Global| Jan 14 2019

Global| Jan 14 2019Manufacturing PMI Weakens in Europe While IP Collapses

Summary

IP in context Industrial output in the EMU has just made its sharpest year-on-year drop in over five and one half years (when IP was engaged in a string of 20 straight months of year-on-year IP declines). The one-month drop of 1.7% is [...]

IP in context

IP in context

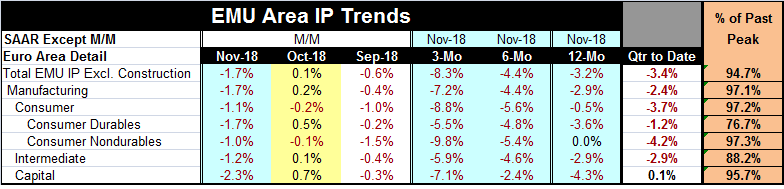

Industrial output in the EMU has just made its sharpest year-on-year drop in over five and one half years (when IP was engaged in a string of 20 straight months of year-on-year IP declines). The one-month drop of 1.7% is the largest in one and three quarter years; otherwise, we must go back over six years to find a deeper on month drop. Clearly, this sort of weakness is a rarity and deserves special attention.

IP by the numbers

IP in EMU (excluding construction) is falling at a 3.2% pace over 12 months, a sharper 4.4% pace over six months, and an even sharper 8.3% annual rate over three months. Its one-month drop is at a 22.7% annual rate. Manufacturing mirrors the monthly progression toward increasing weakness. Consumer goods do also with progressive deterioration visible for both durable goods output and nondurable goods output. Intermediate goods show an increasing progression to greater weakness as well but with a bit less ‘flare’ than for overall IP and for manufacturing. Only capital goods break the train of progressively weak output although that is a technical difference only. Over 12 months, capital goods output is even weaker than for IP overall and over three months it is only a tick less weak than for manufacturing. Capital goods output does, however, show slightly less weakness over six months than over 12 month but placed in context that does not seem like much of a difference or anything of significance.

Output also is uniformly weak in the quarter-to-date and falling so in all sectors except for capital goods where it grows at the minimalist compounded annual rate of 0.1%.

The point of the progressive growth rate calculation is that it demonstrates that the weakening is not a one-month sort of thing but that it has been in play for some time and with some depth. The progressive nature of weakness identifies it as ‘ongoing’ and still in its most virulent phase. The fact that the year-over-year weakness is the worst in over five and one half years – and getting worse- should put us on notice for something that is no garden-variety type of weakness.

I’m not sure that markets have grasped this yet.

The drop in IP for manufacturing is plotted on a matched up scale that lines up the zero points for IP and the PMI (0% for IP corresponds to 50 for the manufacturing PMI). IP’s year-on-year percentage gains are plotted vs. the Markit manufacturing PMI gauge. The PMI gauge is nowhere near as weak as IP. The PMI does not point to a decline in manufacturing output even though both the overall and manufacturing gauges for IP are showing horrific losses. We also see plotted on this graph the previous sharp drop in IP for early-2016, but at that time IP was slowing sharply from an overheated pace. Production reset then moved forward again. This time the drop in IP is sharp and occurs during a period of output deceleration. The drop puts output into a severe state of contraction. The parallels with early-2016 are poor and not at all reassuring.

Moreover, what we are witnessing is weakness everywhere, as we show above with the near uniform progressive deterioration in all sectors.

Tough times now and ahead

We know the geopolitical background is difficult.

• There is a trade skirmish in effect between the United States and China that could become a war.

• Russia has taken page out of China’s South China Sea book and has seized islands that both Russia and Japan claim.

• China has grabbed several Canadian citizens after Canada held an official of Huawei, a Chinese technology company, after the U.S. asked for extradition of that person. China now has a Canadian citizen in custody; it is charging that person with a drug crime and has upped the sentence to death.

• And there is now another Huawei employee that has been detained and is accused of spying in Poland.

• Of course, many think that the Crown Prince in Saudi Arabia has already gotten away with murder of reporter Jamal Khashoggi.

• And this is not the end of power politics in action. With Donald Trump pulling U.S. troops out of Syria, he has threatened Turkey to coerce it not to attack our allies, the Kurds that helped battle ISIS and will be left behind on their own. Turkey has pushed that threat aside leaving it as an open question whether the Kurds are at risk. If they are attacked, would Trump follow through with his threat against an important NATO member with crucial real estate value (location, location, location)?

• In the U.K., Brexit looks like it is poised for a revote and it increasingly appears that the EU’s hard line will succeed in ‘scaring’ the U.K. back into the fold and that could stop the rumbling of a possible new Scottish referendum as well.

No soft landing for the hard headed

The situation seems extremely risky. Stocks are behaving well despite being confronted with some severe consequences. Interest rate cuts would not provide much of a soft landing because the Fed will be as reluctant to use rates as a cushion as it was methodical in raising them in the expansion. The Fed will be wary of putting itself behind the zero rate bound eight-ball again. The economy’s problems, if a recession develops, will not be caused by interest rate hikes per se, but by exhaustion and playing out of the artificial fiscal stimulus that will begin to fade and because the trade war has taken a toll as well.

The cost of confronting China

No one ever said that challenging China would be easy or costless. But it has been well overdue. I think all you need to do is to look at the tone in the national debate to see how many have so quickly jumped off the ‘this-is-close-enough-to-free-trade’ bandwagon. But economists still do not agree with Trump’s desire for bilateral deals. Many just hate Trump too much to like anything he is doing. But China is feeling the pressure and its ‘Belt and Road’ ploy has been exposed for what it is – a tool of exploitation. I’d count this as a policy success despite its potential cost.

Forecasting the future

If we were to try to forecast the future and if we had behavioral equations for all the unknown economic sectors and countries and geopolitical threats, there would still clearly be far too many unknowns to reasonably solve for. There are too many things that we just can’t pin down that leave the future hanging by a thread. And I have not talked about the unsure state of the U.S. economy or its ongoing government shut down caused by two parties more interested in their own objectives and in ‘scoring points’ than in the impact on the country. But that alone probably says enough about it. The U.S. will issue its own regional Fed manufacturing surveys this week for Philadelphia and New York. The Fed’s index of industrial production will be released late in the week. We will know more then, but still probably not enough. It’s a sign of the times.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief