Global| May 14 2015

Global| May 14 2015Japan's Retail Sales Trends Continue to Slip

Summary

There is little good news for Japan's consumer sector. The chart shows the damage and volatility transmitted to retail spending as spending boomed ahead of the announced sales tax hike then plunged in its wake. And now even [...]

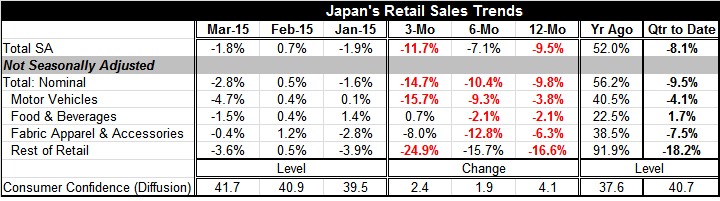

There is little good news for Japan's consumer sector. The chart shows the damage and volatility transmitted to retail spending as spending boomed ahead of the announced sales tax hike then plunged in its wake. And now even substantially removed from that time line, sales continue to struggle and appear to be on a new extended downtrend. Sales are falling at an 8.1% annual rate in Q1 2015.

There is little good news for Japan's consumer sector. The chart shows the damage and volatility transmitted to retail spending as spending boomed ahead of the announced sales tax hike then plunged in its wake. And now even substantially removed from that time line, sales continue to struggle and appear to be on a new extended downtrend. Sales are falling at an 8.1% annual rate in Q1 2015.

Three-month growth is leading six-month growth trends and 12-month growth trends lower.

There is not much wiggle room in the interpretation of these data. All the 12-month growth rates are negative across sectors, all of the six-month growth rates are negative and most of the three-month growth rates (all by one).

March brings a declined in spending across all sectors. February brought across-the-board increases. January saw declines in overall sales as well as declines in three of five sectors.

Consumer confidence in Japan has been on the rise. Its increase, however, is mild with the diffusion metric rising by just 4.1 points over 12-months and by 2.4 points over three months. The level of consumer confidence is still quite poor. Japan reports confidence as a diffusion value so with confidence at 41.7 in March, the bulk of consumers are expecting bad things rather than good. A Diffusion value of 50 is neutral. Japan is still well short of neutral.

However, if we rank this measure of confidence since April 2004 when its readings began to be taken on a monthly basis, the current reading stands in the 56th percentile of this historic queue. That gives you some idea how depressed conditions in Japan have been. A diffusion reading of 41.7 which tells us that there are 9.3% more negative responses than positive responses is above the median over the last 11 years. That means that by the standards of the last 11 years the March reading is modestly constructive - despite its clear negative standing.

Abenomics is still trying to get Japan's economy in gear. The yen is still weak. But Japan is still struggling in a weak global environment. Japan's domestic economy is beset with a huge fiscal debt overhang and weak population growth- actually the population is shrinking. That fact will put a damper on all economic data.

Japan is wary of its debt problem. The second planned hike in the consumption sales tax, aimed at reducing the fiscal deficit, has been postponed because the economy is so weak and reacted so badly to the first hike. There is still a sense that Japan has to hike taxes to get control of its fiscal position. Many international observers think Japan will not be able to deal with this stock of debt. The debt level continues to be a huge factor in assessing Japan's economy. It cannot be discounted. Consumers remain guarded and careful with their spending in part because they are unsure of what steps to corral debt government might next take. These are ongoing negatives in Japan's outlook.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief