Global| Dec 14 2005

Global| Dec 14 2005Japan's "TANKAN" Better than Expected in December

Summary

Nearly all segments of Japanese business had better results than they anticipated in the Bank of Japan's quarterly "TANKAN" Survey. Most notably, the large manufacturing firms, which constitute the closely watched "headline" group, [...]

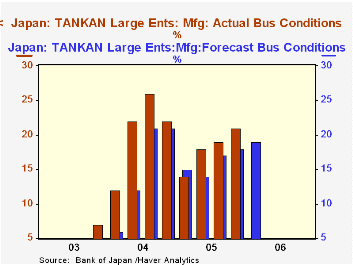

Nearly all segments of Japanese business had better results than they anticipated in the Bank of Japan's quarterly "TANKAN" Survey. Most notably, the large manufacturing firms, which constitute the closely watched "headline" group, saw their diffusion index gain 2 points from September to +21, the highest since a year ago and comparing favorably to the reading of +18 forecast by those companies last quarter. Large nonmanufacturing companies also saw a better-than-expected outturn, +17, against +16 forecast and a +15 actual in September. These businesses are circumspect about the coming quarter, however, with forecasts for March of +19 for manufacturers, down 2 points, and +17 for nonmanufacturers, a steady reading.

By industry, for large firms in the current survey, the margin of actual results over expectations was favorable in nearly areas; only food production, lumber and electrical machinery failed to beat their own forecasts. Shipbuilding, motor vehicles and paper eased somewhat this quarter from their actual results in Q3, although by less than they had forecast. For nonmanufacturing firms, eight of 11 saw improvement over the Q3 results and six of 11 beat their forecasts for this quarter; one, leasing, just met its forecast, which called for a 3 point rise.

Among medium-sized firms (capital ¥100 million to under ¥1,000 million), manufacturers gained to +9, an improvement of 3 points over their forecast and 4 points over their September results. Even so, they too look for a rollback over the winter to +6 for March. Other businesses in the size category didn't fare as well as forecast, seen in the table below, but conversely, they expected to improve this coming quarter. Small businesses remain mired in recessionary conditions generally, but manufacturers in this segment turned in a respectable +7 for the current quarter, and while still negative, small nonmanufacturing companies experienced much less deterioration than they anticipated.

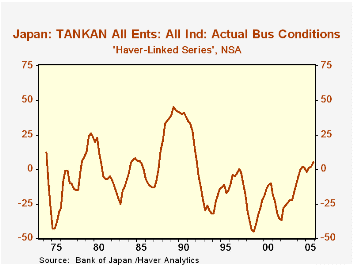

As we call to your attention frequently, this survey was dramatically reorganized two years ago, most significantly changing the very definition of "size" from employee-based to capital-based. Thus, for example, firms counted as "small" before because they employed fewer than 300 people might now be "large" because they have substantial capital; this is particularly true for high-tech companies. Thus, we continue to separate data for the two periods in the survey in our JAPAN database. However, in G10, where we include some customized series that we calculate, we show a long history for "all firms", which would not have been affected by the modified size criterion. That series, seen in the second graph, was +5 this quarter, the highest reading since Q1 1992, nearly 14 years ago. This suggests, as discussed here Monday by Louise Curley, that the recent downward revision to GDP growth for Q3 was merely a transitory adjustment and not the start of a significant deterioration in the Japanese economy.

| JAPAN: Business Conditions: % Favorable minus % Unfavorable |

December 2005

September 2005

June 2005

||||||

|---|---|---|---|---|---|---|

| Forecast for Mar | Actual | Forecast for Dec | Actual | Forecast for Sep | Actual | |

| All Firms | 4 | 5 | 2 | 2 | 1 | 1 |

| Large Firms* | 18 | 19 | 17 | 17 | 16 | 16 |

| Manufacturing ("Headline Series") | 19 | 21 | 18 | 19 | 17 | 18 |

| Nonmanufacturing | 17 | 17 | 16 | 15 | 14 | 15 |

| Medium-Sized Firms** | 5 | 5 | 3 | 2 | 3 | 4 |

| Manufacturing | 6 | 9 | 6 | 5 | 6 | 8 |

| Nonmanufacturing | 3 | 1 | 2 | 0 | 1 | 1 |

| Small Firms*** | -4 | -2 | -5 | -6 | -7 | -7 |

| Manufacturing | 6 | 7 | 4 | 3 | 1 | 2 |

| Nonmanufacturing | -9 | -7 | -12 | -11 | -13 | -12 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief