Global| Jun 12 2020

Global| Jun 12 2020Japan's IP Is Very Weak...and 'Hope' Is a Four-Letter Word

Summary

Japan's industrial production index fell sharply in April and on revision the drop has been revised slightly smaller. However, the drop is still enormous and it came on the heels of a substantial drop in March and a small decline in [...]

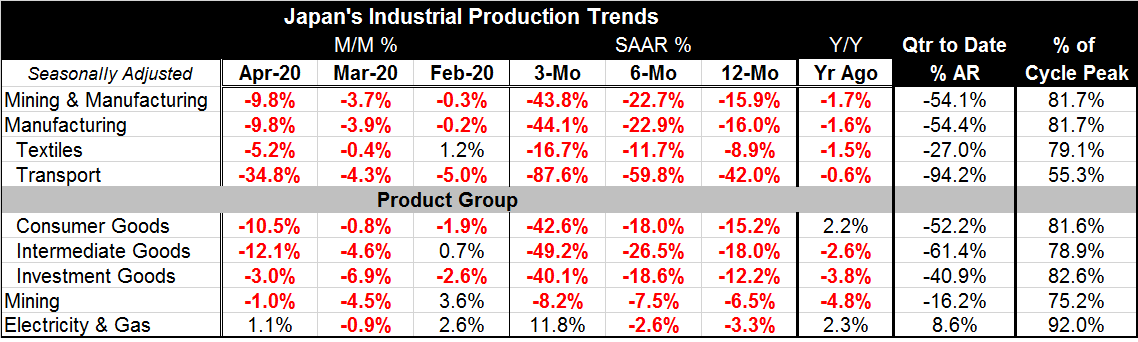

Japan's industrial production index fell sharply in April and on revision the drop has been revised slightly smaller. However, the drop is still enormous and it came on the heels of a substantial drop in March and a small decline in February. As a result, Japan's IP index, a measure of real output, is falling at an annualized pace of 43.8% over three months. Its year-on-year drop is 15.9%. The figures for manufacturing alone are just slightly worse.

Japan's industrial production index fell sharply in April and on revision the drop has been revised slightly smaller. However, the drop is still enormous and it came on the heels of a substantial drop in March and a small decline in February. As a result, Japan's IP index, a measure of real output, is falling at an annualized pace of 43.8% over three months. Its year-on-year drop is 15.9%. The figures for manufacturing alone are just slightly worse.

The weakest growth rates for manufacturing in Japan came in the 2008-2009 Great Recession cycle and again in 2011. The current year-on-year growth rate of Japanese IP ranks as the 11th weakest year-on-year tally in any month since 2000.

However, recall that Italy is seeing output declines at annual rates at a 90% or more and its year-on-year drop is 45%. Japan is nowhere near that kind of weakness. In the quarter-to-date, Japanese output is falling at a 54% annual rate and that is a big number for Japan but globally it compares to an Italian number of 95%. Many countries in Europe are seeing much more weakness than is Japan even though the center of the coronavirus was transmission out of China. It is a transmission that the rest of the world has become more and more suspicious about and that China has become more secretive and defensive about.

Japan's transportation and textile sectors have been hard-hit as transportation output is only at 55% of its past cycle peak compared to 79% for textiles and 81% overall.

The three major manufacturing sectors, consumer goods intermediate goods and capital goods, have very similar ratios to their past cycle peaks clustered at ranking-readings in their respective high 70th percentiles to low eightieth percentiles.

Japanese IP's annualized growth rates show progressive weakness because the last three-months are the weakest things on this planet in at least a decade just about anywhere you look – Japan included. The only exception is Japan's electricity and gas usage perhaps because with stay-at-home policies consumers stayed home and consumed more utilities output than they otherwise would have done.

There are no new policy moves from Japan. The Bank of Japan is holding the line on its policy. Globally the Fed seems to have a policy of never-ending essentially zero interest rates and may be considering a yield curve control policy like the one Japan uses. The EU Commission has yet to set a stimulus policy handcuffed by its own problems concerning the political correctness of stimulus and who should be helped. The U.S. is embroiled in an intractable domestic political fight that just has been worsened by racial animosities and it will be hard for policy in the U.S. to do the 'right thing' since both political parties are focused on the impact any policy will have by November when nationwide elections will be held.

The global economy remains weak with 'new signs' or 'heightened fears' in the U.S. of a second wave that may (or may not) be mounting. Regardless, it is increasingly less likely that the U.S. will lead the way ahead with a strong economic recovery. Japan has many of its own problems with a mountain of debt and has gone for some time with monetary policy running with the throttle wide open. Japan has played all its cards; it is at the whim of the international community for any ray of hope. Instead of the pending goods of economic re-openings and the potential for a more rapid recovery abroad, Japan has a serious geopolitical issue playing out in Asia involving for now China and Hong Kong but perhaps Taiwan too. Japan's glimpse of hope for much better global growth may be fading.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief