Global| Nov 29 2017

Global| Nov 29 2017Japanese Retail Sales Refuse to Perform

Summary

Japanese retail sales sank in October. Nominal retail sales have dropped month-to-month in four of the last six months and in two of the last three months. There is sequential deterioration in nominal retail sales growth as the three- [...]

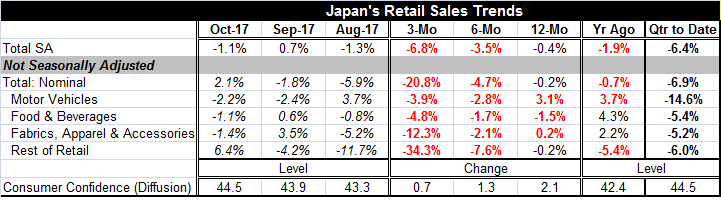

Japanese retail sales sank in October. Nominal retail sales have dropped month-to-month in four of the last six months and in two of the last three months. There is sequential deterioration in nominal retail sales growth as the three-month pace is -6.8%, below the six-month pace of -3.5% which is below the 12-month pace of -0.4%. The entire sequence of growth rates is negative and the trajectory is troublesome. After a long string of nominal declines, year-over-year nominal retail sales growth had turned positive around mid-2016. But now in October, year-on-year retail sales growth is showing a year-on-year decline again. Japan's retail sales are only able to rise in fits and starts.

Japanese retail sales sank in October. Nominal retail sales have dropped month-to-month in four of the last six months and in two of the last three months. There is sequential deterioration in nominal retail sales growth as the three-month pace is -6.8%, below the six-month pace of -3.5% which is below the 12-month pace of -0.4%. The entire sequence of growth rates is negative and the trajectory is troublesome. After a long string of nominal declines, year-over-year nominal retail sales growth had turned positive around mid-2016. But now in October, year-on-year retail sales growth is showing a year-on-year decline again. Japan's retail sales are only able to rise in fits and starts.

Japanese signals remain mixed. Nominal money supply has picked up its pace slightly, but real money supply (M2 plus CDs) has slowed compared to its earlier and longer term pace. Japan's manufacturing PMI (prelim) has trended higher in November to post a top 11 percentile standing in its six-year queue of data dating back to January 2012. The service sector PMI (updated through October) has been even stronger on a ranking basis. Despite the strength on the output side, the consumer side is struggling. Asia has been struggling recently even as the U.S. and Europe have been showing signs of increasing growth or of a broader pick-up.

Japan's consumer confidence is not the source of the problem. While the consumer confidence diffusion index is still below its breakeven value of 50 (it is presented as a diffusion index), that gauge has been improving. It is rising at a 2.4% annual rate early in Q4 over its Q3 average level and it is up by 5% over 12 months. The consumer confidence index is up for two months in a row and it is at its highest value in 29 months. Even though Japanese consumer confidence is not even fully restored to its neutral setting, it has been on a long run of improvement.

Still, retail spending is not back on pace. Even though the data by detail are not seasonally adjusted, it is disturbing to see that motor vehicle sales, food & beverage sales, fabric, apparel & accessory sales and the rest of retailing all are categories showing clear sequential decelerations in their pace of sales and that all categories show negative growth as over three months as well as over six months.

As the IMF is more upbeat and the Fed stays ensconced on its tightening path and while the ECB makes plans for less accommodation, Asia is still lagging. Japan's largest trading partner is China followed by the U.S. China is still struggling to reach its growth objectives. And while U.S. growth is doing better, it is not dynamic growth and its current investment-demand led incarnation is very skewed to investment in the oil patch.

Japan's long program of stimulus is still vying to get traction for economic growth. There seems to be some degree of success in the BOJ's program judging from the performance of Japanese consumer confidence. But getting consumers to actually step up spending has been a harder row to hoe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief