Global| Jul 02 2008

Global| Jul 02 2008Markit Indices Continue to Show MFG Declines in Euro Area

Summary

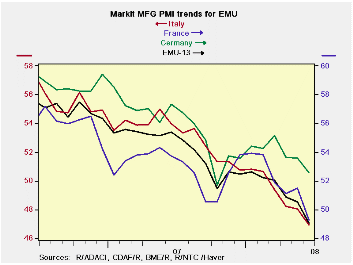

The June EMU MFG PMI moved below 50 for the first time since June of 2005. This signals EMU-wide MFG contraction. The dip comes ahead of a meeting of the ECB when it is expected to hike rates. EMU member finance ministers have been [...]

The June EMU MFG PMI moved below 50 for the first time since

June of 2005. This signals EMU-wide MFG contraction. The dip comes

ahead of a meeting of the ECB when it is expected to hike rates. EMU

member finance ministers have been warning the ECB of the potential for

a rate hike to turn growth negative in the e-Zone. Meanwhile, in the

interest rate and exchange rate sensitive MFG sector it already has

happened- at least by one measure.

Of the three largest EMU economies, two are registering

contraction in MFG by the Market PMI measures: Italy and France. The

Euro-Area’s strongest and largest economy, Germany remains in positive

territory – but is easing.

The Euro Area plus Italy and France show that the economy is

losing momentum at a rapid pace. Germany, on the other hand, has

rebounded from its weakest reading and is losing momentum at a slower

pace.

Still, the negative reading for the Euro Area's overall MFG

PMI does not make it easier for the ECB to do what it seems already to

have decided to do - that is to hike rates. Since the ECB began

considering a rate hike more seriously, inflation has overrun the ECB

ceiling by an even larger amount. Headline inflation is now is at more

that twice the pace that the ceiling allows, leaving the ECB chasing

after its own credibility. This is a race that the ECB is determined to

win.

| NTC MFG Indices | |||||||

|---|---|---|---|---|---|---|---|

| Jun-08 | May-08 | Apr-08 | 3Mo | 6Mo | 12Mo | Percentile | |

| Euro-13 | 49.16 | 50.60 | 50.74 | 50.17 | 51.27 | 52.25 | 37.2% |

| Germany | 52.56 | 53.57 | 53.62 | 53.25 | 53.93 | 54.18 | 60.3% |

| France | 49.24 | 51.48 | 51.12 | 50.61 | 51.91 | 52.07 | 31.7% |

| Italy | 46.91 | 48.05 | 48.24 | 47.73 | 49.01 | 50.57 | 24.2% |

| Spain | 40.61 | 43.79 | 45.19 | 43.20 | 45.42 | 48.21 | 0.0% |

| Austria | 48.39 | 49.76 | 49.83 | 49.33 | 51.31 | 52.71 | 32.6% |

| Greece | 53.81 | 53.77 | 54.38 | 53.99 | 53.08 | 53.50 | 63.6% |

| Ireland | 44.71 | 45.21 | 44.69 | 44.87 | 46.13 | 49.39 | 0.2% |

| Netherlands | 51.07 | 51.46 | 51.45 | 51.33 | 52.02 | 53.99 | 49.5% |

| EU | |||||||

| UK | 45.79 | 49.46 | 50.34 | 48.53 | 49.65 | 52.02 | 2.8% |

| percentile is over range since March 2000 | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.