Global| Jul 20 2020

Global| Jul 20 2020Japan's Trade Deficit Lingers

Summary

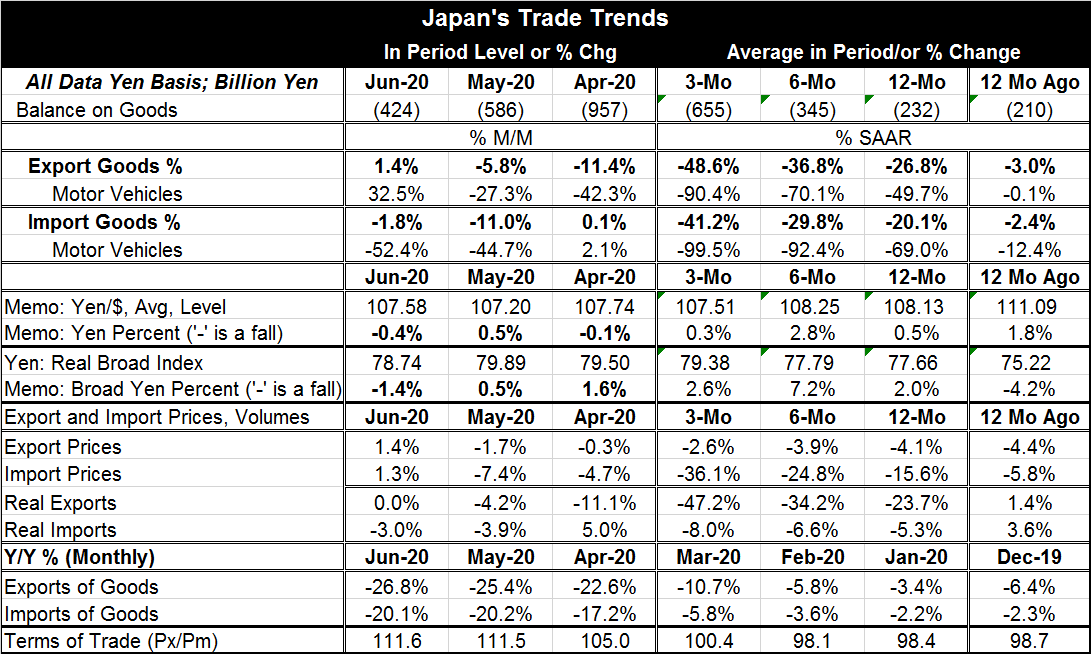

Japan's trade deficit lingers as trade flows continue to implode and fall at ever faster rates over shorter horizons- from 12-months to six-months to three-months. In June, exports logged only their fourth increase in the last 14 [...]

Japan's trade deficit lingers as trade flows continue to implode and fall at ever faster rates over shorter horizons- from 12-months to six-months to three-months.

Japan's trade deficit lingers as trade flows continue to implode and fall at ever faster rates over shorter horizons- from 12-months to six-months to three-months.

In June, exports logged only their fourth increase in the last 14 months. Imports fell in June, marking the second drop in a row on another series of data that show a preponderance of declines over the last year or so.

The yen's broad (trade weighted) exchange rate as well as the yen rate versus the dollar have been rising mildly over the last year although both measures weakened over the past month.

Export and import prices have both been falling over 12 months, six month and three months. Import prices, because of the impact of oil have been falling sharply while export prices have fallen on all horizons but have been gradually declining at a slightly slowing speed. In June, however, both export and import prices posted gains.

The results for export and import volumes basically flip the results for export and import prices. While export prices have been weak but falling modestly, export volumes are falling fast and falling increasingly fast from 12-months to six-months to three-months. Import volumes are falling on all horizons but are falling more modestly by less than double digits. Import volumes fell in June while export volumes went flat.

The volume data suggest that Japan is facing very weak demand for its exports as the virus has spread in the wake of the U.S.-China trade dispute. That weakness is not surprising, echoed by other indicators of global trade. Japan's import volumes while falling have fallen more modestly as the coronavirus cast a pall over global economic conditions.

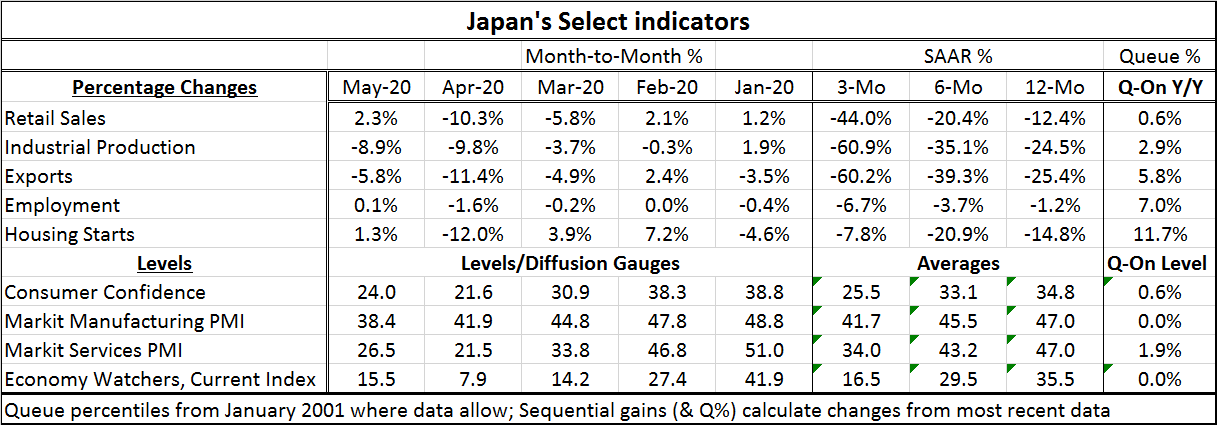

Japanese indicators continue to show a great deal of ongoing weakness. Retail sales that were hit hard on virus concerns in March and April made a modest comeback, rising by 2.3% in May. Industrial production continued to retreat in May, falling by nearly 9% month-to-month. As we can see, Japan's exports remain weak and that has an impact on industrial output. Employment barely ticked higher in May as housing starts posted a somewhat larger gain but only after a very sharp fall in April. Japanese indicators are weak with growth rates that are among the lowest 10 percentile or so that these indicators have posted since 2001.

Other indicators such as consumer confidence, the Markit PMIs and the economy watchers index are also at extreme weak levels in May. Japan does not show much life domestically while exports are suffering with some significant ongoing weakness of their own.

On balance, Japan fits the incoming global profile that does not show much good news. The virus continues to haunt the outlook everywhere although Japan has not had as bad an experience as most. Japan has other structural issues such as its mound of debt and its shrinking population. Still, Japan's main export markets, China and the U.S. have been hard hit and that is clear in the weak ongoing export trends for Japan. The Bank of Japan continues to run with full bore monetary stimulus as it has for some sometime. But Japan's domestic economy is not really responding to that and the global environment is drag for exports. This has been Japan's reality for some time now and it is continuing.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief