Global| May 01 2014

Global| May 01 2014Manufacturing PMIs Move Up in UK & Ireland; Declines in Netherlands

Summary

The Markit manufacturing indices for April show increases in the UK and Ireland and a decline in the Netherlands. Over three months very strong gains are registered in Ireland and the manufacturing index is up by 3.4 points with the [...]

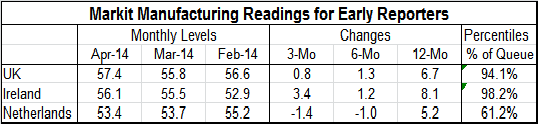

The Markit manufacturing indices for April show increases in the UK and Ireland and a decline in the Netherlands. Over three months very strong gains are registered in Ireland and the manufacturing index is up by 3.4 points with the UK up by 0.8 points. Over three months the Netherlands has lost 1.4 points.

The Markit manufacturing indices for April show increases in the UK and Ireland and a decline in the Netherlands. Over three months very strong gains are registered in Ireland and the manufacturing index is up by 3.4 points with the UK up by 0.8 points. Over three months the Netherlands has lost 1.4 points.

Over six months the UK is the leader, up by 1.3 points, but Ireland is up by 1.2 points, right on its heels. The Netherlands is trailing, still declining with its April 2014 index residing one point lower than it was six months ago.

Over 12 months Ireland is up 8.1 points, the UK by 6.7 points and the Netherlands by 5.2 points. Over 12 months the Netherlands has made substantial progress; however, over the recent six months there's been backsliding.

Ireland and the UK have some of the strongest manufacturing sector standings in all of Europe, according to the PMIs. The UK is in the 94th percentile of its historic queue while Ireland is in the 98th percentile, with its manufacturing sector stronger than its current level only 2% of the time. This is an extremely strong reading for Ireland and a very strong reading for the UK. By comparison the Netherlands reading is in its 61st percentile which implies that it lies 11 points above its historic median and at a relatively firm, but not a strong standing.

It's important to remember that these Markit surveys are based on some very useful diffusion calculations. The diffusion indices presented in the table give an accounting of responses to a survey. Those that indicate expansion get a count of one, those that are unchanged get a count of one -half and those that show declines are assigned a value of zero. The index is assembled by totaling the scores taken as a percentage of the total respondents. The diffusion index essentially tells you the proportion of companies that are expanding. The diffusion index is an indicator of breadth, not of strength, although there was a clear correlation between the two. Right now, for example, the UK economy is engaged in an expansion that's strong by the standards of European breadth, but UK GDP is still relatively modest. Yet, the UK manufacturing sector is knocking down a diffusion index that is only higher 6% of the time. Clearly having so many industries expanding is good news but just as clearly they are not expanding as strongly as they have other times in the past, and there are other times when the diffusion index was not as high yet industrial production growth was stronger.

Diffusion indices are very sensitive to changes in activity. This is why we like to use them to assess economic conditions. But we always have to remember that a diffusion index is an index of breadth, not an index of strength. It's a measure of relativity because it tells you how much better an indicator is doing this month compared to last month, but it doesn't tell you too much about how it's doing in absolute terms.

The earlier flash manufacturing readings for all of the euro area showed a slight step up from March which itself was a step up from February. Yet, the April level still sits below the level of January 2014. From August 2013 the manufacturing PMI has been improving on average by about a quarter one point per month. Of course, these improvements are not monotonic, but it's clear that the pace of increase has slowed. Over the previous eight months the average increase in the manufacturing index had been just about three quarters of one point per month. Since the manufacturing index has jumped over the level of 50, indicating expansion, the pace of improvement has slowed markedly.

The economy in Europe is still expanding. However, the pace of the expansion remains moderate. The pace of the manufacturing sector has slowed and the pace of the services sector expansion has slowed. However, during this time there's been much more excitement about the growth prospects in the euro area. Part of this has to do with the passage of the PMI indices over the level of 50. The manufacturing index did it in July 2013 while the services index did it in August 2013. In addition, of course, some of the struggling monetary union members have been posting positive GDP numbers like Spain which now has two positive GDP gains in a row. To be sure there has been progress by all the European Monetary Union members. Nonetheless, members continue to expand at different speeds and they continue to have different needs. Some continue to be much more self-reliant than others. If the European recovery is going to continue, the European community is going to have to be mindful of the differences and find a way to nurture its weakest members.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief