Global| Sep 24 2019

Global| Sep 24 2019Minor, Meaningless, Bounce in German IFO

Summary

The German IFO gauge is weak and remains weak after a slight improvement logged in September. The current business situation reading improved to 24.5 in September from 21.9 in August and expectations overall ‘improved’ to -2.0 from [...]

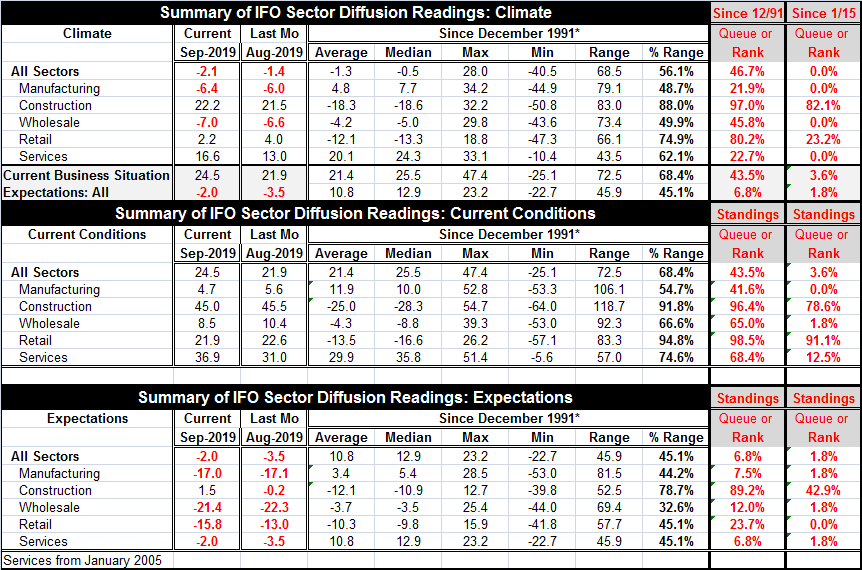

The German IFO gauge is weak and remains weak after a slight improvement logged in September. The current business situation reading improved to 24.5 in September from 21.9 in August and expectations overall ‘improved’ to -2.0 from -3.5. Expectations are weak on any timeline and while the current situation reading is above its mean and it is below its median in September. Only retailing and construction have values in September above their historic means and medians and only construction has an expectation value above its mean and median. That is the short synopsis of where the IFO stands.

The German IFO gauge is weak and remains weak after a slight improvement logged in September. The current business situation reading improved to 24.5 in September from 21.9 in August and expectations overall ‘improved’ to -2.0 from -3.5. Expectations are weak on any timeline and while the current situation reading is above its mean and it is below its median in September. Only retailing and construction have values in September above their historic means and medians and only construction has an expectation value above its mean and median. That is the short synopsis of where the IFO stands.

For perspective, I create two far right hand columns of rankings in the table. One ranks values since late-1991; the other ranks them on a short horizon from January 1995. The pivotal value for these rankings is 50% since that marks each indicator’s median on its relevant timeline. Ranking values above 50 indicate better than median performance; rankings below 50% indicate poorer than median performance. Of 18 rankings for the climate current and expectations readings, only 3 have values above the 50% mark since January 2015. However, over the longer timeline, 7 of 18 readings have values above the 50% mark. Even so, both of those are poor showings. Even on the long timeline, the count still indicates that more than half of the sectors have subpar performance.

Current conditions are still relatively upbeat. For current conditions, four of five sector readings have standings above the 50% market. The weak sector is manufacturing and it is weak enough to pull the all-sector reading below its median too. The highest reading is for the small construction sector followed by a huge 98th percentile reading for retailing. Retailing in Germany has been enormously and surprisingly resilient and strong. Wholesaling and services also have current standing readings above their respective historic medians. Only construction and retail also have above 50th percentile readings over the shorter span as well since January 2015.

For expectations, things change. Only one reading in the two timelines is above the 50% mark and that is for construction over the longer of the two timelines. Over the short timeline, all standings are in the bottom two percentile of their respective ranges except for construction. Over the longer timeline, all readings are below their respective 25th percentile except construction; for all weak sectors but retailing, the standings also are below their 10th percentiles.

The upshot is that current conditions in Germany have become much less buoyant by recent standards and that the weakness in manufacturing is severe enough to drag the all sector current index below its median even on a longer timeline. Construction and retailing are relatively and surprisingly resilient sectors for Germany. But expectations are weak any way you slice them and even the strong construction sector keeps its above median ranking only over the longer horizon. The rebound in the sector evaluation this month is minor. Current conditions are better only because of a rebound in services but even that may be suspect. In the Markit PMI survey, the services sector that had been engaged in a rebound was off relatively sharply in September. So there is some IFO-Markit discord on the services front. Expectations show some mixed improvement but only at such low levels that the fluctuation is meaningless. The German economy clearly remains in trouble. This report affirms that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief