Global| Aug 03 2007

Global| Aug 03 2007July Payrolls a Bit Light, Revisions Minor

by:Tom Moeller

|in:Economy in Brief

Summary

Nonfarm payrolls grew 92,000 during July. The increase was a bit below the Consensus forecast for a 128,000 rise and the prior two months' gains were revised slightly downward. The three month change in payrolls slowed to 135,000 on [...]

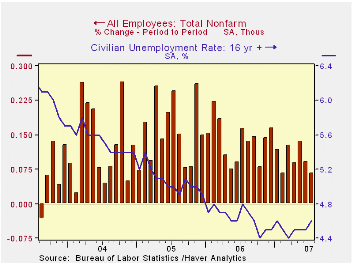

Nonfarm payrolls grew 92,000 during July. The increase was a bit below the Consensus forecast for a 128,000 rise and the prior two months' gains were revised slightly downward.

The three month change in payrolls slowed to 135,000 on average. That's about equal to the 136,000 average change so far this year but below the average of 189,000 last year and 212,000 during 2005.

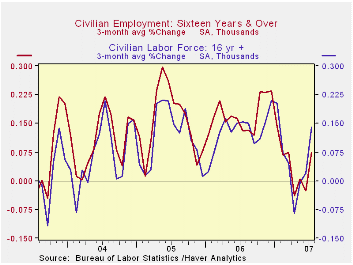

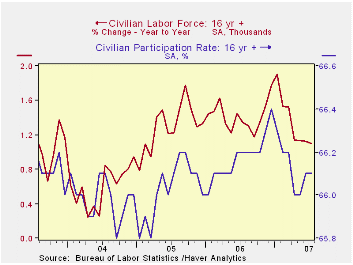

The unemployment rate moved up to 4.6% last month from 4.5% during June. Household employment fell 30,000 (+1.2%) following a 197,000 rise during June. The labor force jumped another 159,000 (1.1% y/y). The labor force participation rate held steady at 66.1%.

From the establishment survey, private service sector jobs posted a 132,000 (2.0%) gain after a 114,000 June rise which was revised slightly higher. Last year’s average gain was 159,000 per month. Retail employment actually fell a modest 1,200 (+0.5% y/y) during July and the average this year has been just 8,000 per month after an outright decline of 2,700 per month during 2006. In the financial sector, jobs recovered from the prior month's 2,000 decline and grew 27,000 (1.4% y/y) for an average gain of 7,000 this year versus 16,000 last year. Professional & business services employment rose 26,000 after June's upwardly revised 7,000 increase. The average gain this year has been 19,000 per month, off from last year's average of 42,000.

Factory sector payrolls fell 2,000 (-1.2 y/y) and jobs have fallen in every month during the last twelve. Construction employment reversed the prior month's downwardly revised 3,000 increase with a 12,000 (-0.7% y/y) decline. Construction jobs have fallen 5,000 per month this year versus an average 11,000 increase per month during 2006.

Government payrolls fell 28,000 (+1.1% y/y) and in 2007 have risen an average 16,000, near the per month average last year of 20,000.

Average hourly earnings increased 0.3% and the 0.4% gain in June was upwardly revised. Factory sector earnings rose 0.3% (3.0% y/y) and private service producing earnings rose a firm 0.4% (4.1% y/y) after June's upwardly revised 0.5% increase. The monthly average increase in overall average hourly earnings this year has been 0.3% versus, down from 0.4% per month last year.

Phillips Curve Instability and Optimal Monetary Policy from the Federal Reserve Bank Of Kansas City is available here.

| Employment | July | June | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Payroll Employment | 92,000 | 126,000 | 1.4% | 1.9% | 1.7% | 1.1% |

| Manufacturing | -2,000 | -13,000 | -1.2% | -0.2% | -0.6% | -1.3% |

| Average Weekly Hours | 33.8 | 33.9 | 33.9 (July '06) | 33.8 | 33.8 | 33.7 |

| Average Hourly Earnings | 0.3% | 0.4% | 3.9% | 3.9% | 2.8% | 2.1% |

| Unemployment Rate | 4.6% | 4.5% | 4.8% (July '06) | 4.6% | 5.1% | 5.5% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief