Global| Jun 23 2021

Global| Jun 23 2021Markit Flash PMIs Show Most Improvement in Services

Summary

Of the six entries in the table, the June manufacturing PMIs stepped back in two of them (France & Japan) and are unchanged in another (EMU). The services gauge stepped back only in the U.K. After this month's data, the service sector [...]

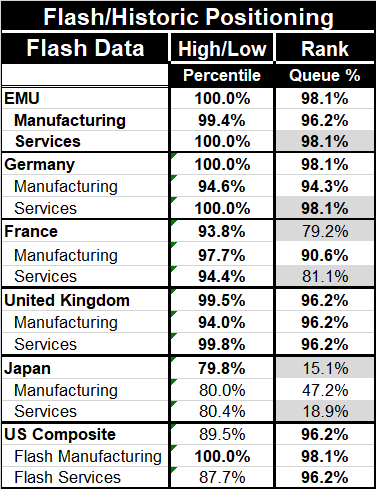

Of the six entries in the table, the June manufacturing PMIs stepped back in two of them (France & Japan) and are unchanged in another (EMU). The services gauge stepped back only in the U.K. After this month's data, the service sector percentile standings are equal to or above the standings of the manufacturing sector that has led this revival in three of six reporting entities (EU, Germany and tied in the U.K.). In the U.S., the services sector trails the red hot manufacturing sector by less than two percentile points in their rank standing. The raw diffusion score is greater for the services sector than for manufacturing only in the U.S. where that has been true for five months running and where service sector job growth has been reviving.

Of the six entries in the table, the June manufacturing PMIs stepped back in two of them (France & Japan) and are unchanged in another (EMU). The services gauge stepped back only in the U.K. After this month's data, the service sector percentile standings are equal to or above the standings of the manufacturing sector that has led this revival in three of six reporting entities (EU, Germany and tied in the U.K.). In the U.S., the services sector trails the red hot manufacturing sector by less than two percentile points in their rank standing. The raw diffusion score is greater for the services sector than for manufacturing only in the U.S. where that has been true for five months running and where service sector job growth has been reviving.

Get back!

Getting the services sector back on track is the most important goal to get the global economy back to normal. Services employ the bulk of the labor in developed countries. While having a manufacturing-led recovery was not a bad thing, as long as the virus kept people indoors mask-wearing and, for the most part, away from the services sector, the ability of a growing manufacturing sector to spread economic growth always was going to be severely limited. It has not been until vaccine use has stepped up and made it possible for people to mingle with a reduced risk of infection that the service sectors globally have been able to come to life. And in many places, vaccinations are not widespread enough to allow service sectors to revive fully.

Spare the vaccine, spoil the growth...

Japan is an example of less vaccine use: it has only 8% of its population fully vaccinated and only 19% with at least one shot. These are very low metrics for a developed country and especially for a country with such an aged population (the U.S. has 45.8% of the population vaccinated, the U.K. 47.2%. However, Germany that is doing quite well has only 32.5% vaccinated). Japan has the lowest composite standing by far in this group (15.1 percentile!) which is the product of a 47.2 percentile standing in manufacturing versus an 18.9 percentile standing for services. Japan's manufacturing sector is doing much better than its service sector but with its low rank standing the manufacturing PMI is barely above breakeven (its raw diffusion score is 51.5) and that is not going pull very hard on its services sector where the diffusion standing still shows contraction at a 47.2 raw diffusion score.

Double bests

Double bests

Only the EMU, Germany, the U.K. and the U.S. have top ten percentile queue standings (90th percentile standings) or above for both sectors as well as the composite. The EMU, Germany, France and the U.K. have top ten percentile standings for their high-low range percentiles. The U.S. just misses on this metric with its services sector at an 87.7 percentile for its high-low mark. That percentile pulls down the U.S. composite as well. Japan's sectors have high-low standings that cluster around the 80th percentile mark.

Context for PMI scores

All of these are simply statistics to try to positon the current PMI readings for you in different historic perspective. Manufacturing is expanding and prospering in most places listed in the table. The services sector that usually expands is expanding everywhere except Japan where economic restrictions have been kept in place to try to reduce the base of infections and make the country safe for the incoming Olympic games. Japan also has a low incidence of vaccination.

Accommodation is still the name of the policy game

Central banks in money center countries continue to pour on the monetary stimulus. Fiscal policy takes different forms in different regions, but policy continues to be highly accommodating. Several central banks on the monetary periphery have been raising their rates. There are no rate hikes from monetary center country central banks. The ECB has even ignored an overshoot of the headline HICP pace year-on-year. In the U.S., there is now a real debate about how much and when to cut its ongoing monthly securities purchases. Chair Powell continues to say that it is too early to even talk about talking about hiking rates. So while that eventuality may seem closer at hand as the Fed discusses changing security purchase practices, in Mr. Powell's view it is still way off in the distance.

Inflation is your friend or fiend?

Meanwhile, inflation has flared particularly in the U.S. and EMU and central banks are sitting on their hands calling the spike temporary and reversible. The Fed's mention of tapering (the decision to talk about it), however, had a powerful impact on markets pushing the yields on the U.S. 10-year government note lower. We have also seen some commodity prices particularly lumber and copper backtrack recently. If inflation were bubbling to a head, we would not expect to see backtracking in commodity prices. Market participants are taking sides over the prospect for inflation. But markets reacted and were ‘reassured' just by the Fed's decision to take tapering off the ‘do not talk about' list.

A complicated outlook

All of this simply paints a complex picture for central banks that remain frozen and perhaps even perplexed about how to act. No central bank wants to act too soon and cut off a recovery in progress. Yet, neither does one want to encourage inflation to accelerate and become established. There are arguments all over the place about this and about what to do. For now central banks remain largely watching events. We do not know what tolerances they have to act. But it is also clear that threats from the virus remain and policy cannot yet disregard the virus as a threat to growth. It is threat that is much diminished, but it is not gone. That is simply another aspect of difficulty for making any policy decision. Global policies seem to be on the cusp of some sort of a regime change. But it may be a change from a regime of heavy monetary and fiscal stimulus to a regime of an extended holding pattern for stimulus and less aggressive action. There is no telling how broad this ‘cusp' of policy tolerance may be. For now all central banks seem to be running the same policy of forbearance when it comes to viewing incipient inflation. We are all wondering how long forbearance will hold and if the incipient inflation will recede and unwind before forbearance wears thin and gets worn out.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief