Global| Feb 01 2017

Global| Feb 01 2017Manufacturing PMIs Turn Up But Bifurcation Remains

Summary

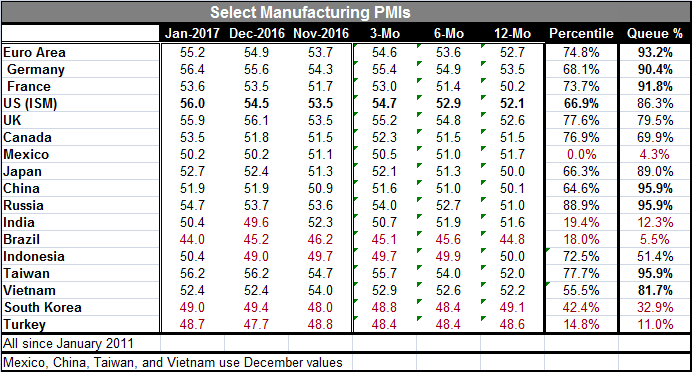

The statistical variation among the values of the countries that have reported their manufacturing indices has widened again this month. The dispersion has been greater than it is in January only 6% of the time since 1991. The most [...]

The statistical variation among the values of the countries that have reported their manufacturing indices has widened again this month. The dispersion has been greater than it is in January only 6% of the time since 1991.

The statistical variation among the values of the countries that have reported their manufacturing indices has widened again this month. The dispersion has been greater than it is in January only 6% of the time since 1991.

The most developed economies are making the clearest progress with a few exceptions. The euro area, Germany and France stand in the top 10% of their respective historic queues of values back to 1991. Taiwan has seen its manufacturing index stronger only 5% of the time. China and Russia are also high-ranking and have been better less than 5% of the time since 1991. For China though since it has been floundering on this timeline, this month's reading is a measure of improvement more than an indicator of strength. Japan has an 89th percentile standing. The U.K. has a 79th percentile standing. The U.S. has an 86th percentile standing (based on ISM manufacturing data).

Weakness is present in Mexico (4.3 percentile), Brazil (5.5 percentile), Turkey (11.0 percentile), India (12.3 percentile), and to a lesser extent in South Korea (32.9 percentile).

While the percentile standing of the U.S. manufacturing PMI is only moderately strong, its raw diffusion reading is one of the best and its 12-month change leads all countries in terms of its improvement. In terms of 12-month changes, Taiwan, Russia and Germany follow the U.S. lead.

In terms of weakness, Brazil, Turkey and Mexico have slipped the most in the last 12 months. Brazil and Turkey have had political problems while Mexico has been in the cross-hairs of the new Trump Administration in the U.S. and that has a desire to reform the NAFTA agreement and to stop U.S. firms from locating in Mexico at the cost of U.S. jobs. For Mexico, the outlook has deteriorated and the prospects are not good.

In the EMU, there are smiles all around as improvements and firm readings are widespread with few disappointments. Greek manufacturing took a step back and continues to show deterioration. The Dutch and Danish manufacturing indices backtracked but to still firm readings. Norway eased slightly along with Italy while manufacturing in Switzerland did skid to a four-month low. But on balance, the European story was a happy one. Euro area manufacturing has been better only 7% of the time since 1991. And manufacturing is on some sort of upswing. The rising tide is not lifting all boats, but it is lifting a lot of them.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief