Global| Oct 19 2020

Global| Oct 19 2020Japan's Trade Surplus Grows

Summary

Japan has a string of three-monthly surpluses in a row, the first such string since 2017. Both export and import trends have been declining with both flows generally falling since late-2018 or early-2019. While year-on-year trends [...]

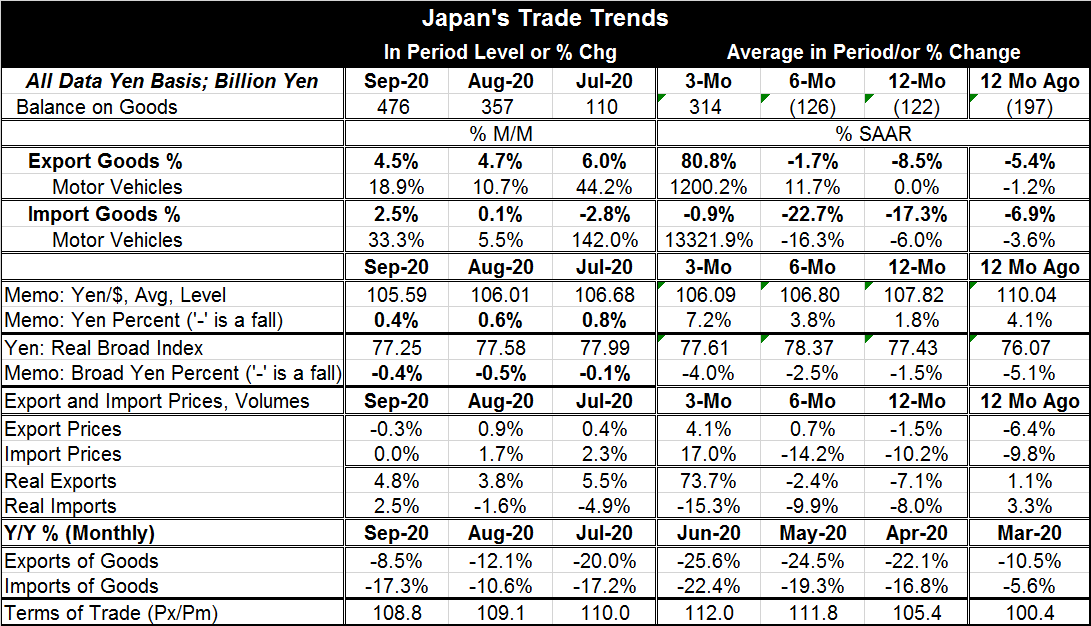

Japan has a string of three-monthly surpluses in a row, the first such string since 2017. Both export and import trends have been declining with both flows generally falling since late-2018 or early-2019. While year-on-year trends still show shrinkage, exports have reversed what had been an ongoing deceleration. Over three months, at least, nominal exports are growing briskly again.

Japan has a string of three-monthly surpluses in a row, the first such string since 2017. Both export and import trends have been declining with both flows generally falling since late-2018 or early-2019. While year-on-year trends still show shrinkage, exports have reversed what had been an ongoing deceleration. Over three months, at least, nominal exports are growing briskly again.

Month-to-month Japan's exports have risen for four months in a row. Imports are up for just two months in a row. In real terms, exports are rising for three months in a row; while real imports are higher in September without string of increases in train. In real terms, exports are very sharply accelerating while real imports continue to lay down a floundering trend.

Export and import price tends are very different too. Export prices log a small decline over 12 months then gradually accelerate rising at a 4.1% annual rate over three months. Import prices year-on-year are falling by double digits and their pace of decline accelerates over six months. It then reverses to post an annual rate surge of 17% over three months. Of course, gyrating oil prices are dominating the import price movements.

Japan's bilateral dollar and broad foreign exchange movements have been relatively tranquil over the past year. The yen has risen by 1.8% vs. the dollar and has fallen more broadly by 1.5%.

Japan's two major trading partners, China followed by the U.S., are now logging recoveries; that explains the export revival Japan is seeing. Meanwhile, real import trends do not suggest that the export revival is giving any traction to Japan's domestic demand- at least not yet.

The Tokyo Metropolitan Government on Monday reported 78 new cases of the coronavirus, down 54 from Sunday. The number is the result of over two and one-half thousand tests conducted on October 16. Compare this to Belgium, a much smaller country. Belgium has recorded an average of 7,876 new daily infections over the last seven days. This rise marks a 79% gain on the previous week. Last Tuesday, Belgium reported 12,051 cases in 24 hours, its highest daily figure since the pandemic began. Belgium and Europe are facing much worse conditions than Japan – there is really no comparison.

Very oddly Japan is having fewer overall deaths so far this year as well. This is well out of step with the global norm. While there is lots of speculation about this (here, for example), it has mostly taken heath experts by surprise. Japan's success against the virus is a part of something broader that has been in train in Japan.

Still, Japan, as a country with a very high average age takes the virus and its risk seriously. Japan's median age in 48.4 years and has risen by 5 years since just 2005. The virus is known to prey on older, less healthy people. Japan's Olympic organizers, looking ahead, are thinking of providing some heath center-like functions in the athletes' Olympic villages. Japan continues to plan ahead and Japanese citizens continue to conduct themselves with caution even though the spread of the virus has been limited.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief