Global| Mar 29 2017

Global| Mar 29 2017La Dolce Vita? Italian Confidence Bumps Higher

Summary

Italian business and consumer confidence moved higher in March. Business confidence is on a four-month string of month-to-month improvements. Consumer confidence is making a rebound after falling in both January and February. Business [...]

Italian business and consumer confidence moved higher in March. Business confidence is on a four-month string of month-to-month improvements. Consumer confidence is making a rebound after falling in both January and February. Business confidence is up on strength in total orders and foreign orders. Consumer confidence is up despite a series of ups and downs among components that often offset and contradict one another but ultimately show net gains.

Italian business and consumer confidence moved higher in March. Business confidence is on a four-month string of month-to-month improvements. Consumer confidence is making a rebound after falling in both January and February. Business confidence is up on strength in total orders and foreign orders. Consumer confidence is up despite a series of ups and downs among components that often offset and contradict one another but ultimately show net gains.

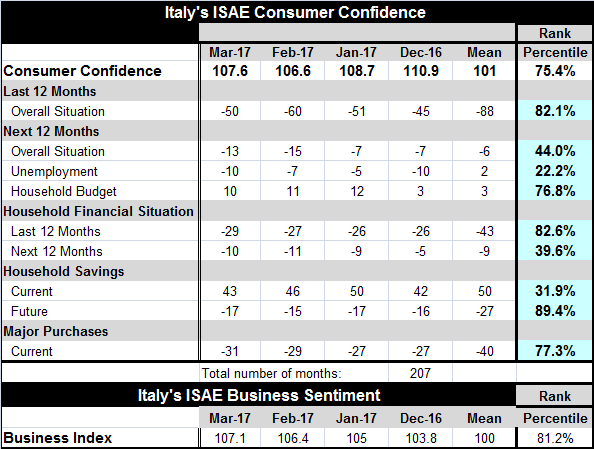

The levels of confidence find consumer confidence with a 75th percentile standing in its historic queue of data. Business confidence is slightly more elevated with an 81st percentile standing. These are solid-to-strong readings for confidence and are surprisingly firm for a country undergoing the economic and political turmoil that Italy is experiencing along with banking sector issues. I'm not sure if it demonstrates the resilience or the blase nature of the Italian people. But there is some buffering agent between consumers and their perception reality.

The overall situation for the consumer over the past 12 months has a relatively strong rating that has been higher historically less than 18% of the time. The raw diffusion index that corresponds to that ranking jumped by 10 points this month.

Over the next 12 months, the overall situation gauge is two points stronger, but it is still below its January level. The standing of the index is a much weaker 44th percentile - a level that is below its historic median. Looking backward one year the overall situation has improved and is only higher 18% of the time, but looking ahead the overall situation is only slowing improving and has a below median standing. All in all, this is not a very strong position for the consumer with such weak readings for the next 12 months ahead. The expectation for unemployment fell by three points in March, representing an improvement (reduction) in a fear-reading that is lower historically 22% of the time (a nice margin but still a draconian event that is feared at the one-fourth to one-fifth probability level - that's not small enough for true comfort. The household budget took a minor setback falling to 10 from 11 while logging a firm 76th percentile standing.

The look back and look ahead situation with the household budget is mixed. Over the last 12 months the financial situation had an 82nd percentile standing; looking ahead it has a much weaker 39th percentile standing. However, the backward looking index weakened in March while the forward-looking index improved slightly. That's a plus of sorts.

Household savings show the temporal configuration with current savings at a much weaker (31%) standing than future savings (89%). But in this case, both the current and the future savings readings weaken in March compared to February.

While the major purchase index has a relatively firm 77th percentile reading, the index slipped in March and has weakened in each of the last two months.

Despite a relatively solid standing for the consumer sector's overall gauge of sentiment, the details of the consumer survey give us a definite sense of the uneven situation consumers are making the best of. This seems to be less of a survey that illustrates the underpinnings of the mood of the consumer than one that shows us the consumers' fragility and lingering vulnerabilities. La dolce vita? Not.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief