Global| Apr 10 2020

Global| Apr 10 2020Japan's PPI Falls Amid Global Inflation Slowdown; Globally Inflation Dies As Expectations Rise from Its Ashes! [...]

Summary

Inflation risk in the face of corona: While the coronavirus grabs headlines and raises fears as it leaves a scattering of death around the globe, it is also wreaking havoc with economics, economic systems and any ability to create [...]

Inflation risk in the face of corona: While the coronavirus grabs headlines and raises fears as it leaves a scattering of death around the globe, it is also wreaking havoc with economics, economic systems and any ability to create projections for the period ahead. Strangely, while the clear impact of the coronavirus has been to stamp out growth and wreck economic expectations everywhere it has been, because the reaction to this outbreak has led to the launch of many government support programs and to central banks launching stimulus. Because of these efforts, inflation expectations are on the rise as well.

Inflation risk in the face of corona: While the coronavirus grabs headlines and raises fears as it leaves a scattering of death around the globe, it is also wreaking havoc with economics, economic systems and any ability to create projections for the period ahead. Strangely, while the clear impact of the coronavirus has been to stamp out growth and wreck economic expectations everywhere it has been, because the reaction to this outbreak has led to the launch of many government support programs and to central banks launching stimulus. Because of these efforts, inflation expectations are on the rise as well.

Inflation expectations

The most up to date reading on inflation expectations come from the U.S. yesterday in the University of Michigan consumer sentiment report. There, inflation expectations, as surveyed across a broad variety of actors, shows these expectations are moving higher. The University of Michigan survey looks at ‘inflation expectations' by chopping up the distribution of ‘estimates' and providing a look at the inflation expectations of optimists and pessimists as well as those in between. While all of these inflation expectation readings rose in April (all of them ROSE, to repeat), the biggest increase was from the pessimists. In reaction to all the policy levers being pulled which, economists still see as falling well short of maintaining growth and well short of keeping the unemployment rate down, inflation expectations are on the rise. Does that make sense?

Lots of commonality

I do not want to take the U.S. experience and graft it on to everyone else. Different countries have different gauges, different surveys, different yield curves and so on. But even if this were just in the dollar area, this development would be important.

Why inflation is falling

At the same time today's Japanese PPI data show inflation is falling. Inflation is falling principally for two reasons (1) economic growth is weakening (2) energy prices have been falling because of the growing glut in oil and gas supply as demand has evaporated as global activity has ground to a halt. This is a global phenomenon, not just affecting Japan.

Some common inflation elements

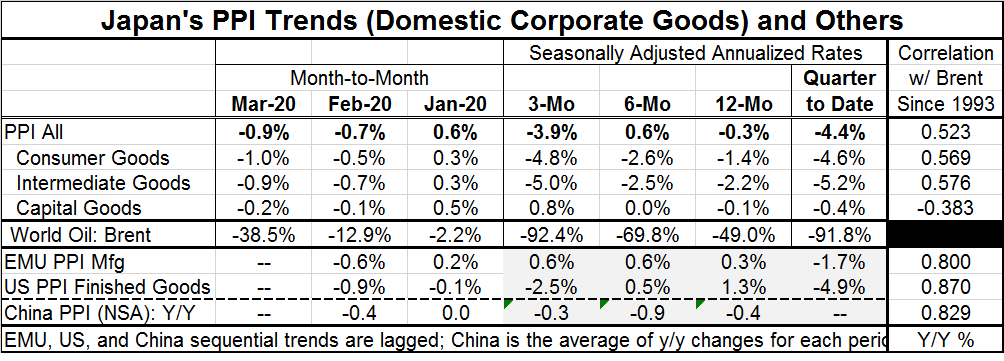

The table for Japan's PPI at the bottom shows some correlations between Brent oil and inflation rates in the EMU, the U.S. and China. The top of the panel shows Brent's correlation with various elements in Japan's own PPI. Oil seems to play a lesser role in Japan with its PPI (Domestic Corporate Goods Price Index) than it does in the other countries where the correlations are 0.8 or more. Still, oil prices have been extremely weak, so weakness in inflation is to be expected. At a time like this, we urge tracking core rates separately and putting more weight on them. Core rates of inflation either in the CPI-type gauge or PPI type gauge also have been well behaved and generally below the pace targeted for CPIs by central banks globally.

A bifurcated view on inflation

For inflation we have this bifurcated view that it is, of course, weak near terms as oil prices and growth have collapsed but the second view is: look out for the future! In addition, there is an OPEC-Russia deal that they want to pull the U.S. and the G20 in on to stabilize prices. This is highly usual. Russia and Saudi Arabia have been having this oil war because Russia was planning to be a free-rider on what it expected would be Saudi output cuts. Instead the Saudis turned the tables on them pumped even more oil, worsened the glut and intensified pressures on Russia to play ‘Let's Make a Deal.' However, neither the Russians nor the Saudis want to support ‘free riders' either.

OPEC is still struggling

If OPEC is able in some way to stop the bleeding from excess supply, some of the downward pressure on prices will abate. This is a very hard time to do that since growth is still weak and weakening and because with so many countries pursuing lockdown policies, energy demand simply is going to remain very weak for a while longer. Bringing oil supply and demand into balance couldn't be trickier.

Got inflation?

But after the crisis and when the oil market does find a new equilibrium and after the global economy is on a path to more normal growth, will all the monetary and fiscal stimulus create inflation? That is the 64 trillion dollar question.

I don't think so.

Inflation risk is lower, not higher

This fiscal spending consists of income support and income replacement intended to keep consumers and businesses whole while growth falls short. Understand that when growth shuts down for most businesses and as people lose their income stream underlying expenses continued. Government support was meant to help replace lost income and to put food on the table and pay rent and health insurance premiums and so on… However, if people look at fiscal spending as it usually is presented, as an add-on, that would be very different. If we had added that much stimulus to what was already there, I'm sure there would be now an inflationary boom. But that is not what happened. And as people go back to work, the special payments and programs will be pulled back. There will be a higher level of debt globally and that will be a drain on government resources, and in my view, it may make future growth weaker since governments will have to service this higher stock of debt. It won't make inflation higher

Tempting to inflate the high debt away?

It may be that inflating this excess debt away would be tempting. But bond markets are vigilant and any attempt to do that would cause market rates to rise and choke off growth creating a slowdown or worse. So the notion of monetizing the debt is a question of how stupid you think global financial markets would be if confronted with that tactic…

More moving parts

On balance, there are a lot of moving parts to our new future and many of them are parts that did not used to move making assessments that much harder to come by. In Japan, PM Abe has tried to fight to reduce Japan's huge mound of debt. He oversaw increases in the consumption tax, but now the needs of the nation and the requirements on government spending may blow his plan out of the water. In Europe, debt corsets too are being relaxed Maastricht or not. Southern European countries want to be sure that they can borrow to address the threat without later being put on another painful austerity diet.

Corona and the corn laws

In short, a lot is changing. And the world could change is a way that will cause the global inflation process to change. If globalization suffers, localized inflation could become a bit more of an issue. But it is too soon to handicap that. And yet clearly the issues with supply chains and with procuring medical sullies equipment and drugs as nations fought among themselves for scarce supplies has been an awakening of sorts. It is reminiscent of the ‘corn laws' in the U.K. (repealed in 1864). The ‘corn laws' refer to tariffs that protected domestic production of corn by keeping prices high and allowing domestic corn to compete with cheaper foreign corn that came under tariff. Some argued for corn laws to retain domestic production of food in the event of war. By manufacturers resented the higher prices for food that would require them to pay higher wages. In the end, corns laws were repealed and economists generally look at this as a triumph of logic and of the free trade model and its benefits.

The cost of crisis

But in this crisis, we also see what happens when supply lines are global and supplies are interrupted. Of course, a country that leans too much on domestic output of a key item could also run afoul of a domestic supply interruption. It would be more vulnerable to worker strikes and would have to administer anti-trust laws more vigilantly. Any time a domestic source is chosen over a cheaper foreign source, distortions and repercussions are put in play. But in times of crisis, these rules and concerns may shift. So it will be interesting to see how policy deals with the new reality and the new set of risks we apparently will now confront.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief