Global| Jan 06 2014

Global| Jan 06 2014Manufacturing PMIs Rise Globally

Summary

The Markit purchasing data for EMU has been finalized as the final numbers confirm an upswing underway in the European Monetary Union. For the whole area itself, we see a clear progression of improvement as the 12-month average for [...]

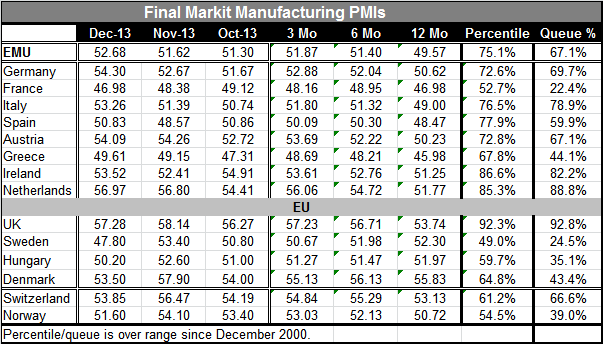

The Markit purchasing data for EMU has been finalized as the final numbers confirm an upswing underway in the European Monetary Union. For the whole area itself, we see a clear progression of improvement as the 12-month average for the manufacturing PMI stands at 49.57. It improves to 51.40 over six-months with the three-month average at an improved 51.87. This improving progression shows that recovery is ongoing.

The Markit purchasing data for EMU has been finalized as the final numbers confirm an upswing underway in the European Monetary Union. For the whole area itself, we see a clear progression of improvement as the 12-month average for the manufacturing PMI stands at 49.57. It improves to 51.40 over six-months with the three-month average at an improved 51.87. This improving progression shows that recovery is ongoing.

If we look to the EMU countries in the table, we see improving progressions in each one of them except France. This underlines the fact that there is an ongoing improvement in EMU. Improvement is spread across most of the members. France continues to be an issue as it has showed declines in its manufacturing PMI in each of the last three months and it shows negative changes over three months compared to six months and over six months compared to 12 months. France is clearly the country watch in EMU.

As for the EU and other members, we find only the UK logs progress over three months, six months and 12 months. Denmark shows deterioration over these periods. In Europe, but outside of the Monetary Union and the UK, the fortune of manufacturing is quite uneven.

Still, EMU is an important set of countries. The United States is engaged in a strong upswing along with EMU. Based on these developments, we would expect that the rest of Europe fall into line and joining upswing being enjoyed by the Monetary Union as well as by the US.

Not only do we have solid momentum in the Monetary Union and in the US but we also have a relatively strong level of activity. In the Monetary Union the aggregate manufacturing PMI stands in the 67th percentile of its queue. That means it is higher only about 33% of the time. However, some of the individual members are doing exceptionally well. The Netherlands stands in the 88th percentile of its historic queue. Ireland stands in the 82nd percentile of its historic queue. Italy stands in the 78th percentile of its historic queue. Germany stands in the 69th percentile of its historic queue. The aggregate figures are held down by the likes of France which stands only in the 22nd percentile of its historic queue, and Greece whose standing is in the 44th percentile of its historic queue, but is still making progress. Outside of EMU the UK's manufacturing sector stands strongest, in the 92nd percentile of its historic queue.

On balance there is reason for increasing optimism on the progress in Europe, in the US and in the outlook for growth globally. However, there is always a fly in the ointment. The services sector is not improving to the degree at the speed or with the breadth of manufacturing. For the Monetary Union as a whole, the services sector, at a diffusion reading of 50.96, is only in the 38th percentile of its historic queue. Its queue standing and strength are positioned far below that of manufacturing, however, like manufacturing, we see sequential strength as the services metrics improve from 12 months to six months to three months.

The Monetary Union again shows bifurcation when it comes to services standings. The standing of the Irish service sector is in the 92nd percentile of its historic queue, with Spain in the 79th percentile of its historic queue, and Germany in the 60th percentile of its historic queue. Once again, France is weak. Its standing is in the 14th percentile of its historic queue with Italy in only the 25th percentile of its historic queue. Services and manufacturing both are showing some uneven progress. Once again the UK has a strong showing as its service sector; its percentile standing is in the 87th percentile.

We give Europe positive marks for its showing in December and, as we see with the US, the manufacturing sector is leading. But also, as you see as in the US economy, the service sector is lagging significantly. For some reason services are not able to build the same degree of momentum that we are seeing in the manufacturing sector. This is a development that will have to change in 2014 if job growth is to return to anything like normal.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.