Global| May 12 2017

Global| May 12 2017Manufacturing PMI vs. EMU IP Growth

Summary

The manufacturing PMI continues to point to stronger growth while industrial production continues to plod along. Industrial production fell 0.1% m/m in March, the same as February. That hardly seems like what the PMI is referring to. [...]

The manufacturing PMI continues to point to stronger growth while industrial production continues to plod along. Industrial production fell 0.1% m/m in March, the same as February. That hardly seems like what the PMI is referring to. Welcome back to the dilemma of hard data-soft data.

The manufacturing PMI continues to point to stronger growth while industrial production continues to plod along. Industrial production fell 0.1% m/m in March, the same as February. That hardly seems like what the PMI is referring to. Welcome back to the dilemma of hard data-soft data.

Breadth, not strength

Diffusion surveys are indicators of breadth, not of strength, but we tend to project strength from breadth. In this case, that may not be so. Maybe the recovery in IP is spreading even with growth on the weak side.

Compare manufacturing to manufacturing and it still falls short

The manufacturing PMI is actually better compared to the manufacturing portion of IP index and there we do find monthly gains of 0.4% in February and in March. But even for manufacturing, the sequential growth rates are actually slowing from 12-month to six-month to three-month. There may be more growth in manufacturing than in overall production, but there is no acceleration the way that the PMI depicts it.

Timing asymmetry?

However, maybe we are just a few months away for seeing the revival. The chart at the top plots year-on-year manufacturing IP growth vs. the manufacturing PMI. There we see that, despite much greater volatility in manufacturing IP, the two series do seem to be more or less in sync. If IP were to pick up over the next several months, we would find the correspondence between these series largely restored.

IP volatility

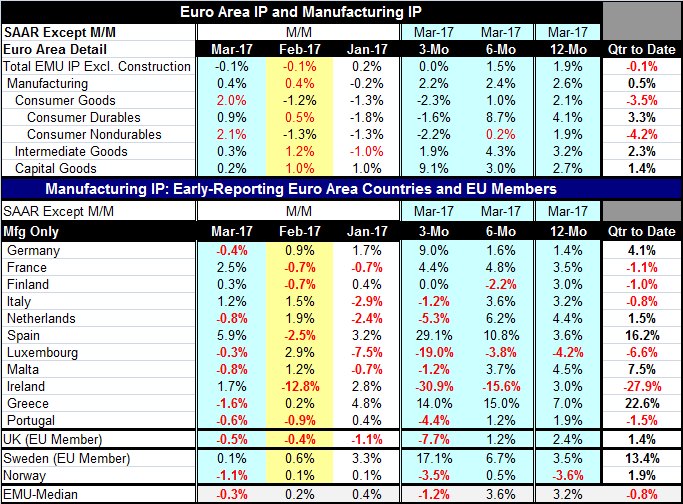

Euro area IP is volatile. Looking at individual countries, Spain has the most volatile IP by far, followed generally by Italy then by France with Germany among the four largest economies usually having the most stable IP. That gives us a second reason to emphasize German data. Not only is Germany the largest EMU economy, but its IP index has the best signal to noise ratio as well.

The veracity of the signals

On that score, unfortunately the German IP index is lower in March. However, more broadly, the German IP index is very hopped up over three months, growing at a 9% annual rate and it has accelerating growth rates from 12-month to six-month to three-month. Maybe this is a sign that the Markit PMI gauges are pointing us in the right direction. France and Spain each also show steady acceleration in IP on these horizons. It looks as though it's too early to throw in the towel on the PMI survey. Only Italy among the Big Four economies has a dodgy trend and that is all due to a decline in output over the most recent three months which is dominated by a sharp fall of IP in January. The country detail shows a lot more unevenness across the euro area.

Manufacturing performance and outlook

However, overall EMU manufacturing output in Q1 is rising at a solid 0.5% pace. Consumer goods output is falling at a 3.5% annual rate, but intermediate goods output is rising at a 2.3% pace and capital goods output is gaining at a 1.4% pace. While individual countries have their own demons to ward off, output for the euro area overall is still expanding at a healthy clip in Q1 and expanding in two of three principal sectors. There are always going to be country level issues in the EMU. There are just too many jurisdictions for them all to be on the same page at all times. As long as the recent weakness is the result of simple variability, there are no problems here. But overall IP growth is deteriorating and even manufacturing growth shows a slight slowing in place. It may be too soon to dismiss the month's weakness reported by individual nations and to embrace the overall manufacturing PMI signal or the German signal. There are still things to keep an eye in the euro area. I do not get the sense that the die has been cast one way or the other for good. Policy is unfolding. Brexit is still developing. Europe still has to make peace with the dissention among the electorate. Even though France made it through its elections with what seemed to be flying colors, the reality for Europe is that there are still deep divisions at every turn that still must be death within order to move ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief