Global| Sep 22 2005

Global| Sep 22 2005Japan's Trade Surplus Shrinks; Petroleum Is Only Part of the Reason

Summary

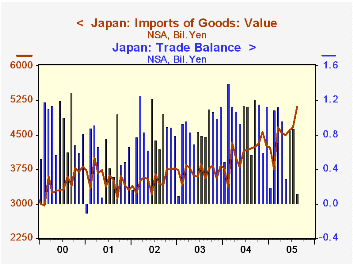

Japan's trade surplus shrank markedly in August from a year ago, reaching ¥116.3 billion from ¥572.9 billion. Exports grew vigorously, up 9.1%, but imports leaped 21.1%. As might be expected, petroleum accounted for a significant [...]

Japan's trade surplus shrank markedly in August from a year ago, reaching ¥116.3 billion from ¥572.9 billion. Exports grew vigorously, up 9.1%, but imports leaped 21.1%. As might be expected, petroleum accounted for a significant proportion of the import growth. Crude oil, refined product and other related gas products totaled ¥1,240.0 billion compared with ¥899.7 billion in August 2004. Press reports highlight this item, which is certainly large and likely to get larger. However, non-petroleum imports were also up considerably, by more than 16% over a year ago. This growth was spread across a number of goods categories.

Frequently, in interpretations of a nation's economic performance, imports are viewed negatively. The country is incurring additional foreign debt, or in Japan's case, reducing its domestic surplus in buying from abroad. Of course this is so, but that development has another, more favorable aspect: increasing imports can be a signal of rising demand. In fact, data on Japan's GDP through Q2 show gains in real terms for household spending, government consumption and private investment in plant and equipment. So demand has been expanding for the general kinds of merchandise being imported. The growth in August seems a strong hint that this continued into Q3.

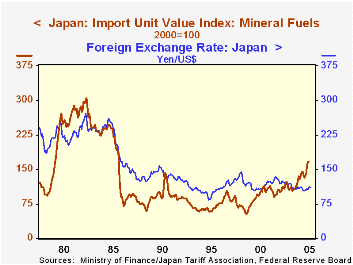

At the same time, we don't want to set aside concerns for Japan from surging energy costs. Nearly all of Japan's energy products are imported, so there is a potential for stress on the Japanese economy as oil and gas prices stay high. In that regard, it is interesting that despite the high dollar price of oil, the unit value of petroleum imports for Japan is less than in the prior energy "crisis" in the early 1980s, as seen in the second graph (although later data will no doubt show the unit value higher than the level in the graph, which is only through June). The difference of course is the exchange rate; the much stronger yen is holding back the yen cost of the petroleum. It's a small favor in the otherwise tenuous Japanese economic environment, but it can moderate the impact of the burdensome energy expenses.

| Japan Trade Not seasonally adjusted Bil. ¥ | Aug 2005 | Jul 2005 | Aug 2004 | Monthly Averages|||

|---|---|---|---|---|---|---|

| 2004 | 2003 | 2002 | ||||

| Exports | 5219.2 | 5536.9 | 4785.5 | 5097.5 | 4545.7 | 4342.4 |

| Imports | 5103.0 | 4666.6 | 4212.5 | 4101.4 | 3696.8 | 3518.9 |

| Balance | 116.3 | 870.3 | 572.9 | 996.1 | 848.9 | 823.5 |

| Petroleum Imports* | 1240.0 | 1059.3 | 899.7 | 798.1 | 717.2 | 615.7 |

| China: Balance | -287.1 | -183.1 | -206.7 | -183.7 | -174.6 | -229.0 |

| US: Balance | 486.7 | 649.5 | 474.4 | 580.6 | 548.9 | 636.3 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief