Global| Jun 28 2007

Global| Jun 28 2007Japan’s Industrial Production Falls by 0.4% Third M/M Drop in a Row

Summary

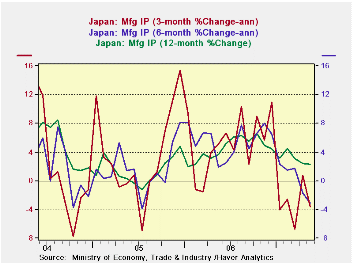

Japans industrial output trend is slipping as it has fallen for the third month in a row. The data show a steady deterioration in both short term and Yr/Yr trends. Still, Japanese officials are not worried. They see a snap back in [...]

Japan’s industrial output trend is slipping as it has fallen for the third month in a row. The data show a steady deterioration in both short term and Yr/Yr trends. Still, Japanese officials are not worried. They see a snap back in the months ahead. Japanese officials are convinced of ongoing demand for Japanese made electronics. A METI survey looks for output to be up by 1.9% in June and 1.7% in July. For the time being Japan's nonmanufacturing economy is carrying growth ahead, much as it has done for the US when MFG slumped. Japan’s IP still is up by 3.7% Y/Y – but is slowing.

Despite the upbeat posture by METI, and recent comments made by the BOJ’s Fukui, the risk seems palpable and greater than the official positions admit. Fukui is worried that the output gap has been pressured too much to relieve the zero inflation situation, as his view is just one example of how Japan continues to take an optimistic view of economic events. The BoJ is ostensibly worried about causing a boom/bust cycle but doing so with no evidence of a boom at all. Growth is in fact barely moderate as the BoJ worries about the size of its output GAP and finds that the economy has been growing beyond potential for some time; Fukui says that the Japanese economy has been growing above its potential of 1.5% to 2.0% in the past few years, boosting production capacity and causing labor shortages, which has resulted in tighter supply and demand conditions. But this has gotten no traction on prices. Still Japan’s central bank is worried about overheating in the midst of a mild frost and METI is sure of rebound even as production suffers a series of setbacks.

| M/M % | SAAR % | Yr/Yr | |||||

| May-07 | Apr-07 | Mar-07 | 3-mo | 6-mo | 12-mo | Yr-Ago | |

| Mining & Manufacturing | -0.4% | -0.2% | -0.3% | -3.3% | -3.1% | 2.3% | 3.7% |

| Total Industry | -0.6% | 0.3% | -0.1% | -1.8% | -2.7% | 2.3% | 3.7% |

| Manufacturing | -0.4% | -0.2% | -0.4% | -3.7% | -3.1% | 2.3% | 3.7% |

| Food & Tobacco | 0.0% | -0.6% | 1.5% | 3.5% | 1.3% | 0.4% | -0.2% |

| Textiles | 0.3% | 0.0% | -2.1% | -6.9% | -4.7% | -4.1% | -3.5% |

| Transportation | 4.3% | -2.4% | -1.4% | 1.5% | -2.5% | 9.5% | 4.8% |

| Product | |||||||

| Consumer Goods | -3.5% | 0.6% | -2.1% | -18.3% | -8.2% | -1.5% | 2.1% |

| Intermediate Goods | -0.4% | -0.3% | 1.0% | 0.7% | -1.7% | 4.2% | 5.8% |

| Investment Goods | 1.7% | 0.6% | -2.9% | -2.3% | -1.0% | 2.2% | 0.8% |

| Mining | 0.2% | 0.4% | 0.9% | 5.8% | 3.5% | 6.2% | 2.4% |

| Electricity & Gas | -1.7% | 2.0% | 2.6% | 12.1% | 0.5% | 2.6% | 4.3% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief