of that lawless state. And as we reconsider the position of Russia we can't help but wonder about China, a country that already is saber rattling with Japan and the Philippines over territories it wishes to claim.

While this may seem a poor segue, all of this makes me wonder about the Federal Reserve policies and the FOMC's assumption that growth is going to continue to press ahead. These changes in geopolitics may have deeper impacts than what we now think. In Europe, Draghi is described as content with the way things are for now. But inflation in Europe is still too low as it is in the US. And in the US, the Fed is still tapering. We have to wonder if the upside risks to inflation are all in central bankers' minds? The world's economies are already on shaky ground. Our various financial sectors are still under the process of repair as central bankers continue to try to figure out a set of rules that can make the economy safe from bankers. We know that other challenges lie ahead; we don't know if instability lies ahead. It's a good time to keep in mind the interaction between economics and geopolitics. And for now, that thought is not reassuring.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.