Global| Dec 28 2017

Global| Dec 28 2017Japan's IP Puts in Another Good Month But Does Not Turn the Trend

Summary

Despite another solid month of IP expansion, IP trends in Japan remain under pressure. Sequential growth rates show no clear pattern. Output generally expands fast in Japan over six months that it has over 12-months. But output also [...]

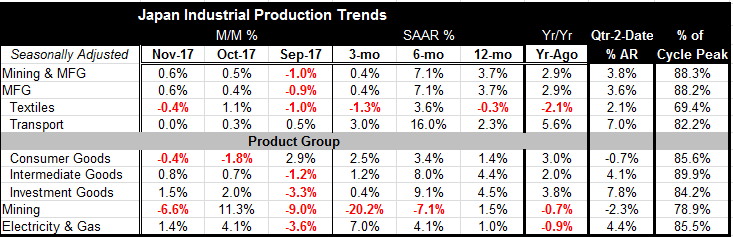

Despite another solid month of IP expansion, IP trends in Japan remain under pressure. Sequential growth rates show no clear pattern. Output generally expands fast in Japan over six months that it has over 12-months. But output also decelerates over three months compared to six months and the three-month pace is generally below the 12-month pace across sectors.

Despite another solid month of IP expansion, IP trends in Japan remain under pressure. Sequential growth rates show no clear pattern. Output generally expands fast in Japan over six months that it has over 12-months. But output also decelerates over three months compared to six months and the three-month pace is generally below the 12-month pace across sectors.

IP ramps up and falls short... However on a quarter-to-date basis output in Japan is generally looking quite solid. But that is only part of the picture.

These uneven results derive from the fact that two months ago output fell sharply. Over the next two months output has expanded briskly to compensate and restore output to a level that is only slightly above its August mark. Thus the September drop in output is still nagging output trends.

The chart shows the time series of year-on-year growth rates by sector. On that presentation all the sector indices have decelerated and consumer goods output is the weakest with investment goods output as the strongest.

Retailing in Japan rebounds, too Japan's retail sales also jumped in November gaining 2.8% month-to-month after dropping by 1% in October. While sales are up across most retail categories in the month, motor vehicle sales are coming off of back-to-back sales declines. But, year-over-year, motor vehicle sales and fabric and apparel sales are the two strongest consumer categories in Japan. Generally speaking, consumer confidence has been improving in Japan throughout the year, but doing so quite slowly.

Central banking and growth in 2018 In its recent meeting the BOJ officials began to consider, at least hypothetically, what the monetary policy end game will look like. However at its recent meeting the Bank did not alter any of its existing policies and the policy path was affirmed by an eight to one vote. Still, the BOJ is, like other central banks, has felt that it is time to let us know that it is thinking and planning ahead.

The road ahead Central banks around the world are either turning policy tighter (the US) or planning to be less accommodative (the ECB) or at least thinking about it (BOJ). Better growth is expected for 2018 more or less all around with China as the most notable exception. Still, global supply appears to be in a state of excess and excess demand does not seem plausible on any reasonable horizon. Prices generally are stable and inflation is hardly accelerating especially if you take oil out of the picture- and oil prices have ridden up recently only on an unusual and temporary supply disruption.

Bottlenecks? Looking at Japan in particular industrial output is currently only at about 88% of its past cycle peak. Ignoring any further investment that might have been made to boost potential output further, we find that current output is still 12 percentage points short of what it was at its best in the last cycle. This is hardly the stuff of bottleneck inflation. And of course, quite apart from domestic sourcing of output firms can always import. That makes capacity utilization much more of an anachronistic concept. While there may (or may not) be a step up in growth in 2018, the likelihood that supply pressures will boost prices seems remote. Labor markets may seem tighter than do capacity utilization rates as unemployment rates in Japan, Germany, the UK, and the US all are quite low. But demographics and shifting participation rate behavior make it hard to nail down what all these traditional labor market gauges really mean. Global competition and the steady implementation of technology which seems to have a strong labor-saving bias have helped to keep wage costs at bay even in those places where labor might seem to be in a highly utilized state. And THAT is not going to change in 2018.

Got demand? Are you sure? Moreover the issue of demand is hardly settled. In the US at least the pickup in spending has tailwinds from dissaving behavior (which is not sustainable) and from asset rebuilding in the wake of hurricane destruction in the South and wild fires in the West. It remains to be seen how much life consumers around the world will demonstrate in 2018 - and how much the new tax program will stimulate the US economy. As has been the case for some time, there are a lot of factories globally ready to ramp up output but there has been less consistency in the ramping up of demand. The global economy has depended too much on the US to provide demand stimulus. Have conditions in 2018 really shifted the supply-demand mix in an important way? That is the big question for the year ahead and for central bankers. Central bankers are thinking ahead and extrapolating some pretty thin trends...those in the vanguard are already taking action. But are they once again too quick on the trigger and even pulling the punch bowl away before most of the guests even arrive at the party? Those are questions for 2018.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief