Global| Mar 22 2017

Global| Mar 22 2017Japan's Trade Trends Turn Sharply Higher; Much of the Gain Is Recent; Much of that Is in Prices

Summary

Japan has logged its largest current account surplus since April 2010. The 2011 Tsunami led to a nationwide nuclear power plant shut down, increasing oil imports and depressing the trade position in its aftermath for an extended [...]

Japan has logged its largest current account surplus since April 2010. The 2011 Tsunami led to a nationwide nuclear power plant shut down, increasing oil imports and depressing the trade position in its aftermath for an extended period of time.

Japan has logged its largest current account surplus since April 2010. The 2011 Tsunami led to a nationwide nuclear power plant shut down, increasing oil imports and depressing the trade position in its aftermath for an extended period of time.

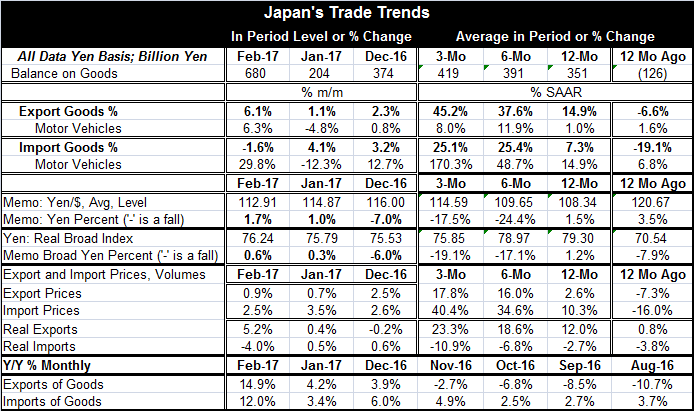

As the chart shows, both exports and imports are now growing very rapidly again. Surging oil price is a factor, but the strength in exports shows that it is much more than that.

The yen is higher vs. the dollar by a small margin (1.5%) year-on-year, but over the last three months and six months, it is falling rapidly again. The broad trade weighted yen is acting more or less the same as the yen vs. the dollar on this timeline.

Accounting for higher nominal values, both export and import prices are rising rapidly. Export prices are up by 2.6% over 12 months and import prices are up by 10% over 12 months. Over three months, export prices are surging at a 17% annual rate while import prices are gaining at a 40% annual rate. Taking away the effects of inflation, real exports are up by 12% over the past year while imports are lower on balance by 2.7%. Over three months, export volume is surging at a 23% annual rate and import volume is falling at nearly an 11% annual rate.

The real trade flows tell us of a pick-up in Japan's external demand as export volume kicks up to show growth. Japan's two largest export markets are China and the United States. However, domestically, since import volume has not stepped up, that is raising questions about the evolution of Japan's domestic demand.

Also released today was Japan's all-industry index for January. It rebounded to rise by 0.1% but only after dropping by 0.2% in December. That is still a weak performance on balance. And Japan's supermarket sales fell in February from their year-ago level. These are not good indicators for domestic revival and pose significant counterpoints to the apparent upbeat message in the headline for the trade report.

It is not yet clear if exports are a reading of strength in the trade report that we can take to the bank or not. Exports are up by a strong 14.9% year-on-year, but that compares to year-on-year gains of just 4.2% in January, 3.9% in December and -2.7% in November. The revival in Japan's exports is for the most part a one-month affair. We will want to see if this strength is corroborated in the next few months. For now it is more of an encouraging sign. Imports similarly were showing nominal year-over-year gains of 2.5% to 6% since October of last year and the spurt to a 12% gain in February is out of blue and all a mate of price not volume. We will want to track these result to see if a change is really afoot or if this is just more volatility during a time of rising and unstable oil prices.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief