Global| Nov 28 2018

Global| Nov 28 2018Little Changed in Paths of EMU Money or Credit

Summary

Globally, money supplies are decelerating to some extent with nominal M2 growth in the EMU a minor exception. All money growth rates decelerate from three-years to two-years to one-year. Only the U.K. and EMU have stronger growth over [...]

And the Tortured Path that Lies Ahead

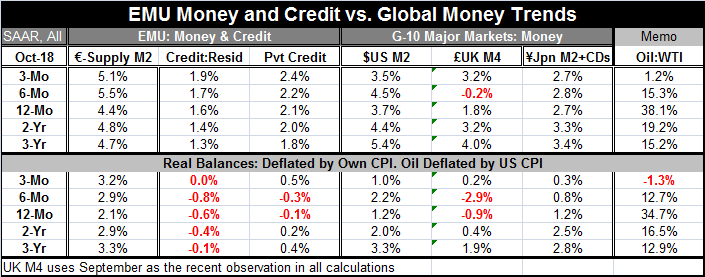

Globally, money supplies are decelerating to some extent with nominal M2 growth in the EMU a minor exception. All money growth rates decelerate from three-years to two-years to one-year. Only the U.K. and EMU have stronger growth over three months for money supply than over 12 months, although for neither does that seem very significant. For real money balances, all growth rates decelerate from three-years to two-years to one-year. Again the U.K. and EMU are exceptions for shorter growth rates as the only places where three-month real balance growth is faster than 12-month growth.

Globally, money supplies are decelerating to some extent with nominal M2 growth in the EMU a minor exception. All money growth rates decelerate from three-years to two-years to one-year. Only the U.K. and EMU have stronger growth over three months for money supply than over 12 months, although for neither does that seem very significant. For real money balances, all growth rates decelerate from three-years to two-years to one-year. Again the U.K. and EMU are exceptions for shorter growth rates as the only places where three-month real balance growth is faster than 12-month growth.

EMU Credit Growth

In the EMU, credit growth has been essentially stable with some technical claim to minor accelerations or short and longer terms horizons. But there is nothing stirring beyond ‘an acceleration’ of several tenths of a percentage point on annualized rates of growth. There is technical acceleration but nothing fundamental that you can build growth on.

The Oil Pulse

The impulse from rising oil prices is now turning to a negative one as oil prices decelerate from 12-months to six-months to three-months as growth rates drop from 34.7% to -1.3% and more of that is in train.

Nominal Global Money Growth

Nominal Global Money Growth

Nominal global money supply growth shows a growth rates of 1.8% over 12 months in the U.K. compared to 2.7% in Japan, 3.7% in the U.S., and 4.4% in the EMU. But as noted above, money growth rates have generally been slipping and generally are decelerating from 12-months to three-months. Three-month growth rates range from 5.1% in the EMU, to 3.5% in the U.S., to 3.2% in the U.K. and to 2.7% in Japan.

More on EMU Credit

In the EMU, credit to residents creeps higher from a pace of 1.6% over 12 months to 1.7% over six months to 1.9% over three months. However, discounted for inflation and recalibrated as growth rates in real money balances and these rates of growth show net declines in credit over 12 months and six months with flat performance over three months. Private credit is only slightly better off, showing an annualized net gain over the recent three months at a 0.5% pace.

Policy Moves and Economic Trends

Money and credit stimulus clearly does not amount to much. But globally, growth has been slipping and trade flows have been slowing. The OECD has issued a warning and its collection of leading indicators has been reinforcing the outlook for weaker conditions. In the U.S., the President is complaining about the rapidity of Fed rate increases. In Europe, Mario Draghi has repeated that the policy of QE will come to an end at yearend.

In the U.S. as the Fed stays on its rate hike path, rates are getting higher as the effect of fiscal stimulus is wearing off. Interest sensitive sectors already are showing the strain much to the Fed’s surprise. To compensate, there is less of a drain on consumers and businesses from oil prices. But since the U.S. is also an oil producer, that may have a way of coming out in the wash as the benefit to consumers is a transfer from producers whose importance has grown in the U.S. and whose investment plans could well be curtailed if oil prices fall by enough.

U.S. Policy: As the Global Keystone...or Headstone?

U.S. policy is at the center of the global policy storm as the Trump pressures over trade have dominated trade talk and are largely responsible for trade flow slowing. The Trump rhetoric continues to ratchet higher. Meanwhile, it is wholly speculative whether or not the U.S. and China will cut a trade deal on the sidelines of the summit being held in Argentina. While global conditions that feature plunging oil prices and weakening stock prices would seem to send a clear message about growth prospects and the state of global demand, central bankers are not making cyclical policy. They are making structural policy. The ECB is going ahead with its plans to terminate QE. And in the U.S., there is no sign that that the central bank has chosen a more moderate rate profile in view of unfolding economic events. All eyes are on the Fed and all are curious as to whether the Fed will hike rates in December and about what its rate guidance will look like at its next meeting.

Brexit...Godot

Europe and the U.K. await the vote by the U.K. parliament on the pending Brexit plan. Anything goes there and we know that we cannot be reliably guided by opinion polls. So we wait and wait…

Firmness in Pursuit of Fairness – The end of Sugar-Daddy

Globally, growth ramps down as the U.S. has been demanding more fairness in trade. The rest of the world mostly opposes changes apparently as though the U.S. is expected to remain sugar-daddy to the world. We see plenty of examples of the old post-war alliances dealing with policy rifts. That is to be expected as wartime relationships shift and as national identities are reestablished. And while Germany has been reunited, it has not been reestablished as a military power. Still, it is dominating Europe as an economic power and one whose ‘growth’ model has been oppressive for fellow EMU members. Germany continues to impose its will on Europe while everyone else is screaming about ‘America First’ policies. It is curious how in the Post War period the U.S. could be so generous. But as this process of repair from the war has evolved, everyone thinks it is business as usual to run their own selfish policies but see the U.S. as tyrannical when it begins to put its own interests first or simply to demand equal treatment or that allies pay their own way especially for defense services provided. We are 70 years on…except for the Koreas, of course. When do you stop nursing the baby?

Free Trade or License to Exploit?

Under free trade, the global economy could have become a perpetual motion machine. But when that machine is jimmied and when countries put up selective barriers or control their exchange rate to determine an outcome and when some countries turn into perpetual surplus countries and others transform into deficit countries, the sustainability of that configuration has been destroyed. RIP Free Trade. Currencies must move and must be able to rebalance current accounts. Trade is a crucial feature of this system and it cannot be hijacked by national objectives. China and other Asian countries have done this to expedite and assure development. At first it was a post-war strategy, but it has become codified and many believe that running a trade surplus is now their right! But it’s wrong. That in fact is a free-trade killer. No country can run deficits forever as part of trade system.

Too Much Too Fast

The shift of resources from West to East (from deficit to surplus countries) has been too fast and has threatened the economic prosperity and social stability in the West. Too much wealth has been transferred and too many jobs have been lost in too short a period of time. That is largely because China, a massive country, has waited so long to develop then has sought to catch up in a virtual instant. Can China deal with slower growth? Can it deal with more balanced growth? Its ‘Belt and Road’ project is not geared for that. It is a program of old-fashioned trade dominance. China like Germany seems to seek economic dominance more than fairness.

New Watchword: FAIRNESS

I would say that the U.S. push for trade fairness has come just in time if not too late. But as always, time will tell. I think it is time to rethink who are the bad guys in this international trading system and to put all players on fair and equal footing. Unfortunately, it may be too late to do that with China because of its socioeconomic policies that now preclude a market-determined exchange rate, Chinese political repression and information control have left it with a more affluent population willing and eager to get financial assets - if not themselves- out of the country. And China is so large that such migrations of money or people would burden the economic system and dominate the exchange market. Capital controls in China are probably here to stay and that will be the ultimate roadblock to true free trade. So make no mistake about it. We blew it. We had a chance for free trade, but instead countries co-opted it and used trade to fulfill nationalistic objectives. And now free trade will no longer be an option. We are headed into a new realm of bargained trade. Get ready, ‘cause here it comes… and it is not just Donald Trump. It is the new reality.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief