Global| Apr 26 2019

Global| Apr 26 2019Japan's Retail Sales Lose Traction

Summary

Retail sales in Japan scored an increase in March after two consecutive monthly declines. Still, the just-completed first quarter is showing sales fall at a 4.2% annual rate. The sequential growth rates show that sales have been [...]

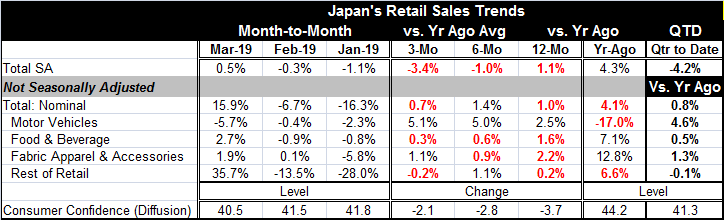

Retail sales in Japan scored an increase in March after two consecutive monthly declines. Still, the just-completed first quarter is showing sales fall at a 4.2% annual rate. The sequential growth rates show that sales have been increasing at 1.1% annual rate over 12 months, declining at a 1% annual rate over six months, and then falling faster at a 3.4% annual rate over three months.

Retail sales in Japan scored an increase in March after two consecutive monthly declines. Still, the just-completed first quarter is showing sales fall at a 4.2% annual rate. The sequential growth rates show that sales have been increasing at 1.1% annual rate over 12 months, declining at a 1% annual rate over six months, and then falling faster at a 3.4% annual rate over three months.

In step with this weakness, we can see that Japan’s consumer confidence also fell back in March; its Q1 average (see QTD value: 41.3) is weaker than its March 2018 level (44.2).

While the detailed categories for Japan’s retail sales are not seasonally adjusted, the year-over-year percentage changes still give us a clean reading on growth since year-over-year data are not very sensitive to seasonal adjustment. Year-on-year only motor vehicle sales are as strong as a 2.5% gain. Fabric apparel and accessory sales are up by 2.2%. Food and beverages sales are up by 1.6%. The rest of retail is up by just 0.2% year-over-year.

The chart shows a sharp fall-off in momentum for sales. A number of Japanese indicators have been showing a soft side. What is eye opening in this case is that the global economic weakness until now has been in manufacturing and in the output industries for tradeable goods. With this report, it is domestic retail sale sales that are weakening. Yesterday the U.K. distributive trades survey showed moderating in wholesaling and severe weakness in the outlook for wholesaling. So Japan does not stand alone with weakening domestic signals for growth.

In its meeting yesterday, the Bank of Japan provided guidance to the effect that rates would be on hold for an extended period of time. Monetary policy in Japan already is extremely stimulative between the negative short-term rates and the yield curve control policy. The central bank is not blinking and is keeping stimulus in play with no reservations with the global economy in slowdown mode.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief